- Exporters cautious amid weak South Asian demand

- Need-based trades seen; no aggressive restocking yet

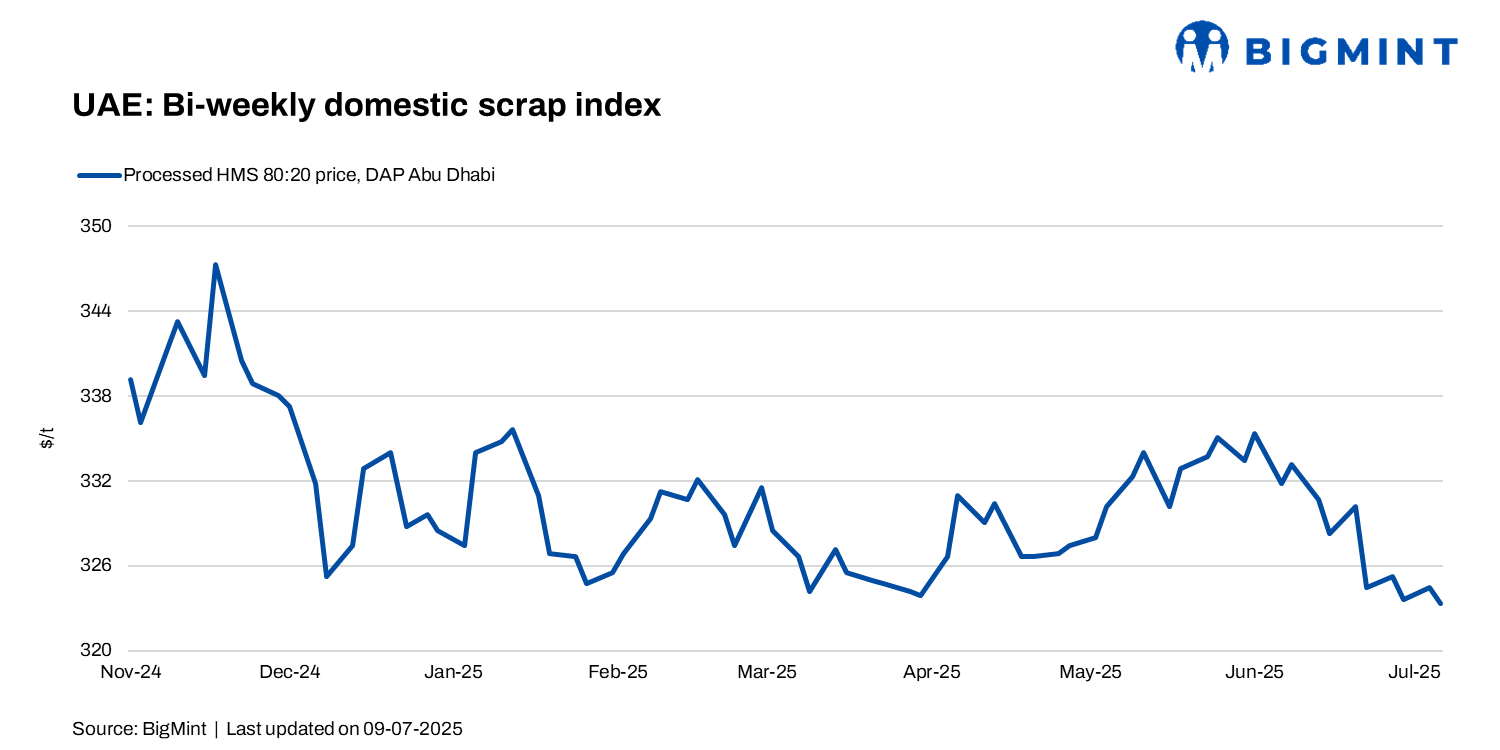

BigMint‘s UAE domestic processed HMS index remained largely stable w-o-w, inching down by AED 1/t ($0.3/t) w-o-w to AED 1,188/t ($323/t), amid ample local availability and weak demand from import destinations such as India and Pakistan. Additionally, most purchases were to fulfil immediate needs, and no aggressive restocking was observed this week.

On a DAP basis (excluding VAT), light melting scrap (LMS) was quoted at AED 840-900/t ($229-245/t), while HMS 80:20 and HMS processed were both assessed in the range of AED 1,150-1,180/t ($313-322/t), while shredded and PNS stood at AED 1,240-1,260/t ($338-343/t). LMS 50:50 (mixed) stood at AED 1,020-1,040/t ($278-282/t), fabrication was priced at AED 1,250-1,270/t ($341-346/t), and end-cutting inched up to AED 1,280-1,300/t ($349-354/t).

Export market scenario

Shredded offers from the UAE remained firm at $388-390/t CFR Qasim, while HMS-PNS mixed cargoes were quoted at $380-382/t CFR. Pure GI bundles were heard at around $371/t CFR, and HMS 80:20 stood at $360/t CFR.

On a deal-level basis, the export market remained limited, with a deal for 500 t of LMS concluded to Pakistan from the Middle East at $330/t CFR Qasim. Demand from South Asia was muted.

HMS (80:20) spread

The average spread between HMS 80:20 from Europe and the UAE’s processed HMS 80:20 widened w-o-w to approximately $10-12/t CFR Nhava Sheva. Prices of imported HMS on the west coast of India stood at $334-335/t CFR, while the UAE’s processed HMS tags were at $323-324/t DAP Abu Dhabi.

UAE billet market updates

In the domestic market, around 2,000-2,500 t of 150-mm 3sp billets were traded at $490-495/t delivered to a UAE re-roller, while another 5,000 t were booked at $485-490/t delivered to Abu Dhabi by a merchant billet producer for prompt shipment.

Outlook

UAE scrap prices are likely to remain range-bound amid subdued demand from South Asia and steady domestic availability. Mills may continue to buy cautiously, with a limited appetite for higher offers in the near term.

Leave a Reply