- Turkiye instability weighs on trade, limits scrap demand

- Post-Eid rebound likely amid improved trade sentiment

US ferrous scrap export offers remained largely stable, inching up by a mere $1/t w-o-w amid Turkiye’s political unrest and the Ramadan slowdown. Market activity in Turkiye, Bangladesh, and Pakistan has temporarily slowed, further limiting the trade momentum.

A market participant noted, “Turkiye, a key buyer of US scrap, has seen mills pause purchases due to political tensions, currency volatility, and weak steel sales.”

Despite the uncertainty, US exporters maintained firm offers at $385-390/t CFR.

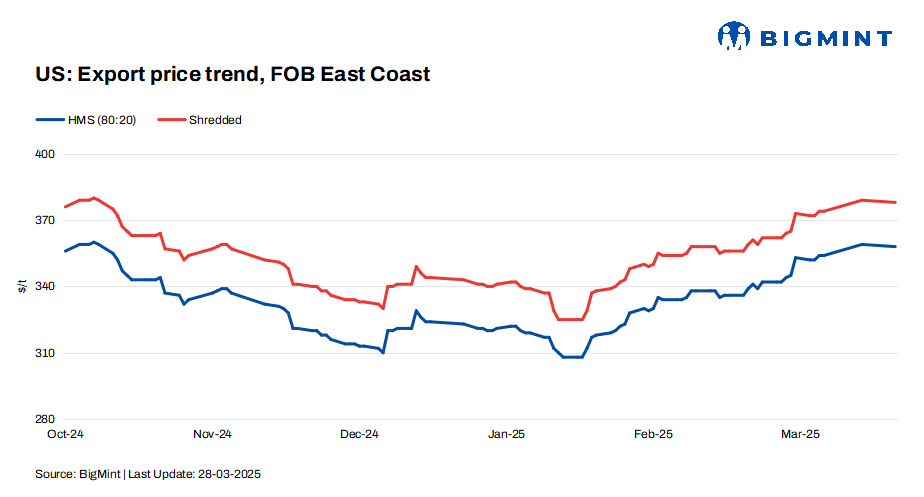

FOB assessments (US East Coast, bulk)

- Shredded were down by $1/t w-o-w to $378/t

- HMS 80:20 decreased by $1/t w-o-w to $358/t.

CFR assessments (bulk)

- HMS 80:20 was at $381/t CFR Turkiye, stable w-o-w.

- HMS 80:20 stood at $368/t CFR Vietnam, up by $3/t w-o-w.

- HMS 80:20 was at $384/t CFR Chattogram, up by $6/t w-o-w.

Updates on key importers

Turkiye: Demand for US-origin scrap in Turkiye remains subdued as buyers resist higher offers amid weak rebar sales and ongoing domestic uncertainties.

A Baltic supplier noted, “Turkish mills are aiming to keep scrap prices above $370/t next week, but US and other suppliers are unlikely to agree. Buyers are pushing for lower prices, resisting high offers. Prices are expected to hover at $378-383/t for EU, Baltic, and US cargoes, while European sellers are still targeting $385-390/t.”

US scrap suppliers are holding firm on prices, supported by slow domestic collection and loading shortages, limiting any downward movement. Buyers see acceptable levels at $374-375/t CFR, though only a few are willing to pay up to $378/t CFR, while US exporters remain steadfast at $385-390/t CFR.

Bangladesh: Demand for US-origin scrap in Bangladesh remains weak as mills struggle with subdued steel demand during Ramadan and sluggish infrastructure activity. Mills are operating below capacity, with some accepting lower margins to sustain cash flow.

US West Coast bulk HMS 80:20 offers stand at $380-385/t CFR, but buying interest remains limited. Domestic scrap prices stay elevated due to restricted LC approvals, though the upcoming 10-day Eid market halt and lack of new LC openings may put downward pressure on prices.

Vietnam: Demand for US-origin scrap in Vietnam showed slight improvement owing to higher offers from supplier. However, market activity remained sluggish due to slow construction recovery, delayed government spending, and postponed infrastructure projects. Offers for US-origin deep-sea scrap inched up w-o-w to $365-370/t CFR.

Outlook

US ferrous scrap exports to Turkiye may face challenges in early April due to political instability and the post-Ramadan market slowdown. A weaker lira could raise import costs, prompting mills to explore cheaper alternatives like Chinese and Malaysian billets, reducing US scrap demand. Around 3-4 cargoes are needed by Turkish mills for April but with 15 offers on the table, many may shift to May, increasing pressure on prices. Asian bulk importers continue to remain less focused on US scrap, eyeing the US-Canada trade stand-off.

Leave a Reply