- Mills largely on sidelines; buying strictly need-based

- Rising freight, handling costs tightening mill margins

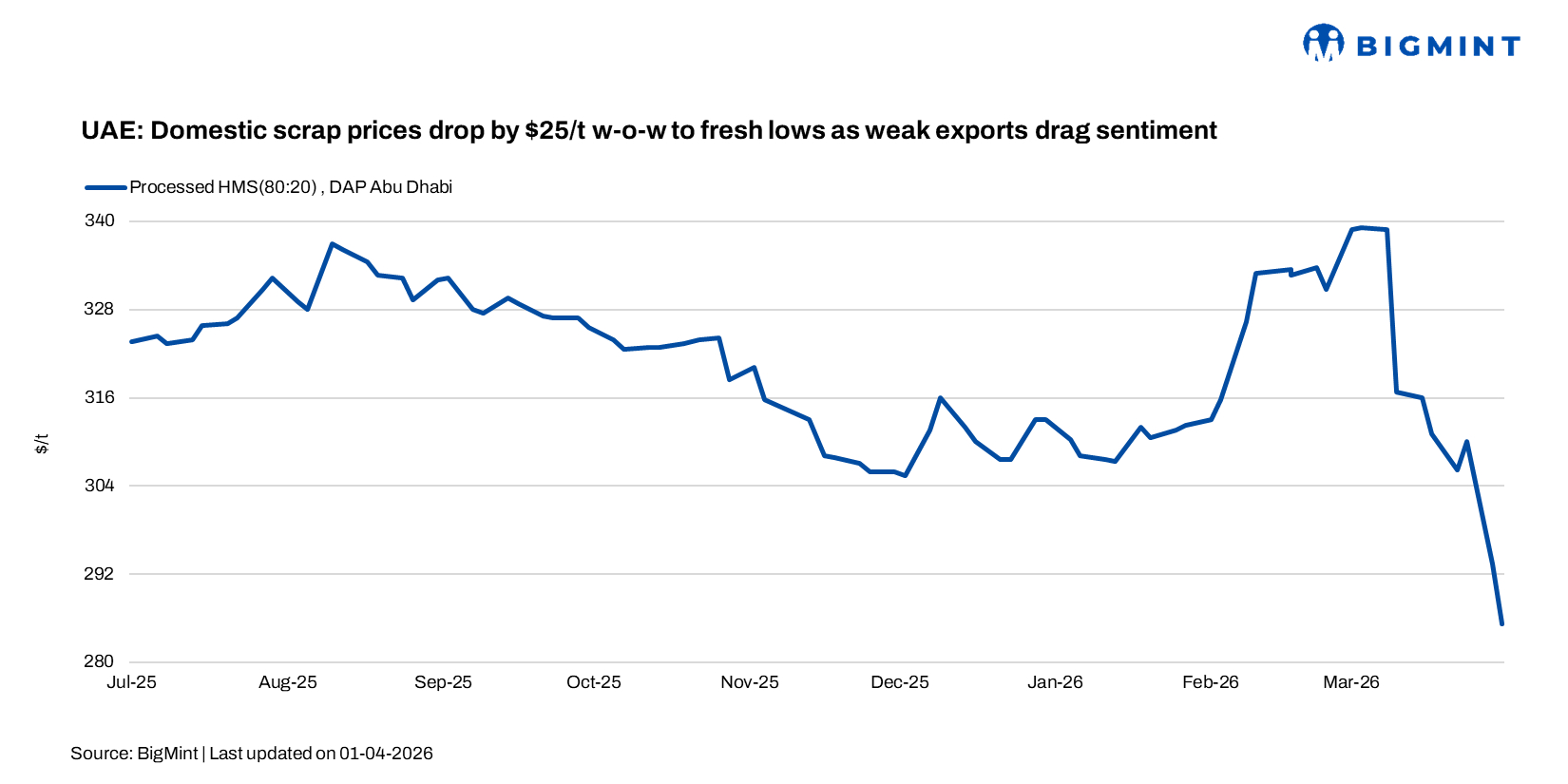

The UAE scrap market continued to face pressure in the last week of March, with prices softening to record lows as export demand remained weak. Market sentiment stayed subdued, with mills showing limited interest in fresh bookings amid ongoing uncertainty, including recent disruptions in Abu Dhabi.

BigMint’s domestic HMS 80:20 (processed) scrap index declined by AED 91/t ($25/t) w-o-w to AED 1,048/t ($285/t) DAP Abu Dhabi in the week ending 1 April, marking its lowest level since the assessment began on 11 October 2023, as persistently weak export demand continued to weigh on market sentiment.

A UAE-based trader said the domestic scrap market is still under pressure, with processed HMS heard around AED 1,040-1,050/t ($281-284/t), excluding VAT. He noted that mills are holding back purchases due to limited order visibility.

- HMS 80:20: AED 1,015-1,030/t ($274-278/t)

- PNS (unprocessed): AED 1,050-1,070/t ($284-289/t)

- HMS 80:20 (processed): AED 1,040-1,055/t ($281-285/t)

- Fabrication scrap: AED 1,100-1,150/t ($297-311/t)

- LMS: AED 825-840/t ($223-227/t)

Meanwhile, a Dubai-based supplier noted that prices remain under pressure, with processed HMS at AED 1,050-1,080/t ($284-292/t) and shredded at AED 1,170-1,200/t ($316-324/t). He added that buying interest remains limited, as mills stay cautious amid ongoing uncertainty following recent drone strike disruptions at the Emirates Global Aluminium (EGA) facility in Abu Dhabi.

Mills are mostly staying out of the market for now, taking a wait-and-watch stance. With exports not moving and steel demand still slow, buying is limited and only happening when necessary.

Logistical disruptions are continuing to push steel prices higher in the UAE, as mills face rising supply chain costs and increasing uncertainty. Producers are struggling to manage both internal and external cost pressures, with disruptions around the Strait of Hormuz significantly impacting raw material inflows.

Mills are finding it difficult to absorb these costs, as alternative routes, such as via Oman, add an extra $35-40/t, while local transportation costs have also increased. At the same time, delays and inefficiencies in multi-modal logistics are creating further bottlenecks.

Although demand remains relatively strong, supply constraints are making planning difficult beyond the short term. As a result, some producers have already increased rebar prices by $45-55/t and withdrawn discounts to offset rising costs.

Outlook

The market is likely to stay under pressure in the coming week, with mills continuing to buy only on a need basis due to weak export demand. However, ongoing logistical disruptions and higher costs are expected to prevent any sharp price drop. Any upward movement will depend on how supply constraints evolve and whether demand shows signs of improvement.

Leave a Reply