- August scrap bookings remain below expectations

- Most mills delay fresh bookings amid poor rebar sales

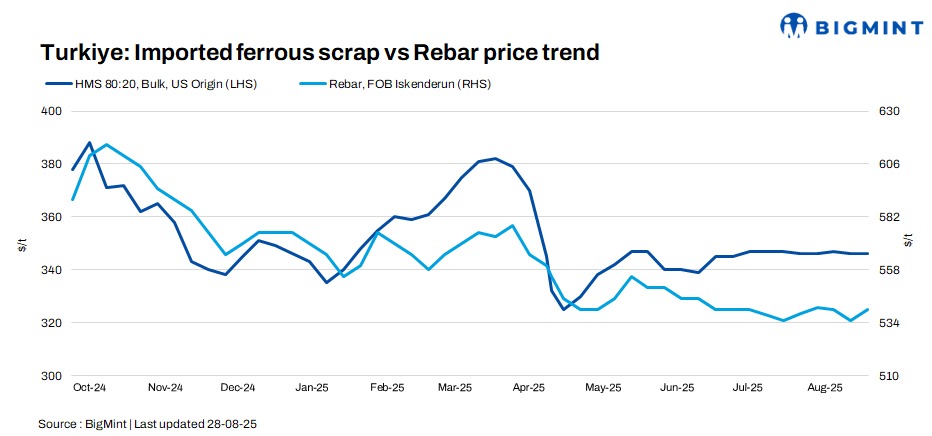

Turkiye’s deep-sea ferrous scrap import prices remained stable w-o-w, as market activity stayed subdued and sentiment was weak under persistently quiet trading conditions. Both buyers and sellers showed little interest in negotiations, with weak demand continuing to weigh on prices.

August scrap bookings totaled just 13-14 cargoes, well around 20-22 initially expected. Mills limited purchases amid slow summer steel sales, leading to a supply overhang.

Price assessments

- US-origin HMS 80:20 bulk scrap was assessed at $346/t CFR Turkiye, stable w-o-w.

- Bulk HMS 80:20 from the US East Coast stood at $316/t FOB, a decrease of $1/t w-o-w.

The Turkish rebar-to-scrap spread remained at $194-195/t, with workable rebar export prices reported at $540/t FOB.

Market updates

Tradable values for HMS 80:20 were reported in the $340-349/t CFR range, with most deals at $345-347/t CFR. While EU-origin cargoes were offered at $343-345/t CFR.

As per Baltic scrap suppliers, current Baltic/European offers are around $340-360/t for HMS and shredded. Some are even at $340/t, with a few at $338/t, depending on the origin.

Participants noted that the market remains very slow, with stronger pressure to reduce prices as focus shifts toward October shipments. Sellers also faced challenges in securing vessels for end-August, with some postponing shipments into September.”

A mill executive said, “There is ample availability of cargoes, mainly from Europe, but mills have shown little interest in September bookings that would normally have been covered by now, and new deals are likely at lower prices, although US recyclers are expected to hold firm.

Domestic market

In the domestic steel demand remained weak. Kardemir managed to sell about 21,000 t of rebar locally, but most producers held back from new scrap bookings while focusing on sluggish rebar sales.

Outlook

Market sentiment suggests further downside risk, with participants expecting lower scrap deal levels ahead if steel demand fails to recover in September.

Leave a Reply