- Scrap imports reach over 20 mnt in CY’24

- Turkiye’s domestic crude steel production rises 10% y-o-y

- Scrap prices may stay firm even as supply challenges multiply

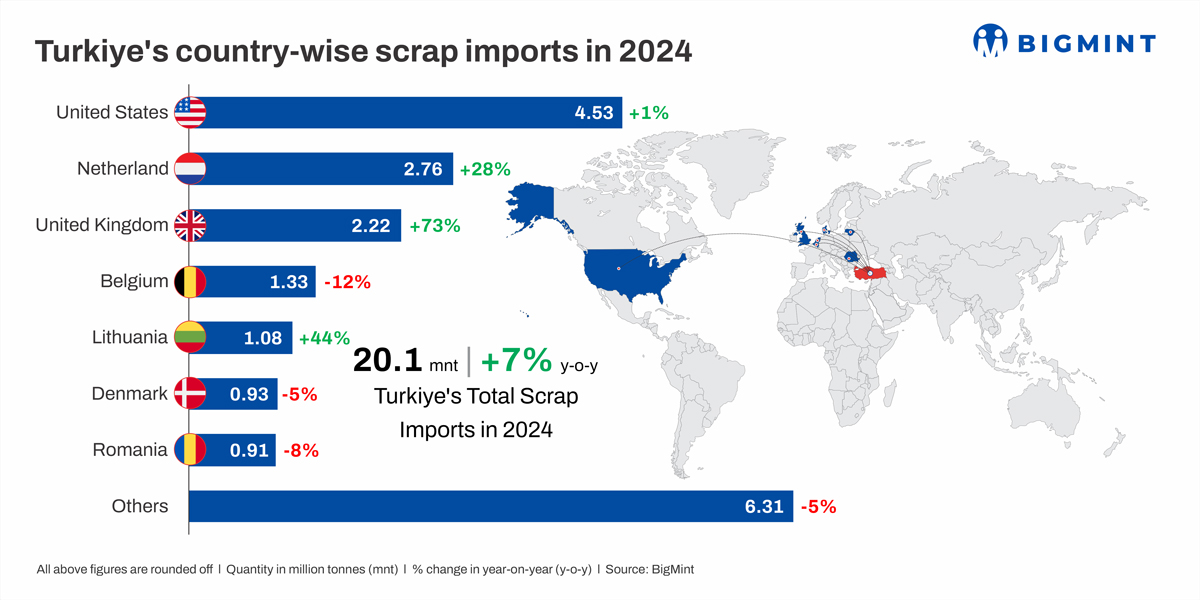

Morning Brief: Turkiye’s ferrous scrap imports rose by 7% in calendar year 2024 (CY’24) to 20.07 million tonnes (mnt) compared to 18.82 mnt in CY’23. Turkiye’s ferrous scrap usage rose 8-10% y-o-y to 27-28 mnt in CY’24, driven by higher EAF and BOF output.

In CY’24, Turkiye’s steel industry rebounded after two stagnant years, driven by infrastructure growth, facility upgrades, and post-earthquake reconstruction.

The Red Sea turmoil and skyrocketing freight rates led Indian and Bangladeshi buyers to avoid US and EU scrap, which led to cargoes getting redirected to Turkiye.

The early months of 2024 saw significant improvement in scrap imports, with January witnessing an increase of 37% y-o-y and February 33% y-o-y. A strong rebound was also observed in August and September with volumes surging by 30-35% y-o-y, indicating a late-year recovery.

Country-wise imports by Turkiye

UK: In CY’24 imports rose by 73% y-o-y to 2.22 mnt from 1.28 mnt in CY’23.

US: Imports rose by 1% y-o-y to 4.53 mnt. September saw the highest growth (+57%), while July the steepest decline (-44%).

Netherlands: Imports increased 28% y-o-y to 2.76 mnt from 2.16 mnt in CY’23.

Lithuania: Imports grew 44% y-o-y to 1.08 mnt from 0.75 mnt in CY’23).

Factors driving scrap imports

Turkish steel industry rebounds: The domestic steel industry rebounded after two years of stagnation, supported by Turkiye’s infrastructure growth, modernisation of metallurgical facilities, and post-earthquake reconstruction efforts. Crude steel production in CY’24 reached 37 mnt, marking a 10% y-o-y increase from 33.64 mnt in CY’23.

