- Turkiye mills hold back amid low rebar demand

- Bangladesh inactive post-Eid, demand stays weak

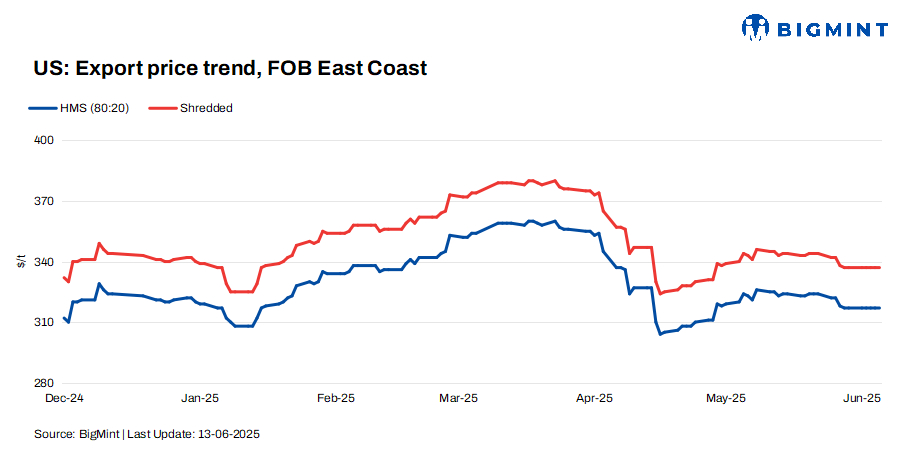

US ferrous scrap export prices remained stable w-o-w, with market sentiment showing early caution but stabilising following a Eid slowdown and sluggishnes in key markets like Turkiye, Bangladesh and other Asian regions.

Tariffs drive sentiments

At the start of the new buying cycle, expectations were bearish due to weak finished steel demand, with some predicting a $20/tonne (t) price drop. However, President Trump’s announcement of a 50% steel import tariff (effective 4 June, excluding the UK) helped stabilise both finished steel and scrap prices.

Domestic US market trends

Domestic mills are capping price increases by offering only slight premiums over dockside export prices. With limited alternative supply options, domestic prices are closely tracking bulk export levels.

According to market participants, trade is subdued, largely due to tight scrap availability. Supplies are a little low, so most players aren’t even trying to secure new deals at the moment.

FOB assessments (US East Coast, bulk)

- HMS 80:20 – $317/t, stable w-o-w.

- Shredded – $337/t, stable w-o-w.

Key importers’ updates

Turkiye: Turkish mills maintained a cautious approach this week, avoiding new bookings of US-origin HMS 80:20 scrap despite offers remaining steady at around $340-345/t CFR. Tradable levels slipped to $335-340/t CFR as mills placed counterbids closer to $330/t CFR, citing poor rebar demand and tight margins.

US exporters saw limited participation, while European sellers pushed similar offers but faced resistance as well. With no immediate signs of a rebound in finished steel demand, deep-sea scrap activity is likely to stay limited unless prices drop further.

Factors limiting buying interest:

- Post-Eid recovery in rebar demand remained sluggish

- Mills are unwilling to book unless offers fall to $325-330/t CFR

- Persistent economic pressures and low export sales restrain buying

Bangladesh: Imported scrap demand in Bangladesh remained muted this week. The ongoing Eid holidays kept most mills inactive, delaying fresh bookings and limiting trade activity.

Only one major Chattogram-based mill booked a Kanto cargo in the $345-350/t CFR range, marking the first bulk deal post-Eid. However, interest in US bulk remains limited due to price sensitivity and cash flow concerns across mills.

Market participants said operational and financial challenges continue to weigh on demand, particularly in Dhaka, where some mill closures are expected. Without a pick-up in finished steel demand, US-origin scrap buying is expected to remain absent.

Vietnam: Demand for US-origin scrap in Vietnam saw a mild pick-up this week as prices edged up, supported by firmer offers from suppliers, though actual buying interest remained limited due to cautious mill sentiment.

Offer levels for US bulk cargoes were heard at round $350-360/t CFR, while bids hovered closer to $340-350/t, indicating a persistent gap in buyer-seller expectations. Vietnamese mills remain wary of booking large volumes. Regional scrap availability is tightening as more Japanese and Korean material flows toward India.

US-origin HMS 80:20, bulk

- CFR Turkiye down by $3/t to $338/t.

- CFR Vietnam up by $5/t to $340/t.

- CFR Bangladesh inched stable to $375/t.

Outlook

Looking ahead, the summer outlook remains uncertain. Possible shifts in US trade policy could push the domestic scrap market either way. For now, market participants are holding off on predictions and waiting for clearer signals.

![]()

Leave a Reply