- US tariffs, billet demand drive vessel arrivals

- Scrap prices drop to 3-year low in Apr’25

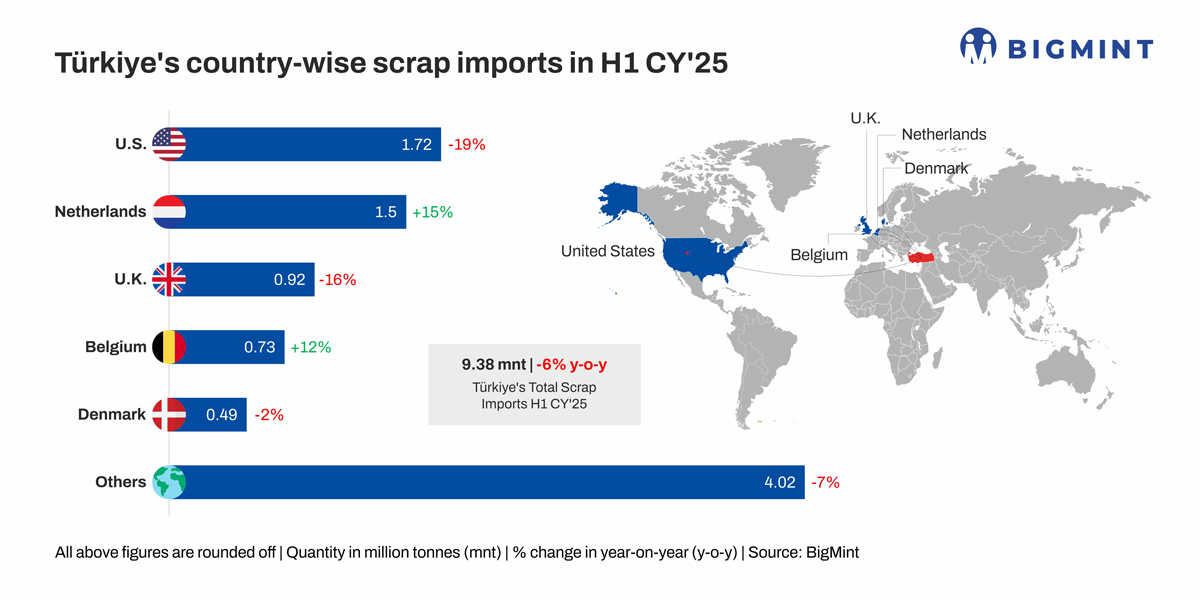

- US top supplier despite significant decline

Turkiye’s total ferrous scrap imports stood at 9.38 mnt in H1 CY’25, down 6% compared to 9.98 mnt in H1 CY’24.

On the other hand, Turkiye’s bulk ferrous scrap imports rose 4% y-o-y to 7.75 million tonnes (mnt) in H1CY’25 from 7.42 mnt in H1CY’24.

As per BigMint, the billet import volume also witnessed a sharp rise y-o-y amid increased semi-finished usage from mills to avoid higher conversion cost from scrap to rebar, although some opportunistic restocking for scrap was done by mills, supporting bulk cargo arrivals.

Turkiye’s total scrap consumption in H1CY’25 stood at 14.87 mnt, marginally higher by 0.3% compared with 14.83 mnt in H1CY’24, reflecting broadly stable demand.

Billet imports rise: Turkiye’s billet imports rose 27% y-o-y in H1CY’25 to 4.07 mnt, compared with 3.21 mnt in H1CY’24.

According to BigMint’s vessel-tracker information, a total of 350-370 bulk vessels had their estimated time of berthing (ETB) scheduled during H1CY’25.

Bulk scrap prices hit 3-year low

Turkish deep-sea imported scrap prices dropped to $325/t CFR for US-origin HMS 80:20 by the end of April 2025, the lowest level since mid-2022. This three-year low was driven by oversupply, weak finished steel sentiment, and sharp domestic rebar price declines, enabling mills to push scrap prices lower.

Restocking activity continued at reduced levels as an influx of low-grade scrap, weak demand for European cargoes, competitive Chinese billet offers, and rising yard inventories added downward pressure. Some mills cut production, further dampening scrap demand, although stronger domestic rebar sales provided limited support.

Halfyearly price average

- US-origin HMS 80:20 CFR Turkiye averaged $352/t in H1 CY’25, down 11% from $395/t in H1 CY’24.

- US-origin HMS 80:20 FOB East Coast US averaged $330/t in H1 CY’25, down 11% from $370/t in H1 CY’24.

- Rotterdam HMS 80:20 bulk FOB Europe averaged $327/t in H1 CY’25, down 10% from $365/t in H1 CY’24.

Country-wise imports

The US remained the largest supplier in H1CY’25 despite a 19% drop, accounting for 18% of Turkiye’s total scrap imports. US suppliers maintained firm offers following former US President Trump’s announcement of 25% tariffs on steel imports.

US: Imports fell 19% to 1.72 mnt in H1CY’25, compared to 2.12 mnt in H1CY’24.

Netherlands: Imports rose 15% to 1.50 mnt, up from 1.31 mnt a year earlier.

UK: Imports declined 16% to 0.92 mnt, compared to 1.10 mnt in H1CY’24.

Belgium: Imports increased 12% to 0.73 mnt, up from 0.65 mnt last year.

Denmark: Imports slipped 2% to 0.49 mnt, compared to 0.50 mnt in H1CY’24.

Key updates

Crude steel production increased 2% y-o-y to 18.89 mnt in H1 CY’25 from 18.61 mnt in H1 CY’24.

HRC imports totaled 2.23 mnt in H1CY’25, down 6% y-o-y from 2.38 mnt in H1CY’24, indicating reduced overseas procurement.

Turkiye’s rebar imports stood at 0.29 mnt in H1CY’25, rising 26% y-o-y from 0.23 mnt in H1CY’24

The Turkish lira depreciated 19%, with the average exchange rate at TRY 37.8/$ compared to TRY 31.8/$ a year earlier.

The Turkish lira depreciated 19%, with the average exchange rate at TRY 37.8/$ compared to TRY 31.8/$ a year earlier.

Outlook

Turkiye’s scrap demand in the coming months will largely hinge on domestic steel consumption, the competitiveness of billet prices against imports, and ongoing currency volatility. Any further weakness or slowdown in rebar sales could cap import volumes despite seasonal restocking requirements.

Market activity remains limited, with both buyers and sellers adopting a cautious stance. While sellers are holding out for higher prices, buyers are also waiting, though Q3 restocking needs may prompt activity.

Attention now shifts to the Central Bank of Turkiye’s Monetary Policy Committee decision on September, alongside broader geopolitical developments in the region. Both factors could shape finished steel demand and, in turn, scrap imports in the months ahead.

Leave a Reply