- Over 15 deals (equivalent to 500,000 t) concluded in the last three days

- Price outlook signals stabilisation with resistance above $400/t

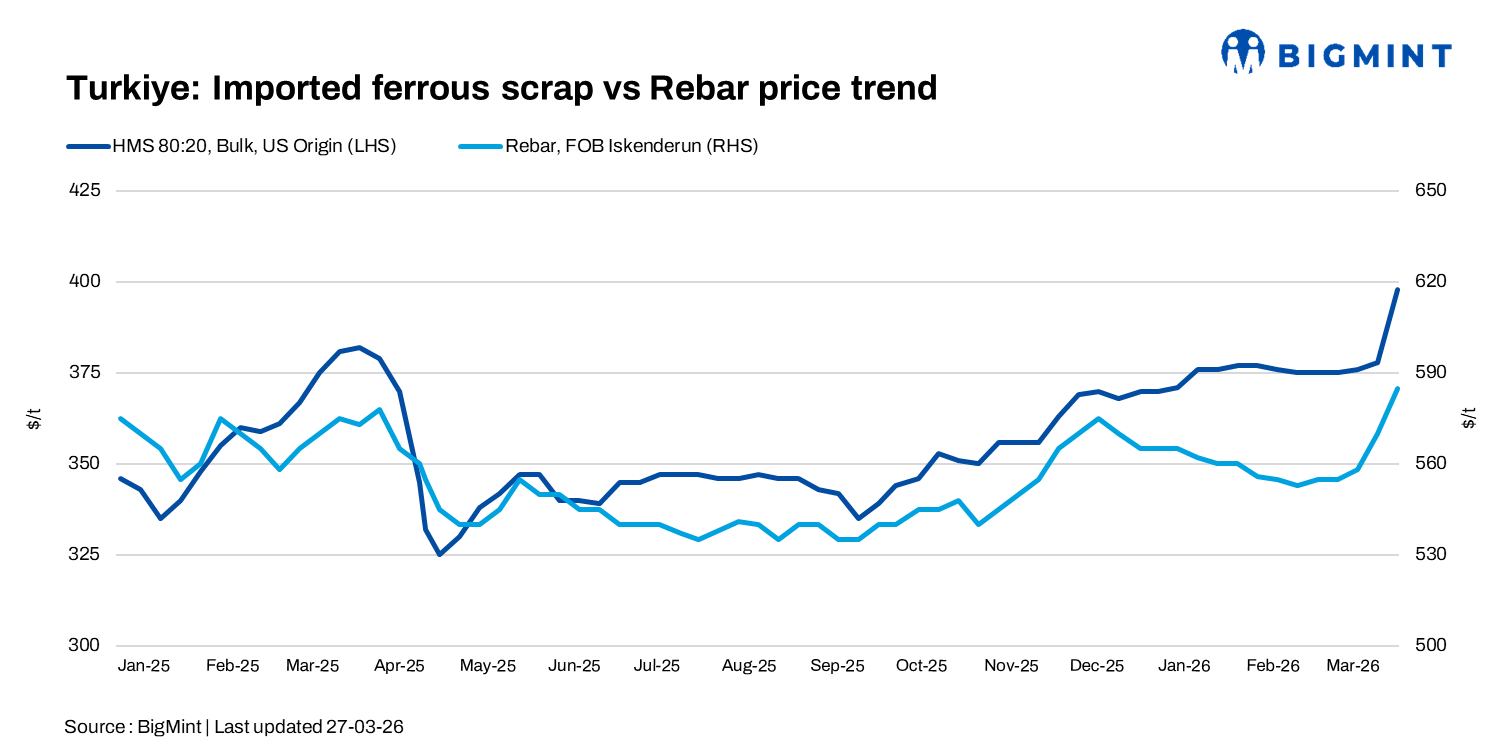

Turkish deep-sea import scrap prices continued to rise in the week beginning 23 March, supported by a flurry of recent bookings across multiple regions amid improved buying interest. Mills were actively securing cargoes for April-May shipments amid tightening availability of semi-finished steel, shifting procurement focus toward scrap.

The current assessed price for US-origin bulk HMS (80:20) stood at $397-400/t CFR Turkiye, with fresh offers heard at $404-405/t. EU/Baltic origin suppliers were quoted slightly lower at $395-397/t CFR.

It is noteworthy that mills concluded around 20 deals in just the past 3-4 days, taking the total to nearly 27 deals for the month–a sharp surge in buying activity toward month-end.

This translates to approximately 0.5 mnt (over 520,000 t) of scrap bookings within a single week, based on average cargo sizes of 25,000-30,000 t from EU/Baltic origins and over 30,000 t from the US.

Market participants feel this move was expected, but timing may not have been ideal. “Mills could have booked earlier, before Eid, when offers were around $380/t CFR. Now it has clearly turned into a seller’s market,” a Baltic trader said.

As a result, most mills are estimated to be paying $10-15/t higher on recent bookings. Another source mentioned that this rise isn’t due to any shortage of scrap, but mainly because of higher freight and bunker costs, which are currently driving prices.

An Iskenderun-based mill source noted that longer delivery timelines from China, coupled with reduced billet and slab availability from Iran and Russia, are prompting mills to accelerate scrap purchases. “With limited semi-finished inflows expected in the near term, mills are building scrap inventories,” the source said.

Meanwhile, an Europe-based scrap supplier source highlighted that uncertainty around freight and bunker costs is also influencing buying behaviour. “Freight remains unpredictable, and mills prefer to secure cargoes now rather than risk higher costs later,” the supplier said, adding that this has further supported the recent upward momentum in prices.

East Marmara-based mills

- EU-origin HMS 80:20 at $395/t

- EU-origin HMS 80:20 at $395/t

- Denmark-origin HMS 80:20 at $392/t

- UK-origin HMS 80:20 at $390/t, bonus at $413/t

- Poland-origin HMS 80:20 at $390/t

Aegean-based mills

- USA-origin HMS 80:20 at $398/t, shredded and bonus at $418/t

- USA-origin HMS 80:20 at $397/t

- USA-origin HMS 80:20 at $397/t

- USA-origin HMS 80:20 at $397/t

- USA-origin HMS 80:20 at $395/t

- Finland-origin HMS 80:20 at $390/t

West Marmara-based mills

- USA-origin HMS 80:20 at $396/t

- EU-origin HMS 80:20 at $390/t, shredded and bonus at $415/t

- Netherlands-origin HMS 80:20 at $385/t

Mediterranean-based mills

- UK-origin HMS 80:20 at $392/t

- EU-origin HMS 80:20 at $390/t

West Black Sea-based mill

- Sweden-origin HMS 80:20 at $394/t

Outlook: Finished steel export offers were heard to have improved slightly to $590-600/t FOB, lending some support to mill sentiment. However, market participants indicated that Turkish mills are likely to step back from the market in the near term after the recent round of restocking.

An Marmara-based mill source noted that “most mills have secured sufficient cargoes for now and may remain out of the market for some time.” Meanwhile, a trading source added that mills are unlikely to accept scrap prices significantly above $400/t, as margin pressures remain a concern. Overall, while sentiment remains firm, limited near-term buying and resistance to higher price levels may lead to a phase of stabilisation.

Leave a Reply