- Mills engage in selective buying on unsupportive steel demand

- Domestic scrap prices edge down as import values decline

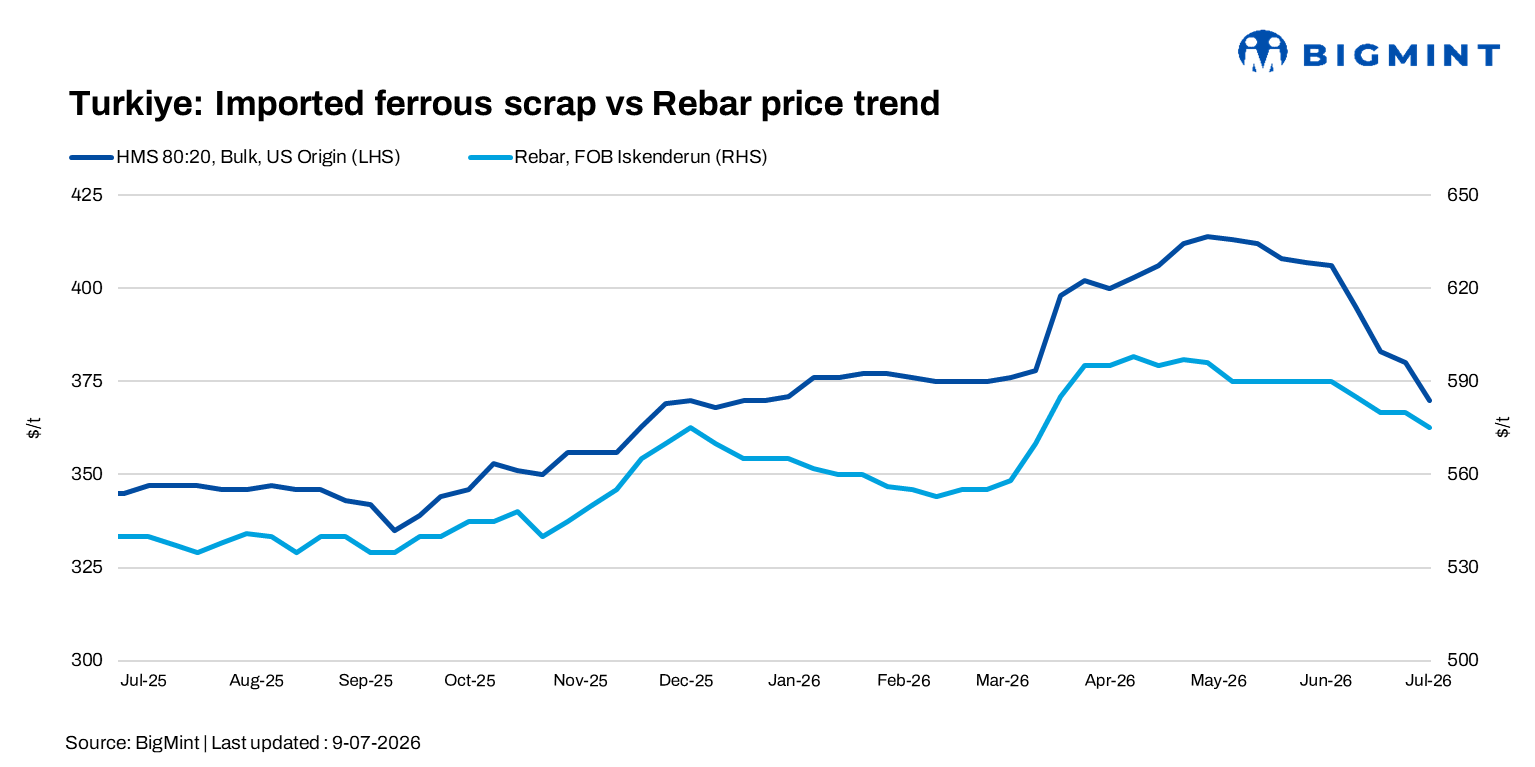

Turkiye’s imported deep-sea ferrous scrap market weakened further during the week ended 9 July as sluggish finished steel demand, softer rebar prices and cautious mill procurement continued to weigh on sentiment.

Imported scrap prices have now slipped below pre-Iran-Israel conflict levels to their lowest since the first week of January 2026. Weak steel margins, coupled with subdued domestic and export demand, have kept Turkish mills on a need-based procurement strategy, limiting purchases to immediate production requirements.

European-origin HMS 80:20 was heard at $362-365/t CFR, while US-origin HMS 80:20 was indicated at $370-372/t CFR, both down $10/t w-o-w. Despite softer market conditions, US suppliers remained reluctant to reduce offers further because of elevated freight costs, while buyers continued targeting lower workable levels.

Lower imported scrap prices expanded the scrap-to-rebar spread to $200-205/t, as rebar export offers stood at $570-575/t FOB.

Price assessments

- US-origin HMS 80:20 around $370/t CFR Turkiye, down by $10/t w-o-w.

- US East Coast HMS 80:20 around $336/t FOB, down $9/t w-o-w.

Trading activity remained limited during the week as Turkish mills continued to procure scrap on a hand-to-mouth basis amid weak finished steel demand. Market participants reported 4-5 deep-sea transactions, including a US-origin HMS 80:20 cargo sold to a West Marmara-region-based mill at $373/t CFR, UK and Europe-origin HMS 80:20 cargoes booked by Mediterranean at $363/t and $365/t CFR, respectively, and a Russia-origin HMS 80:20 cargo sold to an Aegean region-based mill at $363/t CFR.

Market updates

Market participants noted that US-origin HMS 80:20 offers remained around $375-378/t CFR, while tradable values clustered at $370-372/t CFR. Higher freight costs continued to support US offers, preventing sellers from matching the steeper declines seen in Baltic and European cargoes.

A Baltic trader said, “Finished steel demand remains extremely weak, making further scrap price corrections inevitable. Mills are buying only when necessary.”

Domestic steel market remains weak

Weak demand for long steel products continued to limit scrap procurement. Kardemir reopened domestic rebar sales after cutting prices by TRY 170-175/t ($4/t) to TRY 31,800-32,000/t ($678-683/t) exw. The producer sold around 42,000 t, supported mainly by competitive pricing and favourable payment terms rather than stronger market demand.

Other Turkish mills also reduced domestic rebar offers by $5/t w-o-w to $565-585/t exw, while August export offers eased to $570-575/t FOB. Market participants said further price reductions would largely depend on additional declines in imported scrap values.

Domestic scrap purchase prices were also cut by TRY 100-500/t ($2-11/t) during the week as mills aligned local procurement with softer imported scrap prices. Falling import values widened the scrap-to-rebar spread to $200-205/t, improving steelmaking margins. However, mills continued favouring domestic scrap over imported cargoes to protect profitability.

Outlook

BigMint expects Turkiye’s imported scrap market to remain under pressure in the coming week as weak domestic and export demand continues to restrict mill buying. Procurement is likely to remain need-based, with tradable levels expected to hover around $370/t CFR unless finished steel demand improves. Domestic scrap prices may see further corrections if imported scrap weakens more, although elevated freight costs are expected to limit downside for US-origin cargoes.

Leave a Reply