- Price gap widens between offers, bids

- Mills prefer domestic scrap, cap imports

Vietnam’s bulk ferrous scrap prices witnessed mixed trends as trade activity slowed ahead of the year-end. A Vietnamese mill source stated that the holiday season has seen fewer offers and lower bids, with volatile billet and rebar prices leading to minimal restocking.

The fluctuation in billet and rebar prices also led to caution among buyers. Consequently, demand for deep-sea ferrous scrap imports into Vietnam remained subdued last week.

Despite Vietnam not celebrating Christmas, many suppliers were absent, and with the Lunar New Year approaching, market participants expect little change before February.

Additionally, with domestic scrap being more cost-effective, most Vietnamese mills limited their seaborne scrap intake.

CFR assessments

- Deep-sea bulk US cargoes of HMS (80:20) stood at $352/t, up slightly by $2/t w-o-w.

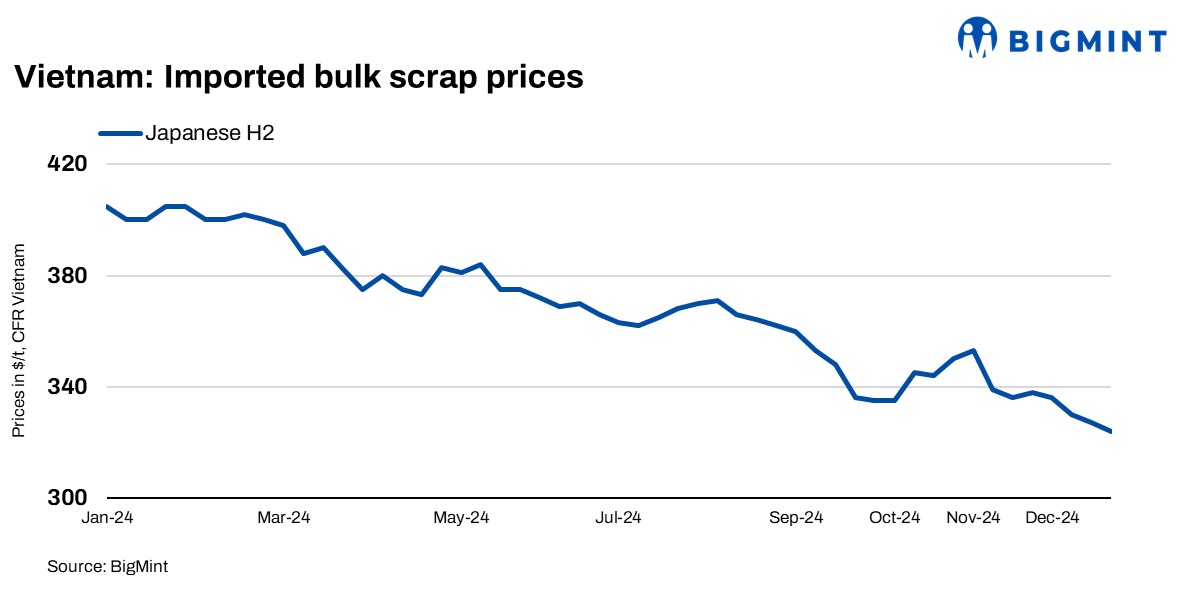

- Japanese-origin H2, a major tradable grade in Vietnam’s scrap market, was at $324/t, a drop of $3/t w-o-w.

Recent price trends

Japanese scrap remained out of favour, with limited interest from Vietnamese mills. Tokyo Steel, a leading scrap buyer in Japan, reduced its domestic scrap purchasing prices at Tahara and Utsunomiya plants by JPY 500/t earlier last week, further dampening interest. As a result, Vietnamese bids for H2 scrap fell to $315-320/t CFR, down by $3-4/t w-o-w. Offers dropped to $322-324/t and hovered at these lower levels.

Deep-sea offers for HMS (80:20), priced at $358-360/t CFR Vietnam, were limited and largely stable from the previous week. However, with longer delivery times and higher costs compared to Japanese material, no bids were heard at these levels.

For buyers, maximum workable prices of US-origin bulk HMS (80:20) remained at around $345-350/t CFR Vietnam. These levels have remained largely the same for five consecutive weeks. Some mills opted for smaller-volume containers to fulfil their inventory needs.

Low-grade scrap imports from the US and South America were transacted within the range of $290-295/t CFR Vietnam, with a deal for HMS (70:30) concluded at $290/t.

Overall sentiment remained weak, with mills already holding high inventories of finished products due to slow sales. This kept buying activity minimal.

The gap between offers and bids widened to $8-10/t in the third week of December from $5-6/t in the previous one, with some buyers reluctant to accept higher prices. For instance, Japanese bulk H2 scrap was offered at $328-330/t CFR Vietnam, but bids were capped at $318-320/t. Similarly, US-origin HMS (80:20) scrap was priced at $355/t CFR Vietnam, while Vietnamese mills were unwilling to conclude deals higher than $345/t CFR.

In the domestic market, a northern mill lowered its scrap purchasing prices of the H1 grade by VND 100/kg ($4/t) to VND 9,000-9,100/kg ($353-357/t) DDP, effective mid-week. Prices of local 3sp IF billets also decreased slightly by VND 100/kg ($4/t) to VND 11,500-11,700/kg ($451-460/t) DDP.

Outlook

Market activity in Vietnam remains slow as the year-end holidays approach, with many sellers holding off on transactions in expectation of a potential price recovery after the Lunar New Year. Prices are expected to increase in February, especially as the construction season resumes, but some Japanese shippers are hesitant to sell at the current low values. Most Vietnamese mills continue to prefer domestic scrap due to its more competitive pricing, keeping scrap imports at a standstill.

With minimal price movement expected in the short term, buyers are likely to delay new purchases until clearer directions emerge in the new year. The market outlook will depend on how the post-holiday demand and supply dynamics unfold.

Leave a Reply