- US scrap buyers show limited appetite this week

- Export prices steady amid thin buying activity

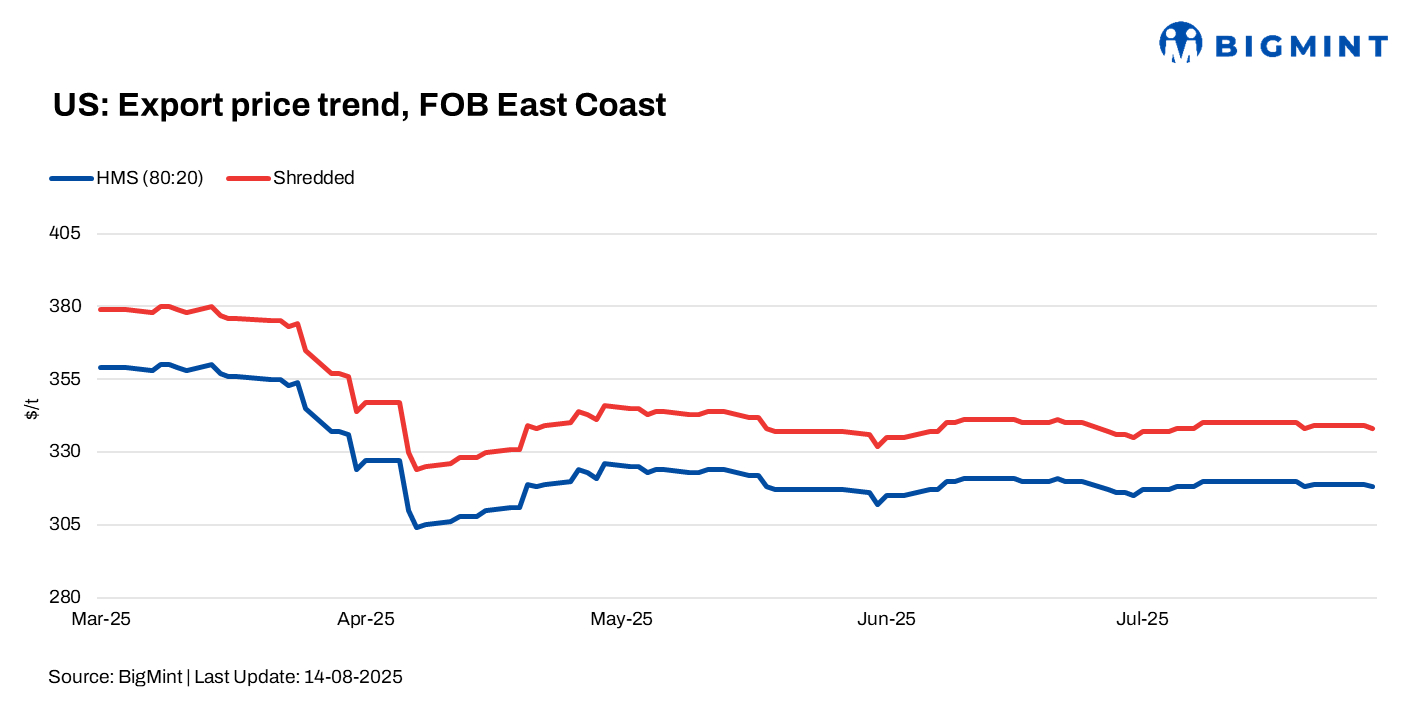

US ferrous scrap export prices were stable this week. Weak demand from key buyers kept US ferrous scrap export prices largely stable. In the domestic market, US scrap trade for August concluded quietly, with both buyers and sellers expecting subdued sentiment to persist into September.

A side participant said, “Buyer were initially kept turnings prices unchanged but lost material, prompting them to raise offers. They added that September will likely remain sideways with ample scrap supply across most regions and only a slim chance of a modest price increase.”

FOB assessments (US East Coast, bulk)

- HMS 80:20 – $319/t, stable w-o-w.

- Shredded – $339/t, stable w-o-w.

US-origin HMS 80:20, bulk – CFR assessments

- Turkiye – stable w-o-w at $347/t.

- Vietnam – up by $3/t w-o-w at $333/t.

- Bangladesh –up by $3/t w-o-w at $353/t.

Updates on key importers

Turkiye: Turkiye’s deep-sea scrap market held largely stable w-o-w. Mills slowed purchases in recent days but are expected to step up bookings for September shipments as low-priced billet and slab from Asia remain scarce.

Factors shaping Turkish scrap demand

- Weak domestic and export rebar sales keeping mill demand restrained

- Limited billet availability and some sentiment support from overseas markets

Despite a brief July uptick in scrap bookings, mills stayed cautious, awaiting clearer price direction and potential $3-5/t gains for September-October loadings.

Bangladesh: Demand for US-origin scrap in Bangladesh stayed muted w-o-w, with mills limiting fresh bookings amid a monsoon-led construction slowdown. Shredded and busheling were at $370-375/t and $385-390/t, respectively.

Domestic scrap prices held firm, with local grades at BDT 46,000-47,000/t ($379-387/t) and premium grades at BDT 49,000-50,000/t ($403-411/t). Mills are expected to resist higher offers in the near term amid weak steel demand.

Vietnam: Imported scrap prices rose w-o-w, driven by tight supply and improved sentiment from China, though trading stayed limited. Offers stood at $345-350/t CFR, bids at $325-340/t, with prices supported by supply constraints despite weak downstream steel demand.

Outlook

Supply constraints and limited billet availability may lend slight upward pressure to prices, but weak finished steel demand in key importing regions will likely keep gains modest and trading activity subdued in the near term.

Leave a Reply