- Mills continue selective buying amid weak rebar demand

- Higher freight rates to support US-origin scrap offers

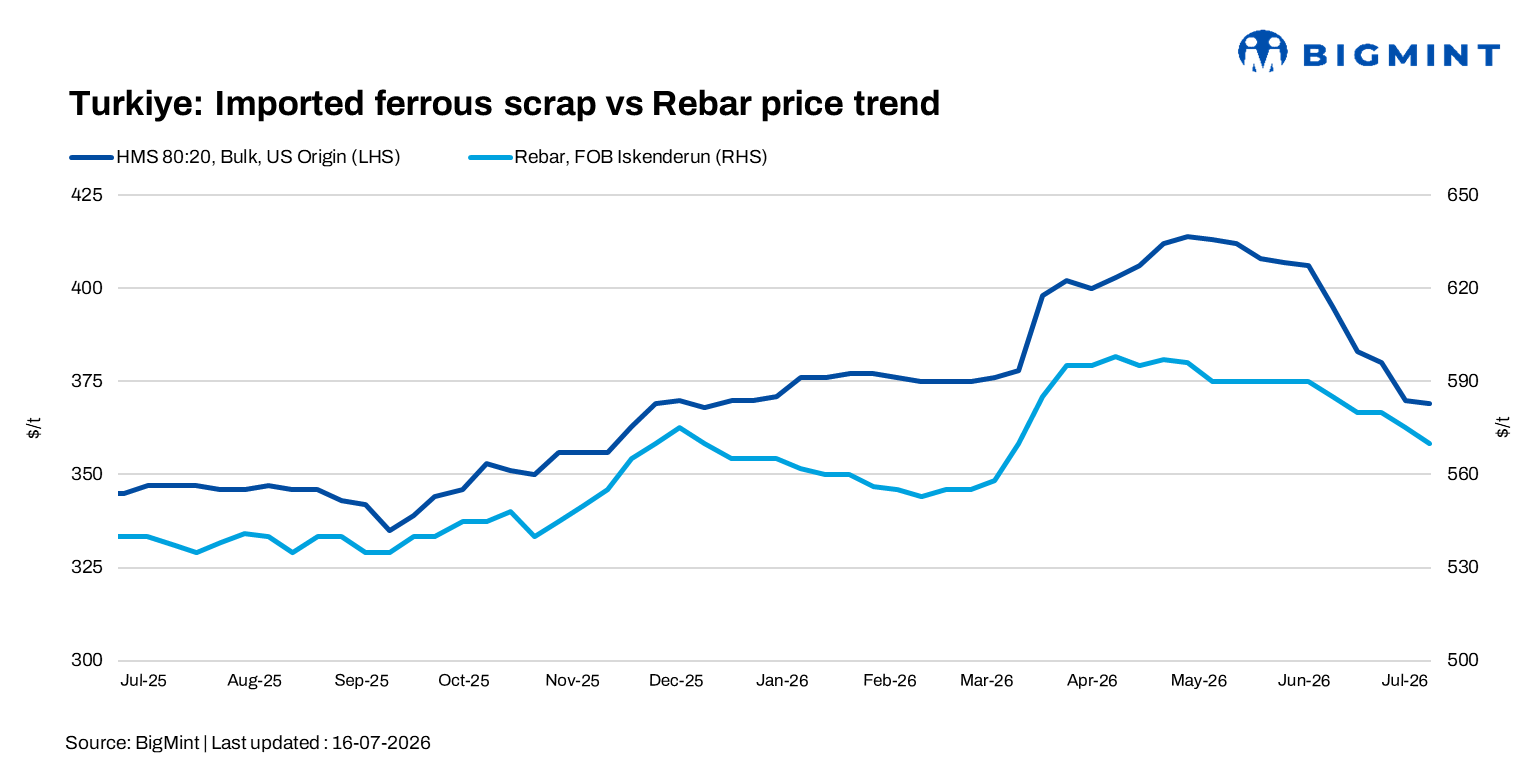

Turkiye’s imported deep-sea ferrous scrap market remained largely stable during the week ended 16 July as sluggish finished steel demand, weak rebar sales, and cautious mill procurement continued to limit trading activity. Although overall sentiment remained bearish, higher freight costs and limited availability of US-origin cargoes prevented further price declines.

Price assessments

- US-origin HMS 80:20 around $369/t CFR Turkiye, down by $1/t w-o-w.

- US East Coast HMS 80:20 around $334/t FOB, down $2/t w-o-w.

The US HMS 80:20 bulk CFR price stood at its lowest level in 2026 so far, with similar levels last seen in the final week of December 2025.

US-origin HMS 80:20 was assessed at around $369-370/t CFR Turkiye, largely unchanged w-o-w, while European/Baltic-origin material was heard at $362-368/t CFR. Market participants noted that rising freight rates from both the US and Europe continued to support export offers, squeezing suppliers’ margins and reducing their willingness to lower prices further.

Trading activity remained subdued throughout the week, with only one previously concluded Poland-origin HMS 80:20 cargo reported at $363/t CFR. Most exporters refrained from issuing firm offers, while Turkish mills continued favouring domestic and short-sea scrap due to better pricing and lower procurement risk.

Market participants indicated that tradable values for US-origin HMS 80:20 remained around $365-368/t CFR, while European-origin material was workable at lower levels. However, higher freight costs continued to prevent US suppliers from matching the discounts offered by European exporters.

A US-origin trader noted that although trading remained quiet during the public holiday period, further downside appears limited as freight costs continue to support US export prices.

Domestic steel market remains weak

Weak demand for long steel products continued to limit scrap procurement. Domestic rebar offers were heard at $565-575/t exw, while export offers remained around $568-570/t FOB. Mills continued to struggle with weak domestic and export sales, keeping deep-sea scrap purchases limited to immediate production requirements. The scrap-to-rebar spread remained around $200-202/t, supporting steelmaking margins.

Outlook

BigMint expects Turkiye’s imported scrap market to remain largely rangebound in the coming week. Mills are likely to maintain need-based procurement as finished steel demand remains weak, while elevated freight costs and limited US-origin cargo availability should prevent any significant decline in imported scrap prices. Further market direction will largely depend on the pace of recovery in domestic and export rebar demand.

Leave a Reply