- Company’s thermal coal sales rise

- Centurion targets 500,000 t in 2025

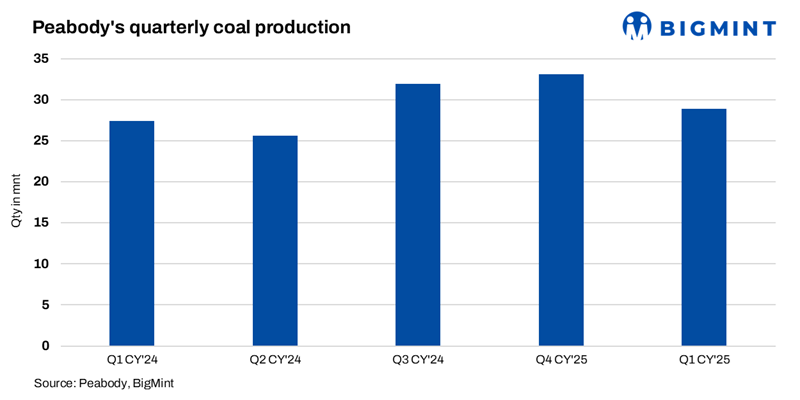

Peabody Energy sold a total of 28.9 million tonnes (mnt) of coal in the first quarter of 2025 (Q1CY’25), up from 27.4 mnt in the same quarter last year.

The Powder River Basin led with 19.6 mnt, followed by ‘Seaborne Thermal’ (4.4 mnt), ‘Other U.S. thermal’ (3.1 mnt), and ‘Seaborne Metallurgical’ contributing 1.8 mnt, according to the company’s report. Notably, the Centurion mine exceeded development targets and remains on track for 500,000 t of sales in 2025.

Segmental performance highlights

Seaborne thermal: Delivered $84.2 million in adjusted EBITDA with 4.4 mnt sold, surpassing guidance. While realised export prices dropped to $79.39/t from $96.41 in Q4CY’24, strong output from the Wilpinjong Mine helped offset the decline.

Seaborne metallurgical: This segment saw a dip, with EBITDA at $13.2 million due to a 9% drop in benchmark pricing and lower volumes (1.8 mnt).

Powder River Basin (PRB): PRB posted 19.6 mnt in sales, generating $36.3 million in EBITDA. Strong U.S. coal demand pushed margins to 13%.

Other U.S. thermal: Sales reached 3.1 mnt. EBITDA came in at $32.9 million with margins at 20%. Revenue per ton was $54.32, and costs were maintained at $43.71, down 6% from Q4CY’24.

Operational and strategic developments

Peabody maintained capital discipline with operating cash flow of USD 120 million. It remains ahead of schedule on Centurion Mine development, which shipped its second batch of premium hard coking coal and is on track to meet its 500,000 t sales goal for 2025. Full-scale longwall production is slated for Q1 2026.

Peabody has raised a material adverse change concerning the March 31, 2025 gas incident at Anglo American’s inactive Moranbah North Mine, putting their coal asset acquisition at risk. The deal may be terminated if the issue isn’t resolved promptly.

The company also signed a seven-year contract with Associated Electric Cooperative Inc., securing 7-8 mnt annually for Midwestern power stations.

Financial position and outlook

Peabody holds a strong balance sheet with USD 696.5 million in cash and over USD 1 billion in liquidity. The company declared a USD 0.075 per share dividend and remains cash-positive on a net-debt basis.

“While the second quarter typically reflects seasonal softness in thermal coal demand, we’ve successfully secured full commitments for our planned 2025 production from the Powder River Basin. Additionally, metallurgical coal prices have rebounded from their March lows, supporting a more favorable market outlook.” said Peabody President and CEO Jim Grech.

Leave a Reply