- NAPP coal gains cost advantage

- Cement buyers turn increasingly selective

US Northern Appalachian (NAPP) thermal coal is steadily strengthening its position in India’s cement and industrial fuel mix as delivered-cost economics tilt in its favour against fuel-grade petroleum coke (petcoke). Supported by softer freight, competitive calorific economics and a growing pipeline of incoming cargoes, US-origin high-CV coal is increasingly being evaluated by cement producers as a viable substitute, particularly at a time when petcoke continues to struggle with subdued demand and seasonal caution ahead of the monsoon.

The shift is not yet broad-based, but market participants indicate that procurement strategies across several cement producers are increasingly being guided by delivered energy economics rather than headline cargo prices, with buyers weighing fuel flexibility and margin protection against uncertain demand conditions.

NAPP coal improves delivered energy competitiveness

US NAPP coal of around 6,900 NAR was heard trading in the mid-$130s/t CFR east coast India, while offers for west coast India were heard in the low-to-mid $130s/t CFR range. At these levels, the fuel has begun to offer a modest but meaningful calorific-cost advantage over imported petcoke.

US Northern Appalachian (NAPP) coal with a calorific value of around 6,900 NAR was indicated at approximately $135-140/t CFR, translating to an estimated energy cost of about $19.4-19.8/GCal. In comparison, imported petcoke with 6.5-8.5% sulphur content was heard at around $147-152/t CFR, with approximate energy economics of $20.2-20.6/GCal.

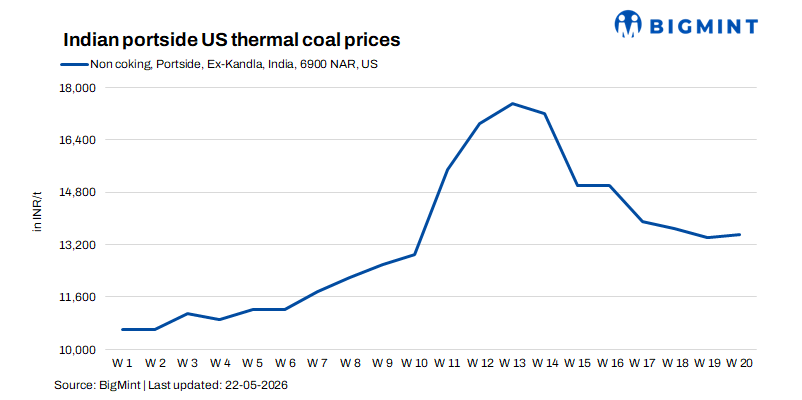

As per BigMint’s assessment of Non coking coal, Portside US (6900 NAR) Kandla rosed moderately by INR 100/t w-o-w to INR 13,500/t.

While the cost differential appears relatively narrow on a per-unit basis, market participants noted that for large cement kiln operators consuming substantial volumes, even a marginal advantage translates into meaningful savings when scaled across sustained procurement cycles.

A trader active in the west coast market said cement producers are increasingly reluctant to commit to fresh petcoke purchases at prevailing price levels when US coal offers better calorific economics and greater flexibility in blending. According to market participants, the focus has shifted from outright price comparison to cost per unit of heat generation, where NAPP coal is beginning to secure an advantage.

The competitive pressure has become more visible as petcoke prices continue to soften while coal offers remain comparatively attractive. Cement producers, particularly those with fuel flexibility, are increasingly balancing domestic coal, imported thermal coal and petcoke rather than relying on a single feedstock.

Heavy cargo inflows reshape market sentiment

At the same time, India is witnessing a significant inflow of NAPP and Illinois Basin (ILB) coal, both for industrial consumers and the retail market, indicating that traders remain confident in medium-term demand despite near-term buying caution.

Data compiled by market participants indicate that around 0.51 mnt of floating NAPP cargoes are currently destined for the retail market, while nearly 2.0 mnt is lined up for industrial consumers over the coming weeks.

Among key industrial cargoes, Ultratech Cement remains one of the largest recipients, with multiple vessels scheduled across Tuna, Kandla and Gangavaram, reflecting sustained interest in imported high-CV fuel. Cargoes for Wonder Cement, Ramco, JSW and India Cements are also expected over the coming month, suggesting that industrial buyers continue to maintain procurement optionality even as spot buying slows.

The influx of cargoes comes at a time when immediate buying appetite remains measured, particularly in the retail market where stock availability has risen sharply.

Retail market sees inventory build-up as lifting slows

Retail demand for imported NAPP coal weakened during Week-20, with total lifting declining to 94,410 t, compared with 112,392 t in Week-19, even as fresh arrivals pushed inventories higher. Closing retail stock at Kandla and Tuna increased to 587,805 t as of 18 May, up from 435,654 t a week earlier, indicating a clear build-up in portside availability.

The increase in stocks has begun to soften sentiment in the retail market, with buyers largely procuring on a need basis rather than building fresh inventory positions.

Market participants noted that buyers are showing little urgency amid expectations of softer seasonal demand and the approaching monsoon. Several cement producers are also believed to be comfortable with existing fuel cover, reducing immediate spot-market requirements.

A trader based in western India said cement producers are increasingly cautious about booking large spot cargoes ahead of the rainy season, preferring to stagger procurement and preserve flexibility.

Cement sector turns selective amid monsoon caution

The cement industry’s fuel buying strategy appears to be entering a more cautious phase. While several producers continue to maintain imported fuel programmes, fresh procurement has become more selective as companies weigh slowing construction activity, softer seasonal demand and uncertainty surrounding freight movements.

The approaching southwest monsoon is also expected to weigh on cement demand in several regions, prompting buyers to adopt a wait-and-watch approach. Market participants indicated that procurement decisions are increasingly being staggered rather than front-loaded, especially when domestic coal availability remains relatively comfortable.

At the same time, logistical considerations are also influencing decisions. Some market participants said imported fuel demand could receive support if domestic coal transportation tightens during peak summer months, when rail prioritisation for thermal power stations occasionally constrains industrial fuel movement.

Outlook: supportive economics but near-term buying remains cautious

Looking ahead, US NAPP coal is expected to remain competitive in India’s industrial fuel basket as long as the delivered calorific advantage over petcoke persists. However, the sizeable pipeline of incoming cargoes, rising port inventories and seasonal demand moderation could keep spot buying disciplined over the near term.

For now, market participants expect buyers to remain selective, with procurement likely to stay closely tied to immediate consumption needs rather than aggressive inventory accumulation. While freight volatility and geopolitical uncertainty may continue to influence landed costs, US NAPP coal appears increasingly positioned as a practical substitute for petcoke in India’s cement sector, particularly for buyers prioritising fuel flexibility and delivered energy efficiency.

Leave a Reply