- US scrap demand strong, exports face resistance

- Slow collection keeps EU-origin scrap prices firm

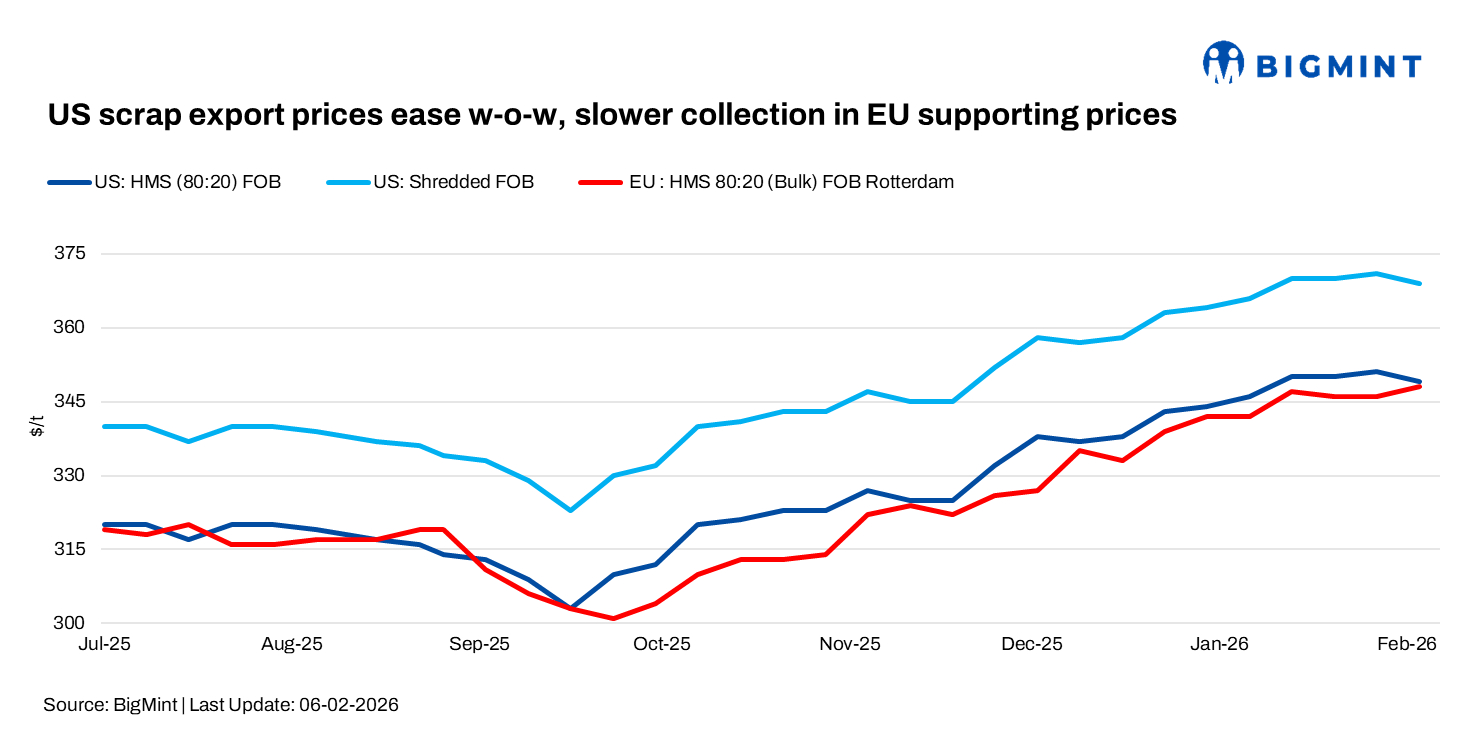

US scrap export prices edged lower w-o-w in early February, even as domestic steelmakers raised bids amid weather-driven supply disruptions across the eastern US. Harsh winter conditions, including snow and ice linked to a polar vortex, disrupted scrap collection and delayed January shipments, prompting US mills to move early to secure February volumes. Scrap collections across Europe remain tight, limiting cargo availability and keeping sellers firm.

Bid-offer gap in export market

Steelmakers in the US Midwest and Southeast raised bids for February-delivered shredded scrap by around $30/t m-o-m, reflecting tight scrap availability and the need to incentivise collections. However, export sentiment remained capped as overseas buyers resisted higher offers. Market participants assessed tradable levels for US or premium-origin HMS 80:20 at around $375-378/t CFR, below seller targets of $380-385/t CFR, highlighting a widening bid-offer gap in the export market.

As a result, FOB export values softened slightly despite strong domestic demand.

FOB assessments (US East Coast, bulk)

- HMS 80:20 at $349/t, down $2/t w-o-w

- Shredded at $369/t, down $2/t w-o-w

US-origin HMS 80:20, bulk – CFR assessments

- Turkiye: $377/t, up by $1/t w-o-w

- Vietnam: $342/t, up by $2/t w-o-w

- Bangladesh: $367/t, stable w-o-w

EU: Currency volatility, quality issues shape offers

European scrap sellers remained cautious as euro volatility continued to complicate export pricing. The euro weakened to around $1.18, down from $1.192 a week earlier, squeezing competitiveness. Despite this, EU sellers continued to target $372-373/t CFR Turkiye, with some offers extending into the high-$370s/t CFR.

Industry participants expect price spreads between premium and obsolete scrap grades in Europe to widen further in 2026. As per market insiders, the current euro 6/t gap between old and new scrap could widen sharply as competition for high-quality scrap intensifies. Lower manufacturing activity across Europe is curbing fresh scrap generation, while recyclers face rising labour, energy, and operating costs. Similar pressures persist in the UK, where costs remain 35-40% above pre-pandemic levels.

Italian export offers to India reflected euro dynamics, with shredded scrap quoted at €320-340/t FOB (around $374-398/t) and HMS 80:20 at €290-300/t FOB ($339-351/t). Scrap collections across Europe remain tight, limiting cargo availability and keeping sellers firm.

As per a dockside market participant, in the Benelux region, good-quality HMS was discussed at around €280/t, equivalent to roughly $328/t FOB. With supply constraints persisting, effective costs rise further after adding dock charges of about €15/t (around $18/t), pushing workable FOB levels closer to $345-350/t.

Outlook

Scrap export prices are expected to stay rangebound as tight collections in the US and Europe support fundamentals, but buyer resistance caps upside. Strong US domestic demand may continue to divert material inward, while euro volatility and widening quality spreads are likely to keep export negotiations selective and prolonged.

Leave a Reply