- Scrap prices steady as rebar demand weakens

- Mills cautious amid stable scrap import levels

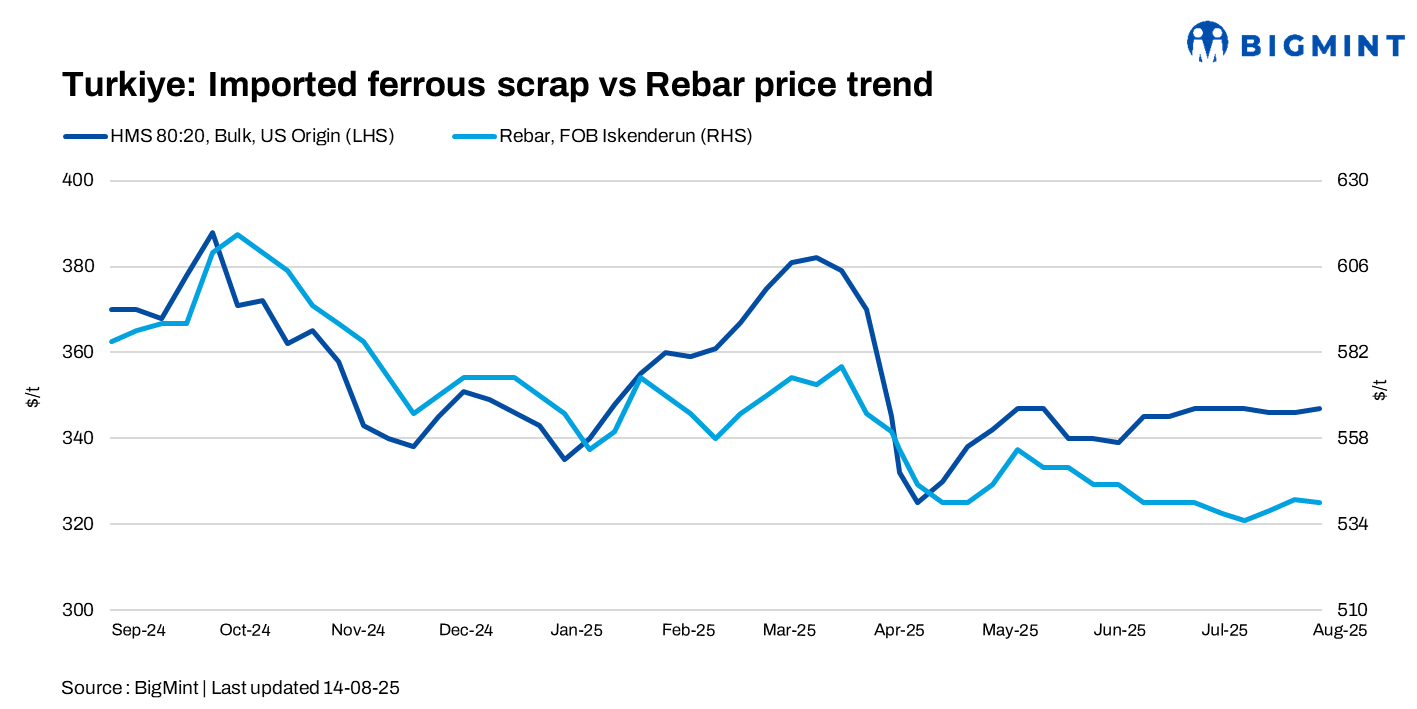

Turkiye’s deep-sea ferrous scrap import prices held largely stable w-o-w at $347/t CFR, moving sideways amid weakening rebar fundamentals. With finished product prices stagnant, mills see little reason to pay more for scrap.

In the last 3-4 days, limited deep-sea deals were concluded.

Price assessments

- US-origin HMS 80:20 bulk scrap stood at $338/t CFR Turkiye, stable w-o-w.

- Bulk HMS 80:20 from the US East Coast was at $318/t FOB, stable w-o-w.

The Turkish rebar-to-scrap spread stood at $190-195/t, with workable levels for Turkish rebars heard at around $535-540/t FOB.

Recent deals

- A Aegean-based mill booked US-origin HMS 80:20 at $345.5/t CFR.

- Another Aegean-based mill booked US-origin HMS 80:20 at $341.5/t CFR.

- Another Aegean-based mill booked US-origin HMS 80:20 at $346/t CFR.

Market updates

A market participant said, “While mills are expected to increase overseas scrap purchases, weak finished steel sales in both export and domestic markets is kepping buying restrained. US and Baltic-origin HMS 80:20 offers were reported at $345-350/t CFR, while importers’ bids were about $5/t lower”.

A mill official said, “The mills have paused scrap purchases for now, with market participants anticipating a short-term price downturn and describing the market as very quiet with a bearish sentiment.

Despite the current lull, scrap bookings saw an uptick in July as Turkish steelmakers sought alternatives to higher-priced billet and slab from Asian sources.

Domestic market

Turkish producers remained focused on the longs steel segment, where rebar prices stayed unchanged and demand was sluggish. Rebar demand is weak, so most mills prefer to wait before resuming scrap bookings, especially as sellers are unwilling to lower prices.

Outlook

Market participants are awaiting clearer price direction, with some watching the Central Bank’s MPC meeting in September for cues. However, others anticipate a modest price increase in the near term, with prices rising by $3-5/t for September and October loading sales. Additionally, mills are expected to book more for September shipments due to limited availability of low-priced billet and slab from Asian suppliers.

Leave a Reply