- Weak rebar demand limits buying activity

- Prices expected to move sideways in early 2026

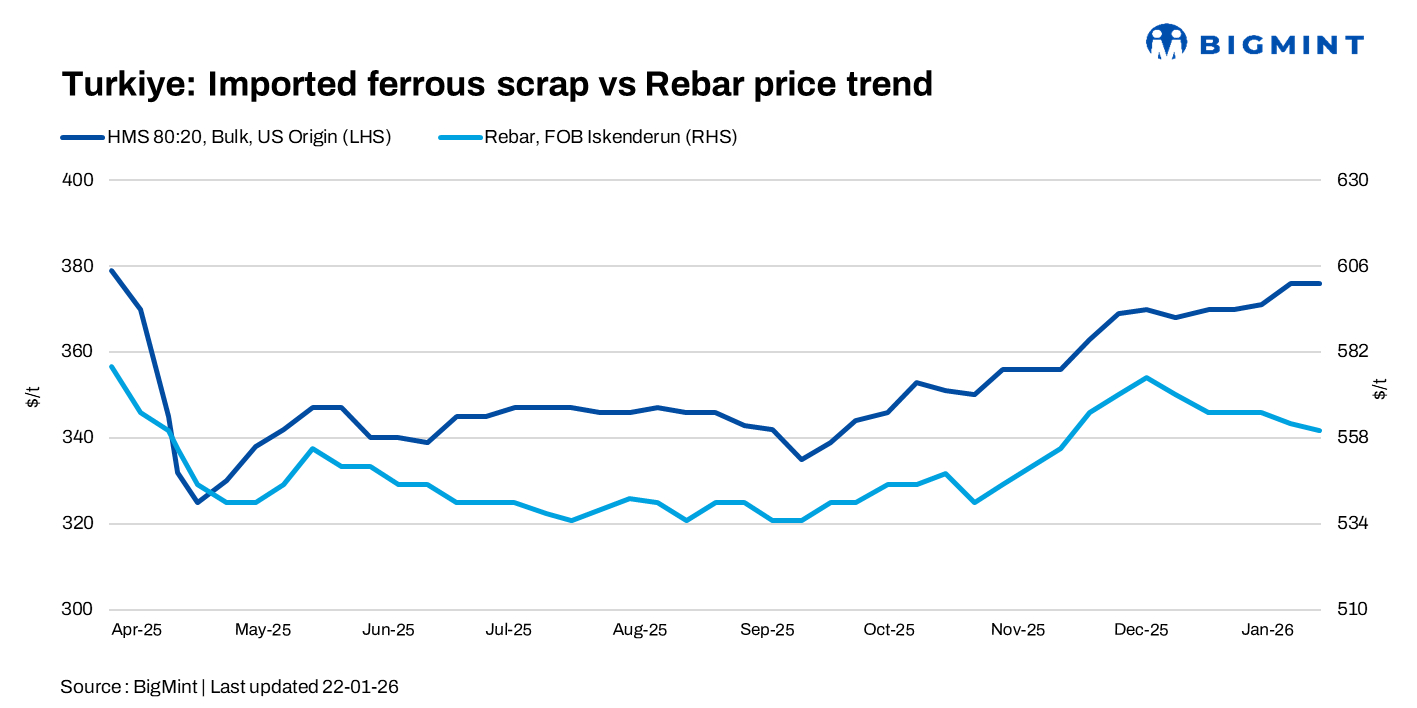

Turkish imported scrap prices stayed largely unchanged w-o-w at $376/t CFR in the week ending 22 January, amid weak rebar demand and cautious buying. Limited deals, tight margins, and scarce winter supply supported prices, while subdued domestic and export rebar markets capped upside. Market participants expect sideways movement in early 2026 amid balanced, lower-than-expected demand conditions.

Price assessments

- US-origin bulk HMS 80:20: $376/t CFR Turkiye, unchanged w-o-w.

- US East Coast HMS 80:20: $350/t FOB, unchanged w-o-w.

Scrap-to-rebar spread: At $184-185/t, with rebar export offers at $560/t FOB

Market commentary

As per market insiders, a few large Turkish mills have begun booking scrap cargoes from the US West Coast, although deliveries– particularly for February– have reportedly faced delays, prompting a more cautious near-term buying approach.

US West Coast scrap typically commands a $30-40/t premium over East Coast material. However, sources indicated that some West Coast vessels have already been booked for delivery into the Izmir region later in 2025, a gradual shift in sourcing behaviour, partly driven by weaker buying interest from South Asia and rising collection costs from Europe.

Despite softer demand, some participants expected scrap prices to remain relatively firm due to limited winter supply, high collection costs, and scarce offers from US and EU sellers. To cover immediate requirements, mills continue to rely heavily on prompt European cargoes.

Around 4-5 deals were reported, including two from the EU and two from the US, in between $372-381/t CFR.

A Marmara-based mill reportedly booked a US-origin HMS 90:10 cargo at $381 CFR, normalised to $376/t CFR for HMS 80:20, with participants saying the level can be considered from new deals as well.

US-origin scrap prices into Turkiye are rising lately because American EAF mills are running unusually hard, even through the year-end holiday period. US EAF utilisation stayed above 80% in late December and rebounded quickly to over 82-84% by mid-January, sharply lifting domestic scrap demand.

As a result, US obsolete scrap prices jumped $20-25/t in December, followed by a further $25-30/t increase in January.

The RMDAS ferrous scrap index reflected this strength, with HMS gaining $28/t to $381/t (+8%). Shredded scrap is up $30/t m-o-m to $424/t (+8%), and prompt industrial scrap is rising $17/t to $434/t (+4%).

This sharp domestic price rise has reduced exportable surplus from the US, forcing exporters to lift offers for the Turkiye-bound HMS 80:20.

Domestic rebar market

The domestic rebar market remained subdued, with harsh winter weather across Turkiye weighing on construction activity and steel consumption. Muted demand continued to limit mills’ appetite for scrap purchases. The rebar export market was also quiet amid weak buying interest. Turkish exported rebar at $560/t FOB Turkiye, unchanged.

Outlook

Market participants expect Turkish scrap prices to move largely sideways in early February, as tight margins, limited winter supply, and cautious rebar demand balance each other. While local demand may provide some support, weak exports, seasonal slowdown, and uncertainty over EU carbon rules are likely to keep prices stable in the near term.

Leave a Reply