Steel consumption edged up by 2% to 38.68 mnt, driven by higher construction and end-user demand. While steel imports increased slightly to 16.73 mnt, exports also increased to 14.95 mnt from 11.9 mnt in CY’23.

In CY’24, Turkiye’s ferrous scrap usage rose 8-10% y-o-y to 27-28 mnt (from 25 mnt in CY’23), driven by higher EAF output at 26 mnt, up 8-9%, y-o-y. BOF production also increased by 10% to 11 mnt from 10 mnt in CY’23.

Redirection of seaborne cargoes: The surge in Turkiye’s scrap imports was primarily driven by increased shipments from the UK, Netherlands, and Lithuania. After the Red Sea incident erupted, Indian and Bangladeshi buyers showed limited interest in US and EU-origin scrap due to freight uncertainty and shipment delays. This led to a redirection of volumes toward Turkiye, where mills benefitted from ample supply and competitive pricing.

Drop in prices: Yearly average scrap prices declined in 2024 which supported higher scrap import volumes. In CY’24, US-origin bulk HMS (80:20) averaged $381/t CFR Turkiye, down 4% y-o-y from $396/t in 2023. Prices peaked in January ($421/t) and hit a low in December ($345/t.

However, the Turkish Lira weakened significantly in 2024, averaging TRY 33.29/$1, compared to TRY 25.2/$1 in 2023, witnessing a 32% depreciation y-o-y which affected scrap imports.

Import and Export scenario of Turkiye in CY 2024

Turkiye steel outlook 2025

Turkiye’s steel industry faces a challenging 2025, grappling with rising competition from Asian producers, uncertain domestic demand, and evolving global trade policies. The World Steel Association projects a 1-2% y-o-y decline in Turkiye’s domestic steel demand to 35.5 mnt, reflecting sluggish economic conditions and limited construction activity.

Trade barriers and shift to flat steel: US and EU trade restrictions are expected to weigh on Turkish steel exports, pushing mills to diversify from traditional rebar and wire rod into higher-value flat steel production in electric arc furnaces (EAFs). However, this transition demands a varied raw material mix, incorporating not just HMS scrap but also other metallic products like pig iron and hot briquetted iron (HBI).

Scrap prices, supply challenges: High scrap prices remain a key concern. The US’s 25% tariff on steel and aluminum imports has driven up local scrap costs, while increased Asian competition adds further strain. Market insiders suggest that scrap prices are unlikely to drop significantly in the near term, prompting some mills to scale back purchases and turn to billets as a substitute.

A recent BigMint survey reveals that over 70% of respondents expect Turkish scrap prices to rise above $375/t in the coming quarter, partly due to the anticipated impact of Trump’s tariffs, which may slowdown US scrap exports to Turkiye.

A demand rebound is expected by March with the start of the construction season, but its sustainability hinges on domestic market stability. The EU’s 2026 ban on Russian pig iron will further reshape raw material flows. While Turkish mills have been integrating HBI and pig iron to optimise production, cost and technical constraints limit widespread adoption.

TLDR scrappage law: The TLDR scrappage law refers to Turkiye’s initiative to rejuvenate its commercial fleet by incentivising the scrapping of older vessels. Implemented by the Ministry of Transport and Infrastructure in April 2021, this regulation offers financial incentives to ship owners replace ships over 20 years old with new, domestically built vessels. The programme aims to enhance maritime safety, promote environmental sustainability, and support domestic shipbuilding. However, its impact on the scrap market is expected to be limited at around 2 mnt over the course of a decade.

EU scrap export curbs: Europe’s steel industry association has raised concerns over the exclusion of ferrous scrap from the EU’s Critical Raw Materials Act (CRMA) and stricter Waste Shipment Regulation (WSR), which could limit scrap availability–critical for low-carbon steelmaking. The EU exported 19.5 mnt of ferrous scrap in 2021, and potential shortage could delay decarbonisation goals. In response, TCUD warns that EU export curbs could disrupt supply chains, impacting Turkiye’s green transition efforts.

Leave a Reply