- Weak buying from importers weighs on scrap prices

- Vietnam, Bangladesh see slight gains despite muted demand

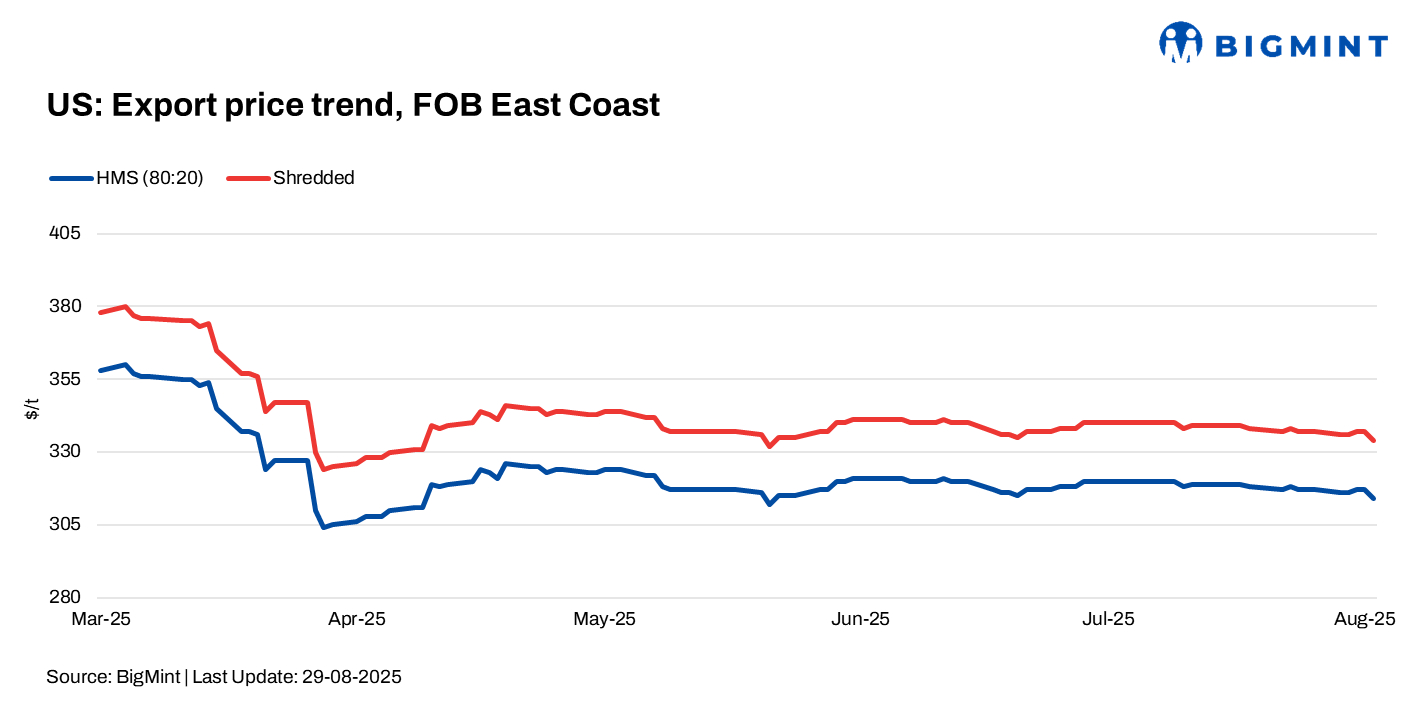

US ferrous scrap export prices softened and fell by $3/t w-o-w, pressured by weak buying interest from major importers, even as select markets showed pockets of activity amid varying local conditions.

FOB assessments (US East Coast, bulk)

- HMS 80:20 – $314/t, down by $3/t w-o-w.

- Shredded – $334/t, down by $3/t w-o-w.

Updates on key importers

Turkiye: Turkiye’s demand for US-origin ferrous scrap remained muted this week, with deep-sea import prices holding largely stable w-o-w. Limited buyer interest and weak sentiment under subdued trading kept fresh bookings minimal.

Factors shaping Turkish scrap demand

- Weak demand, with both buyers and sellers avoiding negotiations

- Pressure for lower prices as focus shifts to October shipments

- Major bookings for September are expected to be complete by next week.

Despite stable prices providing temporary support, mills remained cautious, awaiting clearer direction for September shipments.

Bangladesh: Demand for US-origin scrap in Bangladesh remained weak, as mills avoided bulk bookings amid monsoon rains and sluggish construction. A rare bulk deal of 30,000 t of US West Coast HMS was concluded at $352/t CFR for October shipment, but payment hurdles and currency pressure continue to limit fresh demand.

Vietnam: Demand for US-origin scrap in Vietnam showed limited improvement, with prices edging up w-o-w. HMS 80:20 bulk was assessed at $338/t CFR, while offers rose to $340-345/t amid cautious seller sentiment. Bids followed, firming to $330-335/t.

Despite firmer prices, demand stayed muted due to the holiday slowdown and a weaker VND. Market participants noted that economic stimulus and project acceleration by the government could support scrap demand in the medium term.

US-origin HMS 80:20, bulk – CFR assessments

- Turkiye – down by $1/tw-o-w at $345/t.

- Vietnam – up by $5/t w-o-w at $338/t.

- Bangladesh – up by $2/tw-o-w at $354/t.

Outlook

US-origin scrap demand is expected to remain cautious in the near term. Turkiye’s mills await a clearer price direction for October shipments, Bangladesh faces ongoing seasonal and financial constraints, and Vietnam’s activity may gradually pick up if economic stimulus boosts construction projects.

Leave a Reply