- Scrap demand moderate, mills wait for clarity

- Market to remain slow, may rebound next week

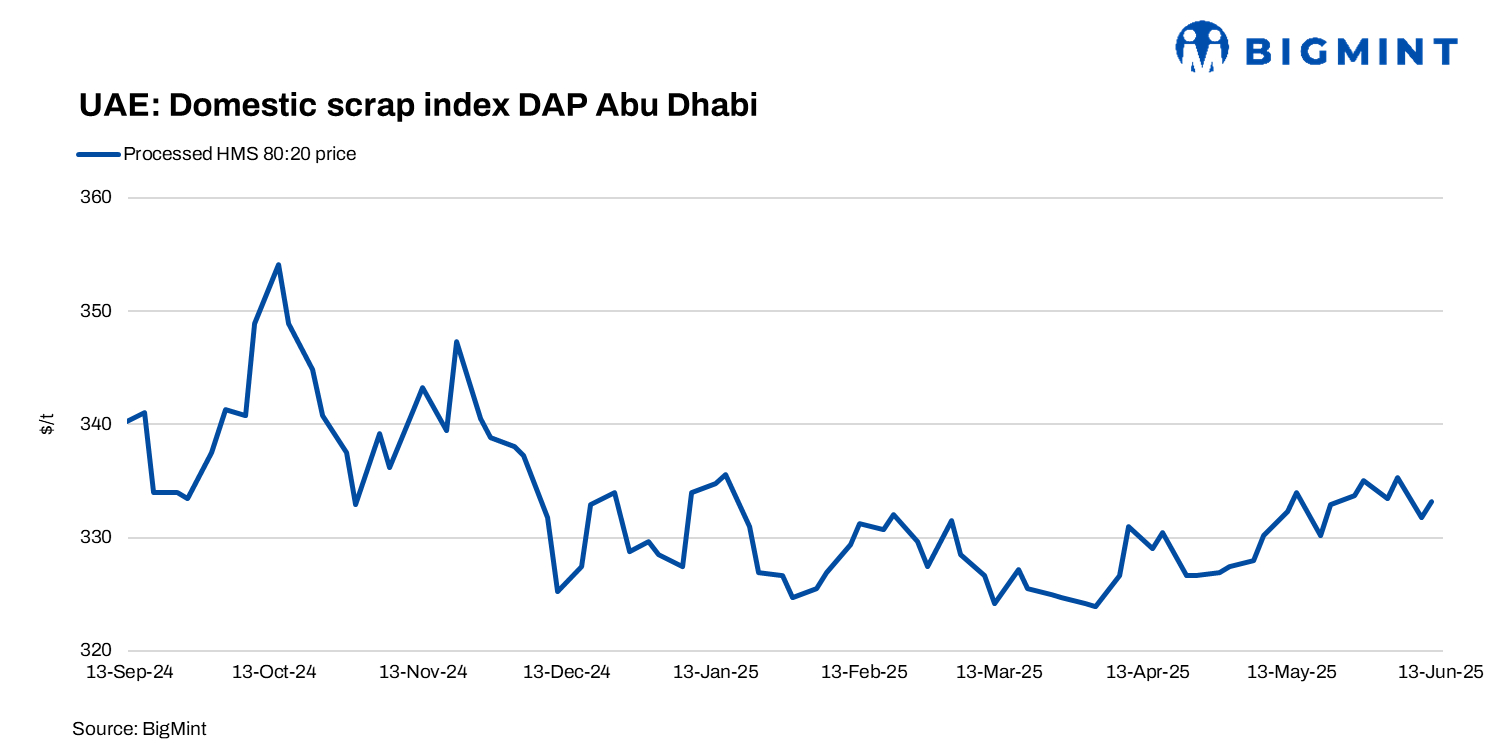

BigMint’s UAE domestic processed HMS index inched down by AED 8/t ($2/t) w-o-w to AED 1,224/t ($333/t) amid slow to moderate inquiries from mills. The market is not active right now and is expecting a slowdown but could pick up next week.

A few mills preferred buying at current offers, and the rest are keeping an eye on recent political conflicts between Iran and Israel.

As per sources, HMS 80:20 is steady at around AED 1,165-1,170/t ($317-318/t). Fabrication scrap was around AED 1,250-1,255/t ($340–342/t). Rebar end-cuts traded at close to AED 1,300-1,310/t ($354–357/t). LMS was at AED 850-870/t ($231–237/t), and processed HMS at AED 1,220/t ($332/t) DAP Abu Dhabi.

Export market

UAE-origin shredded scrap are heard at $375-380/t, and HMS-PNS mix is expected to be $362-366/t CFR Qasim.

HMS (80:20) spread

The average spread between HMS 80:20 from Europe and the UAE’s processed HMS 80:20 narrowed w-o-w to approximately $6-10/t CFR Nhava Sheva. Prices of imported HMS on the west coast of India stood at $340-342/t CFR, while the UAE’s processed HMS tags were at $332-333/t DAP Abu Dhabi.

UAE HRC market active

The UAE HRC market rebounded post-holiday, but a low-priced Russian booking sparked concern. An India-linked buyer secured Russian HRC from NLMK at $450-455/t CFR Jebel Ali for August shipment. While finalised in India, UAE buyers remain wary of payment and sanction-related risks.

Separately, a UAE re-roller booked 10,000 t of Saudi SAE 2-3 mm HRC at $550-555/t delivered Abu Dhabi, likely due to shipment delays. Chinese mills are offering $472-475/t CFR for August, though no firm deals have been reported.

Japanese mills floated $500/t CFR for August, up $6-10/t w-o-w, but potential shutdowns may limit traction. Overall, the market is active but cautious, shaped by origin risk and urgency.

Jindal SAW to invest $118 m in GCC expansion

India’s Jindal SAW will invest $118 million to expand in the GCC, targeting the oil and gas sector. The company will set up a $105 million pipe manufacturing facility in Abu Dhabi with 300,000 tonne per annum capacity, to be completed in three years.

In Saudi Arabia, Jindal SAW Holdings FZE has entered two JVs: a $10 million HSAW pipe project with Buhur for Investment Company (within two years), and a $3 million ductile iron pipe unit with RAX United Industrial Company (12–18 months). Jindal will hold a 51% stake in both. The company’s total installed capacity in India exceeds 2 mnt/year.

Outlook

The UAE scrap and HRC markets are expected to remain cautious in the near term amid geopolitical uncertainties and subdued demand. Domestic scrap prices are holding steady with limited mill-side buying, while buyers remain watchful of tensions in the Middle East. Overall, trade may stay rangebound in the short term.

![]()

Leave a Reply