- Local, short-sea scrap more competitive than deep-sea cargoes

- Weak rebar demand pushes mills to delay Jun-shipment bookings

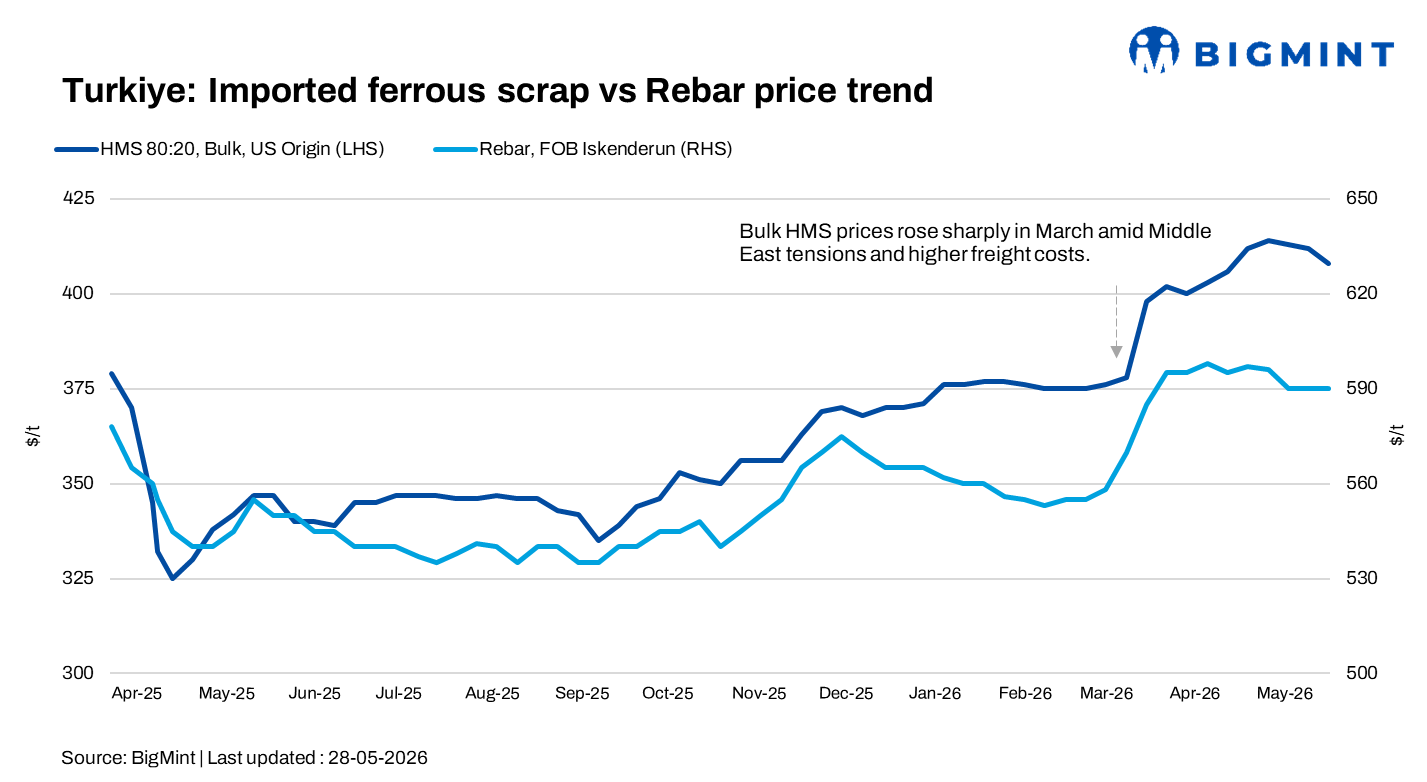

Turkiye’s deep-sea imported scrap prices softened slightly in the week ended 28 May, with HMS 80:20 prices heard around $408-410/t CFR amid limited trading activity ahead of the extended Eid al-Adha holidays.

Market participants noted that many mills delayed bookings despite requiring cargoes for June shipments, as weak rebar demand and tight liquidity conditions kept buyers cautious.

Price assessments

- US-origin bulk HMS 80:20: $408/t CFR Turkiye, down $4/t w-o-w

- US East Coast HMS 80:20: $376/t FOB, down $2/t w-o-w

Throughout May, the market largely remained firm as European suppliers continued maintaining higher offer levels, supported by elevated scrap collection costs, stronger freight rates earlier in the month, and a firmer euro. However, Turkish mills continued struggling with sluggish finished steel sales, high financing costs, and squeezed operating margins, which restricted aggressive scrap procurement activity.

Towards the end of May, however, market sentiment gradually started shifting in favour of buyers. The weakening euro, correction in freight rates, and softer Chinese billet prices increased pressure on scrap suppliers. Several Turkish mills also turned more actively towards local scrap procurement and short-sea cargoes, where material remained comparatively cheaper than deep-sea imports.

Three deep-sea scrap deals were reported during the period, including a US-origin cargo sold to an East Marmara mill at $411/t CFR for HMS 80:20, while UK- and Netherlands-origin cargoes were reportedly concluded around $403-404/t CFR roughly more than a week ago.

Meanwhile, the scrap-to-rebar spread remained narrow at around $178-182/t, continuing to pressure Turkish mill margins, while export rebar prices stayed largely stable near $590/t FOB.

Market comments

A Turkish-based trader said, “Most Turkish mills have entered wait-and-watch mode ahead of the holidays. Buying activity remained extremely limited, although some mills were testing lower bid levels around $400-405/t CFR for US-origin HMS.”

Another trader noted that workable buying indications for US-origin cargoes had softened closer to $403-405/t CFR, while some mills were targeting levels below $400/t CFR.

US suppliers largely maintained firm offers near $415/t CFR, supported by higher collection prices, firm domestic scrap markets, and elevated freight costs. Tradable values for HMS 80:20 were mainly reported around $405-410/t CFR, while workable levels for EU-origin cargoes were heard around $400-405/t CFR.

A Baltic supplier stated, “Sellers are still trying to hold offers firm, but many market participants believe current price ideas above $410-412/t CFR may be difficult to sustain under weak steel market conditions.”

Market participants noted that many mills had already shifted into pre-holiday mode, slowing negotiations and fresh booking activity. One trader said the Turkish market would remain largely inactive until 1 June due to the extended holiday period.

A Turkish mill source added that “The scrap market may gradually soften after the holidays, and US-origin HMS 80:20 below $400/t CFR could soon become achievable.”

Outlook

BigMint expects the Turkish imported scrap market to remain relatively quiet in the coming days as Eid holidays continue limiting trading activity and mill participation. Most buyers are expected to stay cautious in the immediate term, while suppliers are also likely to avoid aggressive negotiations during the holiday period.

After the holidays, however, market pressure may gradually increase as Turkish mills continue facing weak rebar demand, tight margins, and growing competition from cheaper Chinese billet offers. Market participants indicated that deep-sea HMS 80:20 prices, currently hovering around $408-410/t CFR, could soften slightly over the next couple of weeks if finished steel sales fail to improve.

At the same time, several mills are still expected to return for June shipment cargo bookings due to ongoing raw material requirements. Suppliers, meanwhile, continue maintaining relatively firm offers despite improving cargo availability across Europe, mainly supported by elevated collection costs and earlier freight pressures. Overall sentiment remains cautious, with buyers increasingly trying to secure lower workable levels before returning actively to the market.

Leave a Reply