- Holiday season slows export activity

- Weather disruptions restrict US yard receipts

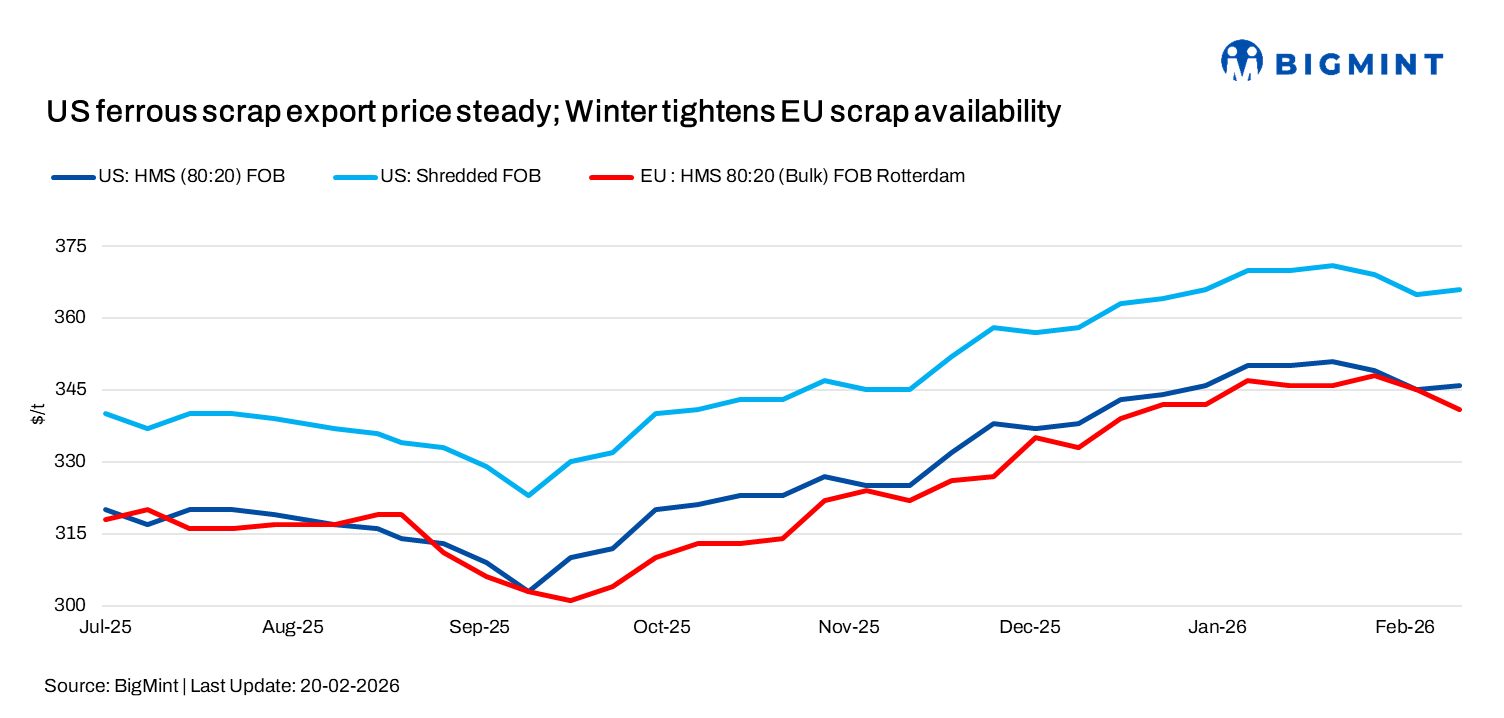

Global ferrous scrap markets displayed mixed but largely steady trends in the week ended 20 February, as tight supply conditions in the US contrasted with subdued buying interest across Europe. Weather-related disruptions, firm collection costs, and currency movements continued to influence exporter positioning.

US market steady as tight supply supports export levels

US export scrap prices remained largely stable, as tight domestic supply and ongoing winter weather limited yard inflows. Exporters were unable to reduce offers meaningfully despite buyer resistance.

A market participants Commented, “that a widening gap between contracted dock prices and lower spot levels, as exporters attempt to manage average costs. Some large tonnage dock prices were reportedly around $30/t above spot purchases.”

Midwest shredded held steady at $450/t delivered. While February saw slight firmness after weather disruptions.

FOB assessments (US East Coast, bulk)

US-origin HMS 80:20, bulk – CFR assessments

- Turkiye: $375/t, down by $1 w-o-w

- Vietnam: $359/t, up by $4/t w-o-w

- Bangladesh: $375/t, up by $2/t w-o-w

Europe market quiet amid firm costs and seasonal slowdown

European scrap markets stayed largely quiet, with limited fresh bulk trades. UK containerised shredded was heard at $370-375/t CFR India, while HMS 80:20 traded at $348-355/t.

For Pakistan, EU shredded offers were around $378-380/t CFR, with workable levels closer to $375-376/t.

Collection rates held steady despite winter, but firm euro and higher collection costs pushed exporter breakeven levels into the low $370s/t CFR.

Australia market records selective deals

Australian-origin scrap saw limited but firm transactions this week. HMS 80:20 was concluded at $320/t CFR Thailand, while sales to Chennai were reported at $350-355/t CFR.

Despite these deals, fresh offers to Chennai remain challenging to negotiate, with HMS 80:20 indicated around $350/t and shredded near $370/t, levels considered difficult for buyers under current market conditions.

Outlook

We expect the scrap markets to remain muted in the near term. Improving weather in the US may ease supply tightness and slightly pressure domestic and export offers in March. European exporters are likely to keep firm offers due to high collection costs and currency support, though weak steel demand may limit bookings. Australian offers to South Asia may remain difficult to close unless sentiment improves.

Leave a Reply