- Bangladeshi mills wary, wait for clearer direction

- Weak Turkish demand to further reduce prices

BigMint’s US ferrous scrap export index dropped by $22/tonne (t) this week, resulting in a total decline of $50-60/t since the start of the month. Following this sharp fall, the index hovered at levels last seen in November 2022, around 2.5 years ago.

Amid rising freights, US suppliers offered material at $335/t CFR. However, a Turkish trader stated that sellers sought higher prices following a $3-5/t w-o-w increase in shipping costs.

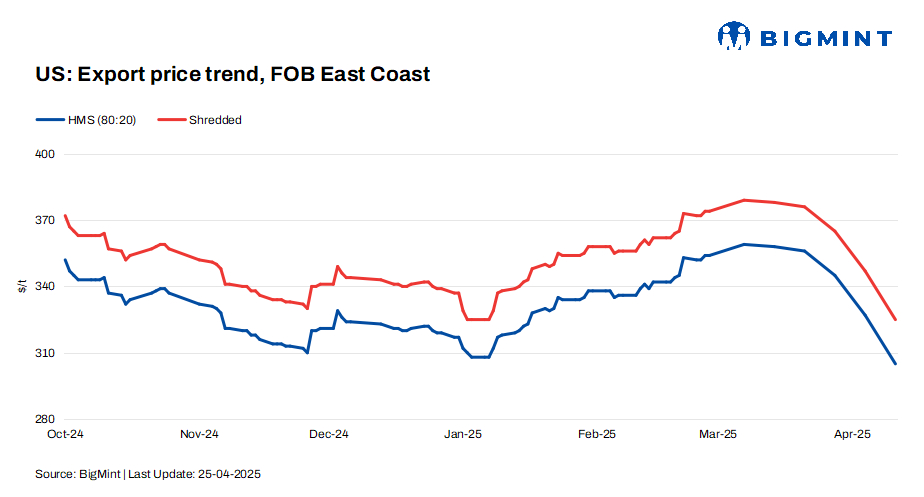

FOB assessments (US East Coast, bulk)

- HMS 80:20 decreased by $22/t w-o-w to $305/t.

- Shredded dropped by $22/t w-o-w to $325/t.

CFR assessments (bulk)

- HMS 80:20 was at $325/t CFR Turkiye, down by $23/t w-o-w.

- HMS 80:20 stood at $350/t CFR Vietnam, down by $10/t w-o-w.

- HMS 80:20 was at $369/t CFR Chattogram, down by $5/t w-o-w.

Updates on key importers

Turkiye: Demand for US-origin scrap in Turkiye remained relatively steady due to its reliable quality and shipping consistency. However, with most May shipment needs already covered, Turkish mills slowed down fresh purchases. This left European yards struggling to find buyers, as recent restocking mainly targeted US and Baltic cargoes.

Offers from the US and Baltic regions were heard mostly at $325-330/t CFR, though Turkish buyers countered with lower bids – one at $315/t CFR for Baltic scrap was reportedly rejected.

Since early April, prices have dropped by $50-60/t amid weak finished steel sentiment and persistent oversupply. Mills continued to restock cautiously, but falling domestic rebar prices added further pressure on scrap import offers.

Bangladesh: Demand for US-origin ferrous scrap in Bangladesh was moderate amid declining global prices and cautious market sentiment. Mills showed limited interest in bulk purchases, preferring to wait for clearer direction as cost pressures persisted and global markets witnessed corrections.

Additionally, sustained pressure from falling deep-sea prices, particularly in Turkiye, continued to influence sentiment across South Asia.

According to a Chattogram-based mill, buyers aimed for lower booking levels, with indicative prices heard at $355-360/t CFR for US or Australian cargoes. Offers for US-origin scrap held at around $365/t CFR, while Singapore-origin bulk was quoted at $370/t CFR.

Another Chattogram-based trader noted that the bulk market was largely inactive this week. HMS from the US West Coast was offered at $350-355/t, but no major deals were closed. While one or two Chattogram-based mills showed interest through inquiries, no purchases were made recently, with the last indication at $360/t. The only confirmed bulk deal was at $350/t CFR Chattogram last week.

Vietnam: Demand for US-origin scrap picked up in Vietnam, as falling prices made imports more competitive than domestic material. Container deals were heard at $300-305/t CFR. With bulk HMS bids at around $340-345/t and deals at $345-350/t, mills took advantage of lower deep-sea offers despite lingering tariff concerns.

Outlook

US ferrous scrap export prices are likely to remain under pressure in the near term, weighed down by sluggish global steel demand, elevated freight costs, and subdued buying interest from major markets such as Turkiye and Bangladesh. Market sentiment stays bearish, with limited bulk activity and growing expectations of further price corrections.

Leave a Reply