- Turkish mills resist high prices amid poor rebar sales

- Vietnamese mills make lower bids on trade uncertainty

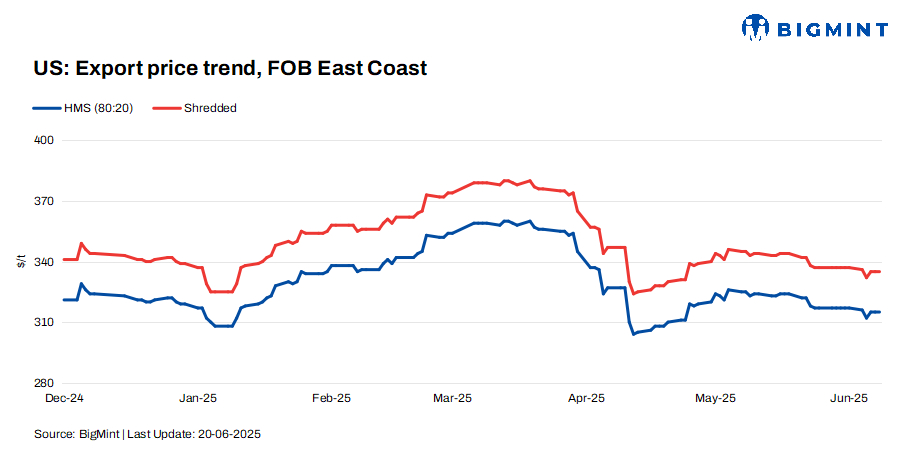

US ferrous scrap export prices declined slightly by $2/tonne (t) w-o-w, reflecting continued buyer resistance and subdued demand across key markets such as Turkiye, Vietnam, and Bangladesh, as mills remained cautious amid weak finished steel sales.

FOB assessments (US East Coast, bulk)

- HMS 80:20 -$315/t, down by $2/t w-o-w.

- Shredded -$335/t, down by $2/t w-o-w.

US-origin HMS 80:20, bulk – CFR assessments

- Turkiye – up by $4/t to $342/t.

- Vietnam – down by $5/t to $338/t.

- Bangladesh – down by $5/t to $370/t.

Key importers’ updates

Turkiye: Turkish mills continued to resist US-origin HMS 80:20 offers, which held firm at $340-343/t CFR, citing weak rebar sales and limited end-user demand. While prices briefly ticked up mid-week, tradable levels remained in the $335-338/t CFR range. Sellers from the US maintained their stance, supported by strong domestic markets and tight availability.

A source at a major trading house stated, “Heard over 20 vessels might be needed for July and early August shipments, given how slow bookings have been so far. But mills are holding back like it’s a matter of survival – they are not touching anything above $340/t CFR.”

Kardemir’s rebar sales, following a price cut, indicated some existing demand. However, weak sales volumes kept other mills cautious, prompting them to hold off deep-sea US scrap purchases unless offers drop further.

Factors limiting buying interest

- US sellers were reluctant to reduce offers below $345/t CFR due to tight supply.

- Rebar demand remained weak in both domestic and export markets.

- Mills faced narrow margins and limited inventory build-up.

Bangladesh: Bangladesh’s appetite for US-origin ferrous scrap continued to wane, with only a few trades concluded in the past week.

Market activity was muted, with fewer participants actively trading. Sellers offered discounts to attract buyers, but mills remained cautious, assessing their production plans amid declining steel demand and limited liquidity.

While Japanese scrap cargoes carried a $10-15/t premium over Vietnamese bookings into Chattogram, the US-origin bulk market remained clouded by uncertainty due to escalating tensions in the Middle East, making future pricing and availability less predictable for Bangladeshi buyers.

Vietnam: US-origin HMS 80:20 bulk prices were down w-o-w, amid muted buying activity and weak downstream demand.

Suppliers reduced offers to $350-355/t CFR, but buyers stayed cautious, submitting bids at around $335-340/t CFR. The lack of urgency from mills and persistent price uncertainty continued to dampen trade momentum.

Adding to the hesitation were the ongoing US-Vietnam trade talks. Despite some progress in early June, unresolved issues, such as Vietnam’s reliance on Chinese inputs, threaten future trade dynamics. With a 46% reciprocal tariff looming in July, both sides are pushing for more dialogue to avoid disruptions.

Outlook

Near-term sentiment stays cautious as mills push back against high offers amid persistent rebar and hot-rolled coil (HRC) demand weakness. A trader noted, “Turks do need scrap, but unless it drops below $340/t CFR, they are just not biting. That said, if fresh orders come in, things could flip fast, and they might rush to book.”

Pockets of regional demand exist from buyers such as Bangladesh and Vietnam, but a broader recovery hinges on downstream momentum, easing trade uncertainty.

Leave a Reply