- Mills put off bookings on weak steel demand, price cut hopes

- Cheaper EU cargoes pressure spreads with the US, Baltic

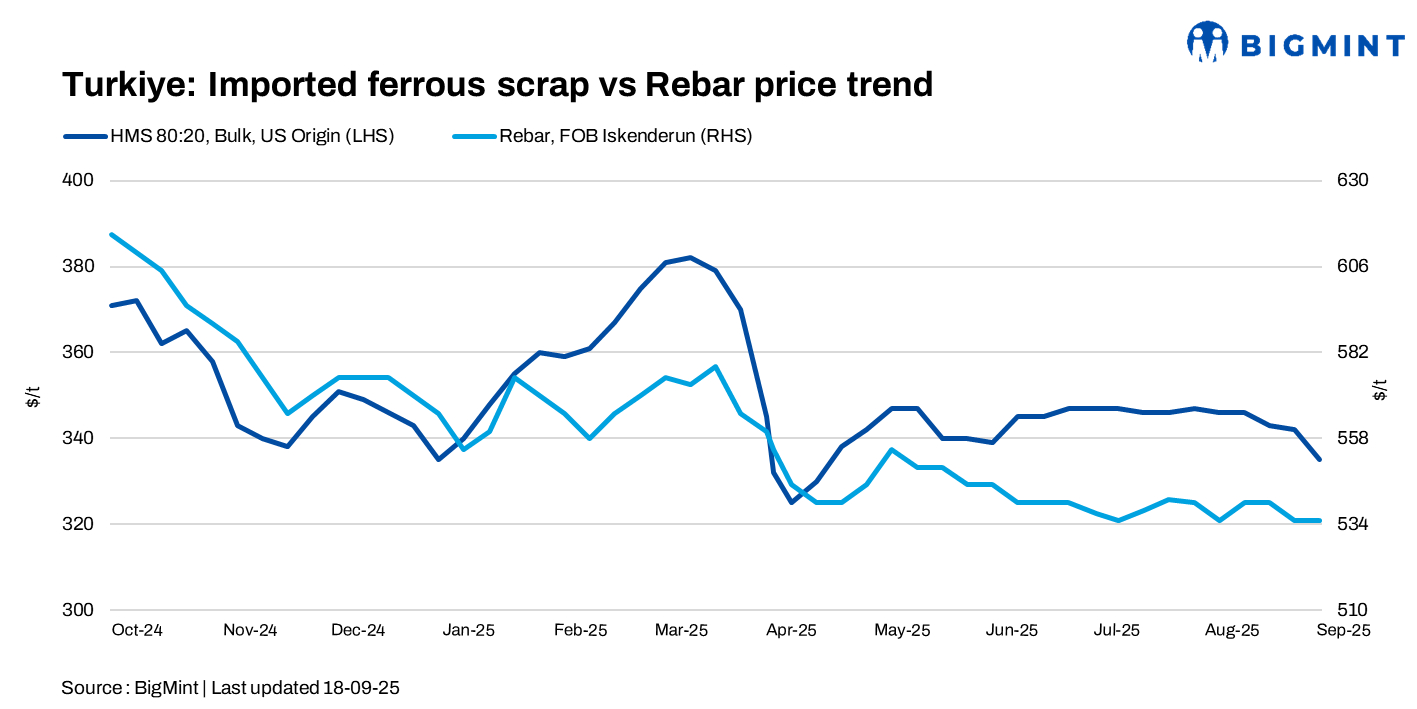

Turkiye’s deep-sea imported ferrous scrap market extended its decline last week, with prices falling by $7/t w-o-w. The drop was driven largely by competitively priced European-origin cargoes, which narrowed the usual spread against US and Baltic supplies and kept pressure on overall market sentiment.

Around 3-4 major cargoes were reported, all for October shipments, but trading stayed limited as mills delayed fresh bookings amid weak finished steel demand.

Price assessments

- US-origin bulk HMS 80:20 was assessed at $335/t CFR Turkiye, down by $7/t w-o-w.

- Bulk HMS 80:20 from the US East Coast stood at $303/t FOB, a decrease of $7/t w-o-w.

The Turkish rebar-to-scrap spread remained at $192-194/t, with workable rebar offers at $530-540/t exw, slightly lower than last week’s $540-550/t.

Market updates

Tradable values for US/Baltic-origin HMS 80:20 were reported at $334-336/t CFR, whereas EU-origin HMS 80:20 was heard at $328-330/t CFR.

As per a Turkiye-based trader, steelmakers continued lowering their bids, pushing prices down as sellers operated near breakeven, with EU-origin cargoes seen as more flexible in adapting to Turkish pricing.

A market participant noted that current low price levels remain less sustainable for sellers. The exchange rate isn’t helping much, making it difficult for Europeans to sell at current levels.

Domestic market

In the domestic market, long product prices held steady despite weaker scrap. Rebar offers from most mills stayed in the range of $520-550/t exw, unchanged w-o-w. Integrated mill Kardemir was the only producer to conclude some domestic sales. Mills continued attempts to raise finished steel prices, though sluggish demand kept interest muted both domestically and overseas.

Outlook

Market participants anticipate limited downside from current levels, as suppliers are expected to resist further price reductions. It seems unlikely that prices will dip further, with supply showing resistance. However, rising freight rates remain a key concern and could impact near-term deal activity.

Leave a Reply