- Warm weather boosts supply, pressuring domestic tags

- Turkish mills delay bookings amid weak steel demand

BigMint’s US ferrous scrap export index slipped by $10/tonne (t) this week, with most April delivery negotiations concluded at lower price in the domestic market. Midwest steelmakers were able to secure significantly lower prices m-o-m, driven by mini-mills leveraging the ongoing supply surplus.

Additionally, this week witnessed the steepest m-o-m drop in Midwest shredded scrap prices since the $40-50/t decline recorded in March 2024. Shredded scrap moved into surplus, as warmer weather across the Northern Hemisphere since mid-March led to increased scrap collection and a pick-up in demolition work.

A trader noted, “Tariffs had little effect on the scrap market, as shipments from Canada and Mexico were not impacted. Given the historically narrow spread between shredded and busheling, there was clear potential for that gap to widen.”

Buyers are hesitant, and exporters are cautious, especially with the potential impact of the tariffs in Asia and the Middle East.

“Tariffs are the wildcard…they’re disrupting the flow of decisions,” said one participant.

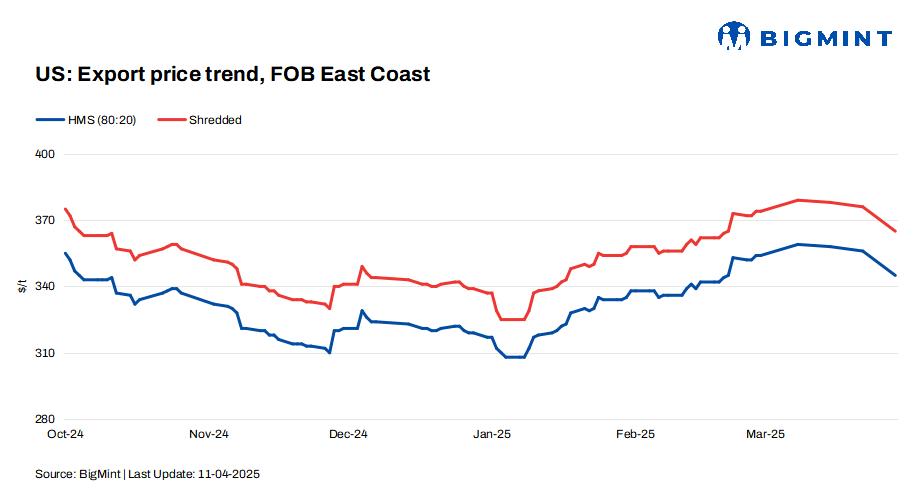

FOB assessments (US East Coast, bulk)

- HMS 80:20 decreased by $10/t w-o-w to $345/t.

- Shredded dropped by $10/t w-o-w to $365/t.

Prices have dropped to levels last seen in early March 2025.

CFR assessments (bulk)

- HMS 80:20 was at $366/t CFR Turkiye, down by $13-14/t w-o-w.

- HMS 80:20 stood at $362/t CFR Vietnam, down by $6/t w-o-w.

- HMS 80:20 was at $380/t CFR Chattogram, down by $4/t w-o-w.

Updates on key importers

Turkiye: Demand for US-origin ferrous scrap in Turkiye weakened significantly this week, as mills pushed back on elevated offers, leading to a sharper-than-expected price correction.

Turkish mills, facing sluggish finished steel sales and rising energy costs, held off on deep-sea bookings to avoid further inventory build-up. Limited export demand and subdued domestic consumption left mills cautious, prompting many to explore more cost-effective short-sea and billet alternatives instead of locking in fresh US-origin scrap cargoes.

Mills are expected to return for restocking soon, as inventories remain thin – but only if prices keep with the bearish trend. Until then, oversupply and lack of urgency may keep US-origin scrap demand subdued in the near term.

Bangladesh: Demand for US-origin HMS (80:20) scrap in Bangladesh eased after Eid, with prices slipping. Mills remained selective in bookings, opting to assess market conditions before committing to bulk deals.

Domestic scrap prices also declined due to muted activity last weekend. However, improved rebar sales this week lifted buying interest slightly, with some mills increasing rebar prices by BDT 500/t ($4/t) to support margins.

While sentiment is recovering, mills are yet to resume full-scale scrap procurement, keeping US-origin bulk buying in check.

Vietnam: Demand for US-origin scrap in Vietnam weakened, as the dong depreciated sharply after tariff tensions with the US, reducing mills purchasing power. Buying indications dropped to below $360/t CFR, while suppliers shifted focus to Bangladesh amid better buying interest.

Outlook

The US ferrous scrap export market is expected to stay soft in the near term, weighed down by weak mill demand and uncertainty over reciprocal tariffs. Buyer sentiment remains low, with only limited optimism from brokers eyeing regional or export-driven support.

Buying confidence is fragmented across domestic regions, though stable inventories suggest no immediate supply pressure.

While overall sentiment is cautious, rising pig iron import costs – due to new duties on Brazilian and Ukrainian material – could lend partial support to scrap prices, particularly for flat-rolled mini-mills.

Leave a Reply