- Rising supply raises risks pressuring Indian prices

- Approaching monsoon to dampen cement demand

US Northern Appalachian (NAPP) thermal coal has established a strong foothold in India’s cement sector as elevated petroleum coke prices force a structural shift in fuel sourcing. Cement producers, which account for the bulk of India’s petcoke imports, have moved decisively toward high-calorific-value US coal after months of resisting high petcoke prices. However, with over 3.1 million tonnes (mnt) of US coal already heading to Indian ports and the monsoon approaching, the market is entering a phase where supply could outpace demand.

US NAPP coal becomes cement producers preferred substitute for petcoke

US NAPP coal, with calorific values of 6,900-7,100 kcal/kg NAR, has emerged as the closest viable substitute for petcoke. Its high energy content allows cement plants to maintain kiln efficiency while lowering fuel costs.

By late April, US NAPP coal was offered at $135-140/t CFR India, with some tenders indicating levels as low as $133/t. A deal at $135/t CFR underscores its competitiveness relative to petcoke.

Supply into India has scaled up rapidly. Over 3.1 mnt of US coal is either at anchor or en route, split between retail and industrial consumers. Cargoes are scheduled to arrive through mid-June across key ports including Kandla, Tuna, Gangavaram, Dhamra, and Paradip.

Retail demand has remained steady, with lifting averaging over 100,000 t/week in late April. Combined port stocks at Kandla and Tuna stood near 389,000 t in early May.

Supply builds, prices begin to soften

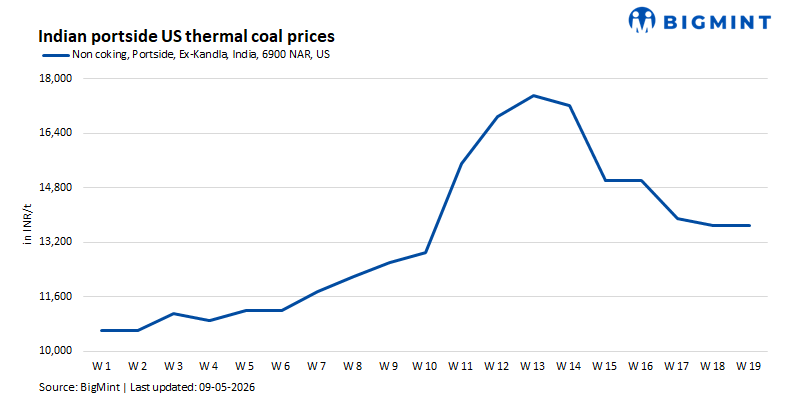

Despite strong initial uptake, early signs of price softening have emerged. Portside prices have declined to INR 13,200-13,500/t ex-Kandla in early May, down from levels above INR 15,000/t in March.

This easing reflects a combination of factors. On the supply side, logistical bottlenecks at US ports have delayed shipments, while a large volume of cargoes continues to move toward India. On the demand side, the approaching monsoon is dampening buying interest, as cement plants typically reduce inventories ahead of seasonal construction slowdowns.

With significant volumes already committed, buyers are increasingly reluctant to chase spot cargoes.

Divergence between retail and industrial markets

A key feature of the current market is the divergence between bulk industrial buyers and the retail segment. While large cement producers have secured coal at lower prices through direct procurement, retail prices have remained relatively firm due to concentrated inventory positions at ports.

Earlier tightness — driven by limited stocks and concentrated holdings — created premiums for prompt cargoes. Although this has eased with incoming supply, retail demand remains steady, suggesting continued underlying consumption even as large buyers step back.

US market dynamics shape Indian pricing

Indian pricing for US NAPP coal is increasingly linked to US domestic market conditions. FOB Baltimore prices for 6,900 NAR coal softened to around $93-94/t in late April, but logistical constraints — including vessel queues and slow loading — have limited the pass-through of lower FOB prices.

This has created a two-speed market: softer FOB levels in the US, but relatively supported CFR prices in India due to freight and supply chain constraints.

Freight remains a critical variable. Although rates have eased from peaks seen after the Hormuz disruption, they remain elevated, keeping delivered costs relatively firm despite softer origin prices.

Cement demand underpins structural shift

The longer-term outlook for US NAPP coal in India remains supported by cement sector fundamentals. Cement production grew 8.6% in FY’26 to 491.4 mnt and is expected to expand further on the back of infrastructure and housing demand.

This provides a stable demand base for imported fuels. Even if petcoke prices correct, the shift toward coal is unlikely to reverse quickly, as cement producers have already reconfigured fuel blends and procurement strategies.

For example, Ultratech Cement reduced petcoke usage to 41% of its fuel mix in January-March 2026, down from 54% a year earlier, signalling a structural rather than temporary shift.

Market sentiment reflects this transition. Buyers are increasingly focused on coal — both imported and domestic — while interest in petcoke remains subdued.

Outlook: balance between supply pressure and structural demand

The near-term market will be driven by three factors.

First, the pace of incoming US cargoes. With over 3.1 mnt scheduled to arrive by mid-June, portside inventories are expected to rise, especially as monsoon-related demand slows.

Second, petcoke price movements. While prices have softened from recent highs, they remain elevated enough to keep coal competitive. A sharper correction could narrow the substitution advantage, but a full reversal appears unlikely.

Third, broader supply dynamics, including freight and global trade flows, will continue to influence delivered coal prices into India.

For now, US NAPP coal has secured a durable position in India’s cement fuel mix. However, with supply building and seasonal demand weakening, the market is likely to see continued price pressure in the near term. The key question is not demand, but how much of the incoming supply the market can absorb without triggering a sharper correction.

Leave a Reply