- Turkish mills delay purchases awaiting price clarity

- Bangladesh demand slows during Eid holidays

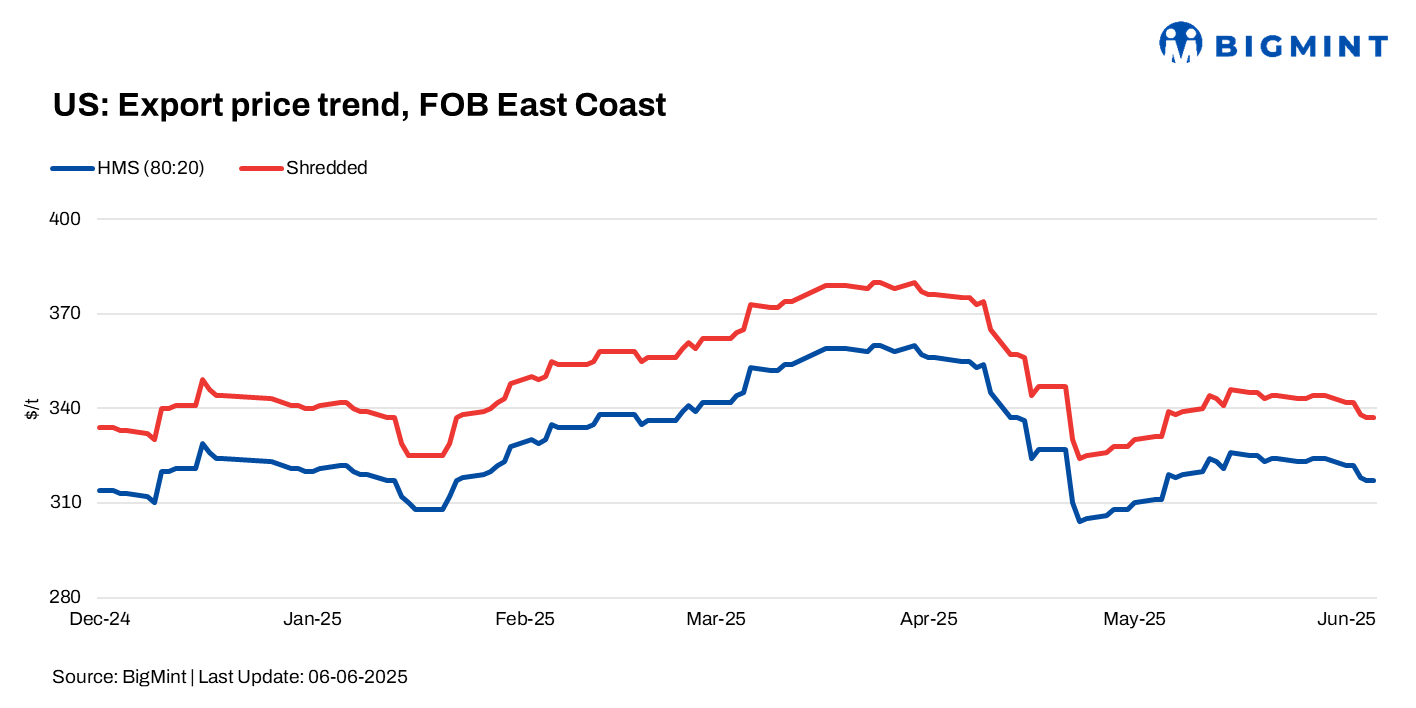

BigMint’s US ferrous scrap export prices fell $7/t w-o-w. US alternative iron prices (pig iron) held steady as buyers waited for clarity on tariffs and market trends.

Domestic market

Expected cuts in Brazilian pig iron supply may support prices amid weak scrap trade.

Mills are securing June scrap on a tentative basis, but many sellers and buyers are holding back, anticipating clearer price direction.

Market uncertainty driven by mixed views on demand, capacity, and tariff impacts is slowing trade.

Inventory levels differ regionally: some mills report high stockpiles, while others, especially in the South, see tightening supplies. Despite this, many expect prices to ease in June.

FOB assessments (US East Coast, bulk)

- HMS 80:20 – $317/t, fell by $7/t w-o-w.

- Shredded – $337/t, fell by $7/t w-o-w.

Key importers updates

Turkiye: Demand for US-origin scrap in Turkiye weakened this week as mills paused bookings amid weak finished steel demand and the upcoming Eid al-Adha holidays. With cash flow concerns and high interest rates, most mills preferred to stay on the sidelines and reassess post-holiday.

US-origin HMS 80:20 offers stood around $340-344/t CFR, with tradable levels dipping to $338-340/t CFR, reflecting broader market pressure. If rebar demand doesn’t recover soon, US scrap suppliers may need to lower offers further to keep material moving, especially as inventory risks grow on the seller side.

Factors limiting buying interest

- Rebar sales remain sluggish in both domestic and export markets.

- Turkish mills are delaying purchases as they anticipate a drop in price.

- Currency volatility and high seller costs cap a sharp price decline.

Bangladesh: Demand for US-origin HMS 80:20 scrap in Bangladesh softened noticeably in early June due to the extended Eid holidays, which slowed market activity and limited fresh purchases.

A US-origin HMS 80:20 cargo was reportedly sold to Chattogram on Monday at $373/t CFR. Market sources suggest the buyer is likely one of the major five mills.

Prices edged down slightly to $375/t CFR, down w-o-w, pressured by rising freight costs and cautious buyer sentiment.

Importers remain hesitant, postponing procurement decisions as they await clearer market signals on pricing and steel demand, likely keeping trading subdued through mid-June.

Vietnam: Demand for US-origin ferrous scrap in Vietnam remained subdued w-o-w, with HMS 80:20 bulk prices assessed at $335/t CFR and offers at $340-345/t CFR. However, buying interest was limited due to the availability of cheaper billets and stable downstream steel prices.

Vietnamese steelmakers showed stronger demand for imported billets from Indonesia, booking around 80,000 t at $430/t FOB. Yen fluctuations reduced Japanese scrap offers, prompting buyers to wait before making new purchases.

US-origin HMS 80:20 ,bulk

CFR Turkiye dropped $7/t to $340/t,

CFR Vietnam down $5/t to $335/t,

CFR Bangladesh inched down by $1/t to $375/t.

Outlook

Market uncertainty and weak steel demand are likely to keep buying cautious. Without an uptick in rebar consumption in Turkiye and Bangladesh or clearer tariff guidance, prices may face further downward pressure in the near term.

![]()

Leave a Reply