- US pig iron imports up 25% y-o-y; scrap imports rise 11%

- Weak demand from Turkiye, Bangladesh trims imports

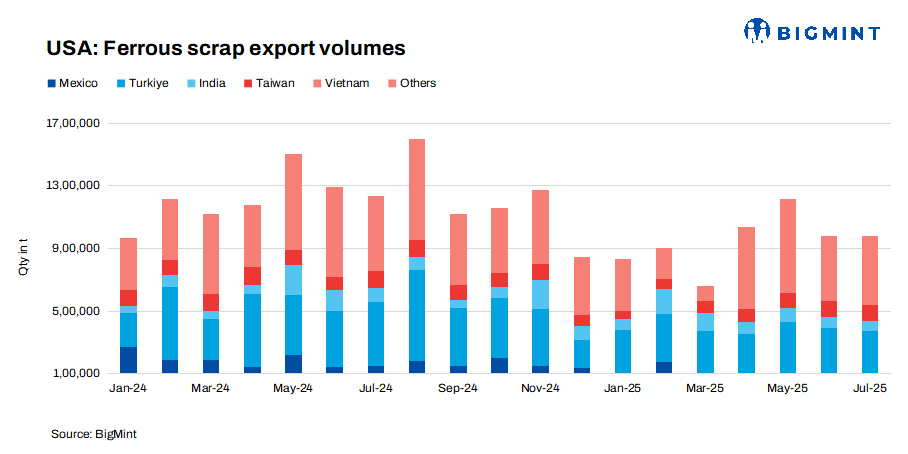

US ferrous scrap exports fell 16% y-o-y to 7.19 million tonnes (mnt) in 7MCY’25 from 8.52 mnt in the same period of 7MCY’24. In July, exports reached 981,633 tonnes (t), slightly up 0.13% from June, but down 21% y-o-y from July 2024. H1CY’25 exports declined 15% to 6.21 mnt versus 7.28 mnt in H1CY’24.

US scrap prices

Shredded scrap averaged $350/t and HMS $328/t in 2025, both down $40/t from 2024, driven by weak overseas demand from Turkiye and Bangladesh, currency pressures, and ample US supply.

On the US East Coast, bulk HMS export prices dipped below $300-305/t at times and have stayed under $320/t since July, with East Coast shredded pricing following a similar trend.

Despite anticipated volatility from tariffs, RMDAS data show stable pricing from mid-May through early October. Shredded scrap averaged $375-380/t in August-September, HMS stayed within $337-355/t, and September saw a brief $19/t decline in the RMDAS industrial composite to $425/t.

Country-wise US ferrous scrap exports

- Turkiye: Imports fell 16% to 2.13 mnt in 7MCY’25 from 2.55 mnt in 7MCY’24, showing slower intake.

- Mexico: Scrap imports declined 50% to 0.66 mnt in 7MCY’25 from 1.31 mnt in 7MCY’24 due to weaker demand and reduced steel production.

- India: Imports remained steady at 0.65 mnt in 7MCY’25, unchanged from 7MCY’24, as sluggish steel demand and higher domestic scrap collection limited overseas purchases.

- Taiwan: Scrap imports dropped 20% to 0.57 mnt in 2025 from 0.71 mnt in 7MCY’24, reflecting weaker steel production and a shift to alternative raw materials.

- Bangladesh: Imports fell 12% to 0.92 mnt in January-July from 1.04 mnt in 7MCY’24, impacted by weak steel demand, currency pressures, high inventories, costly freight, and cheaper regional alternatives.

Global context is mixed: While China’s output slowed in late summer, Turkiye and India are seeing steel production growth in 2025. Domestic melt shops continue steady operations, supported by strong demand in non-residential construction, automotive, energy, and industrial sectors, though some recyclers note margin pressures as scrap costs decline relative to steel prices.

US scrap imports: US scrap imports increased by 11% y-o-y to 2.79 mnt in 7MCY’25, up from 2.51 mnt in 7MCY’24, and also increased in m-o-m by 5.7% to 0.37 mnt in Jul’25 from 0.35 mnt in Jun’25. In March, imports hit a record 459,335 t-up 110% y-o-y, driven by tariff concerns, with sharp rises from Canada, Mexico, and Europe.

Other updates

US pig iron imports: Pig iron imports increased by 25% to 3.33 mnt y-o-y in 7MCY’25, up from 2.66 mnt in 7MCY’24. US pig iron imports surged in May but dropped in June and July amid trade policy uncertainty and higher tariffs on Indian imports, impacting supply. Brazil remains a key supplier, with US imports falling from Brazil in early to mid-2025 due to the trade tariffs.

Crude steel production remained stable at 47 mnt in 7MCY’25, showing only a marginal dip from 47.38 mnt recorded in the same period of 2024, indicating steady output despite market challenges. US mills are operating at 75-77% capacity versus 75-78% in the same period in 2024.

Outlook: While scheduled mill maintenance may temporarily reduce demand, market participants expect scrap prices to remain flat through year-end with a nominal change in export volume barring unforeseen events.

Leave a Reply