- Major scrap buyer withdraws booking; market expects lower bid levels

- Muted rebar demand and tighter liquidity pressure procurement

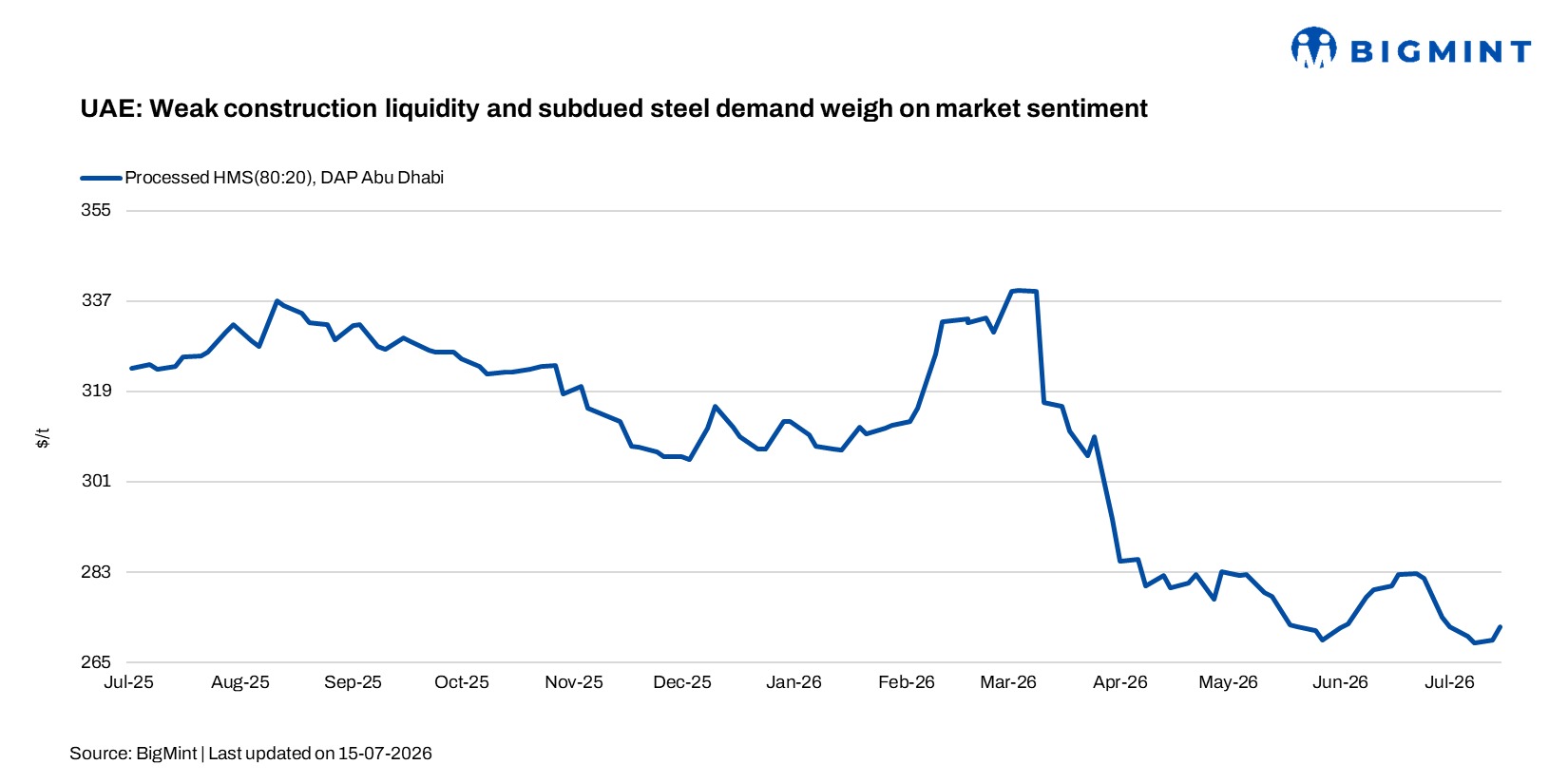

According to BigMint’s assessment, processed HMS (80:20) scrap increased by AED 12/t ($3/t) week on week to AED 1,000/t ($272/t) DAP Abu Dhabi from AED 988/t ($269/t) last week. The increase reflected firmer workable levels of around AED 990-1,000/t ($270-272/t) DAP prevailing during the early part of the assessment period.

