- Wire rods, billets see weak demand

- Scrap prices steady in export market

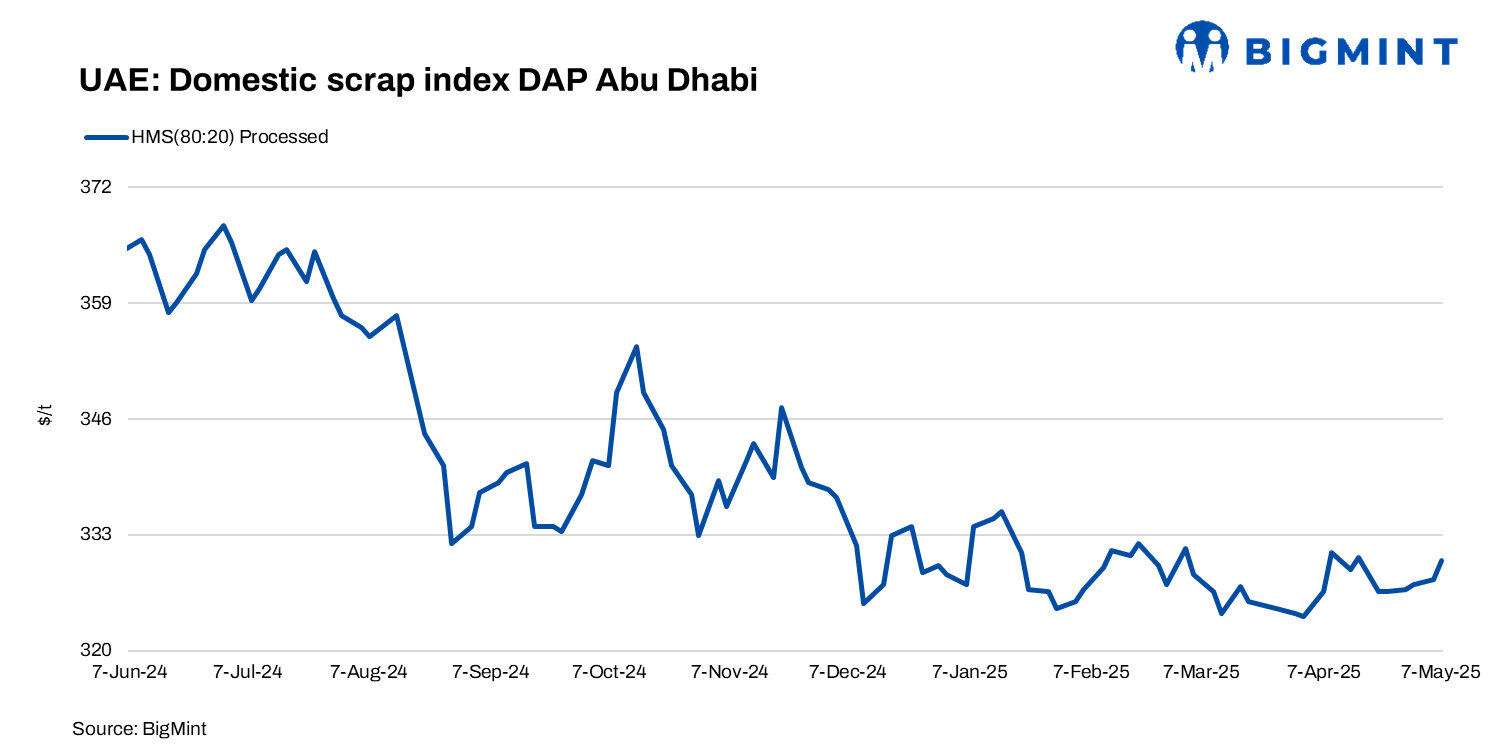

The UAE’s domestic ferrous scrap price saw slight gains over the past week amid tight supply and a rebound in global offers, especially in Turkiye, after a continued drop in prices last month.

Market sentiment has improved, and mills are back to buying, said a scrap buyer based in Abu Dhabi. Collection has dropped sharply due to extreme heat, keeping supply tight.

As per market insiders, HMS 80:20 processed traded at AED 1,200-1,220/t ($327-332/t) delivered in the UAE this week on a DAP Abu Dhabi basis.

Offers for processed HMS (80:20) were heard at AED 1,230-1,240/t ($335-338/t) delivered, according to a Sharjah-based trader.

Scrap prices increased this week, even as local UAE rebar dipped, influenced by lower billet and imported rebar prices.

“Mills attempted to lower scrap purchase prices due to a $10-12/t drop in local rebar prices, but suppliers were unwilling to provide materials for less than AED 1,200-1,210/t for processed HMS and AED 1,250/t for shredded,” a UAE-based scrap trade source commented.

Export market scenario

The export market saw moderate activity, although the overall momentum was sluggish. UAE-origin shredded scrap was heard sold at $378-382/t CFR Qasim. Last week, the UAE’s shredded cargo of 1,000-1,500 t was sold at $382-385/t. Although some buyers still bid below $376-378/t, securing deals even at those levels proved difficult.

HMS (80:20) spread

The average spread between HMS 80:20 from Europe and the UAE’s processed HMS 80:20 remain largely stable w-o-w at approximately $18-20/t CFR Nhava Sheva. Prices of imported HMS on the west coast of India stood at $350-352/t CFR, while the UAE’s processed HMS tags were at $330-331/t DAP Abu Dhabi.

The UAE wire rod market remained inactive, with limited demand and pressure from cheaper Chinese imports. Chinese wire rods were being offered at $465-485/t CFR Jebel Ali, but demand was restrained due to a 10% import duty. Regional producers kept their offers stable, with prices ranging from $560-585/t CPT. Buyers were cautious due to weak downstream demand and lack of attractive pricing. Similarly, the billet market showed limited activity, with domestic offers at $505-510/t CPT Dubai, while low-priced imports were available at $460-465/t CFR, though few deals were taking place.

Saudi HRC buyers were actively restocking, despite ongoing economic pressures and competitive Chinese pricing. Recent transactions include Chinese thin-gauge HRCs below 2mm at $595-600/t CFR and Egyptian HRCs for a domestic re-roller. Domestic prices of commercial-grade HRCs have dropped to SAR 2,310-2,320/t ($616-619/t), and CRC prices softened to SAR 2,550-2560/t ($680-683/t). HDG 1mm was being offered at SAR 3,370-3,380/t ($899-901/t). Prices exclude VAT.

EMSTEEL has introduced a green finance framework to fund low-carbon projects, including sustainable steel and cement production, renewable energy, and energy efficiency. This supports its goal to cut GHG emissions by 40% in steel and 30% in cement production by 2030.

Outlook

The UAE market is likely to stay stable in the short term, with limited changes in scrap collection volumes and steady demand from major mills. Uncertainty in the South Asian market may provide support to domestic prices, and help maintain the current market conditions.

Leave a Reply