- Abu Dhabi suppliers cut prices as buying slows down

- Need-based booking of UAE parcels by Pakistani mills supports prices

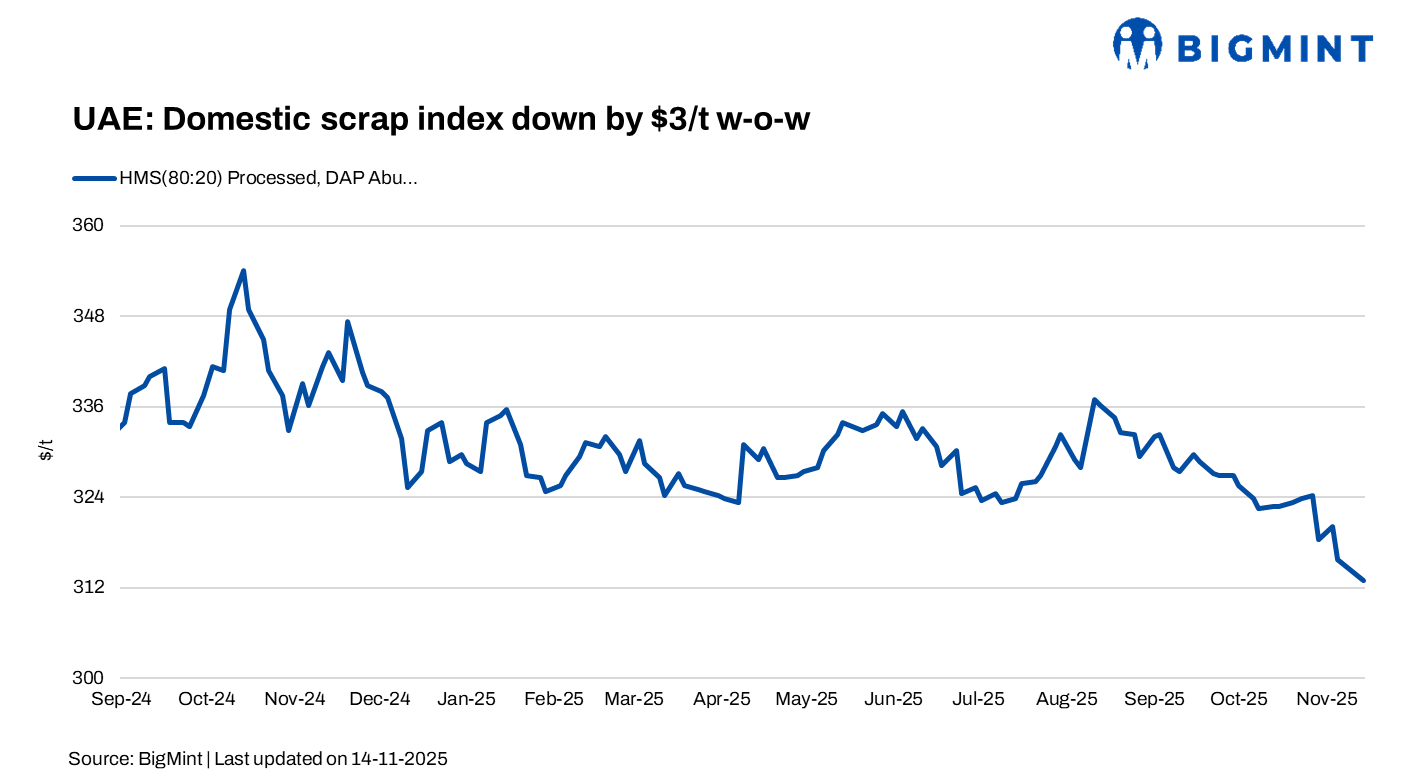

UAE’s domestic processed HMS index declined by AED 10/tonne (t) ($3/t) w-o-w to AED 1,150/t ($313/t), as per BigMint’s assessment. Local market sentiment remains subdued due to persistent oversupply, while export pricing largely held steady compared with the previous week.

A few major UAE mills have paused scrap purchases amid oversupply. Their last workable bids were AED 1,160–1,180/t ($316–321/t) for HMS and AED 1,220–1,230/t ($332–335/t) for shredded, DAP Abu Dhabi.

Suppliers in Abu Dhabi reduced their offers as demand weakened. Galvanised iron (GI) and cast iron (CI) scrap were assessed at AED 1,120/t ($305/t), unprocessed PNS at AED 1,130/t ($308/t), and processed HMS at AED 1,150/t ($313/t) DAP Abu Dhabi, reflecting ongoing market correction and softer buying interest.

Export market

Middle East-origin offers to Qasim inched up, with shredded at $364/t CFR and HMS at $340/t CFR. Broader UAE export offers were slightly firmer on higher collection costs, with shredded at $370-374/t CFR and HMS-PNS mixed cargoes at $350-355/t CFR.

Some Pakistani buyers with urgent delivery needs booked UAE parcels, providing mild support to prices. Offers remained steady as HMS was at $340/t, sheared HMS at $345-348/t, and fabrication scrap at $350-355/t on a CFR Qasim basis.

UAE rebar and flat steel market

UAE rebar demand continues to rise, supported by active construction, infrastructure, and residential projects. Local mills lifted offers to AED 2,400-2,420/t ($653-659/t) delivered, while trader deals were mostly around AED 2,370-2,380/t ($645-648/t).

Total requirements are estimated at around 560,000 t, with allocations spread across the UAE’s benchmark mill with over 170,000 t, the Omani integrated producer over 120,000 t, four UAE mills around 30,000-40,000 t each, and other GCC suppliers around 50,000 t.

Strong demand may widen the playing field for GCC suppliers as local mills struggle to expand output quickly.

UAE HRC procurement gained traction as buyers reacted to volatile Asian pricing. A 10,000-11,000 t Chinese HRC lot was booked at $494-498/t CFR, while Indian mills secured nearly 20,000 t at $500-510/t CFR after lowering offers. Japanese suppliers also remained competitive, selling 45,000 t into Saudi Arabia and the UAE at $490-495/t CFR.

Emirates Steel delivered strong domestic results, selling 2.4 mnt of finished steel in Jan-Sep 2025 (+22% y-o-y), supported by a surge in UAE construction awards. Rebar remained the core driver, rising 31% y-o-y to 1.6 mnt, while local sales increased to 90% — a shift from exports toward booming domestic demand.

Saudi Arabia

Saudi Arabia remains reliant on imported billets as domestic steelmaking capacity trails demand. With CIS volumes disrupted, China has become the Kingdom’s primary supply source, offering steady tonnages and competitive pricing. Buyers, however, note Chinese price volatility and logistical constraints. Expansion of EAF capacity may gradually reduce import reliance, though full self-sufficiency remains 10-15 years away.

Outlook

The UAE scrap market is expected to stay under pressure in the near term due to subdued domestic demand and halted mill buying, though elevated collection costs may keep prices from falling sharply.

Leave a Reply