However, buying sentiment weakened toward the end of the week as mills slowed procurement and one of the country’s largest scrap consumers temporarily withdrew from the market. Market participants now expect domestic buying prices to soften by a further AED 20-30/t ($5-8/t) if subdued demand and cautious procurement persist.

According to a mill-side source, workable levels for HMS 80:20 processed are currently at AED 975-980/t ($265-267/t) DAP, while shredded scrap is workable at AED 1,025-1,050/t ($279-286/t) DAP.

Current indications place processed HMS at AED 980-1,000/t ($267-272/t) DAP Abu Dhabi, while simple HMS is heard at AED 930-940/t ($253-256/t). Shredded scrap was last traded at AED 1,050-1,070/t ($286-292/t) DAP. Across the broader market, HMS 80:20 is heard at AED 880-900/t ($240-245/t), HMS Super at AED 920-940/t ($251-256/t), and fabricated scrap at AED 1,030-1,040/t ($281-283/t), all delivered and excluding 5% VAT.

Despite the export ban keeping more scrap within the domestic market, mills have shown little urgency to replenish inventories, preferring to purchase only against immediate production requirements. “Material is available, but mills are buying only what they need. The market has turned quieter over the past few days, and most participants expect another round of price corrections,” a UAE-based scrap trader told BigMint.

Demand-side conditions remain equally challenging

Liquidity across the UAE’s private construction sector has tightened as residential property transactions continue to slow. According to REIDIN, off-plan residential transaction values fell 12% y-o-y to AED 168.2 billion in H1 2026, while ready property transactions declined 25% to AED 57.5 billion. Slower transaction activity has reduced cash circulation across the construction supply chain, delaying payments to contractors and limiting working capital available for steel purchases.

“Projects are still moving, but payments are slower, and everyone is protecting cash. Buyers are purchasing only against confirmed requirements instead of building inventories,” a UAE-based steel distributor said.

As a result, mills have struggled to sustain finished steel price increases, while distributors continue to avoid speculative buying. Market participants said liquidity, rather than scrap availability, has become the dominant factor shaping procurement decisions, keeping raw material demand subdued despite ongoing infrastructure and government-backed projects.

Domestic and imported rebar prices in the UAE remained stable during the week ended 17 July as buying activity slowed after strong bookings in late June. Meanwhile, imported billet offers widened to $570-610/t CPT Jebel Ali, supported by higher freight rates, shipping disruptions and rising marine insurance costs. East Asian and Chinese billet offers were heard from $555-560/t CPT, although workable levels were closer to $570-575/t, while GCC-origin billet was offered at up to $610-620/t CPT.

Regional sentiment softened

In neighbouring Saudi Arabia, steelmakers have been seeking lower domestic scrap prices amid weak steel margins and sluggish finished steel demand. However, Hadeed has maintained its second-half July procurement prices at SAR 2,070/t ($552/t) for premium heavy melting scrap, SAR 2,060-2,070/t ($550-552/t) for shredded scrap and SAR 2,000/t ($533/t) for HMS. Oversize scrap is priced at SAR 1,500-1,510/t ($400-403/t), while light scrap is at SAR 1,400-1,410/t ($373-376/t). Despite Hadeed’s steady buying prices, market participants said procurement sentiment across the Gulf remains cautious, offering limited support to UAE scrap prices and reducing opportunities for suppliers to divert material into neighbouring markets.

Outlook

Although BigMint’s benchmark strengthened this week, reflecting firmer workable levels during the early part of the assessment period, buying sentiment has since softened as mills shifted to a hand-to-mouth procurement strategy. Market participants expect mills to continue testing lower bid levels over the coming weeks, supported by comfortable domestic scrap availability and limited pressure to replenish inventories. Unless demand from the long steel sector improves or regional procurement activity strengthens, suppliers may face increasing pressure to negotiate at lower workable levels.

Leave a Reply