- Rising freight costs, mixed market signals keep mills cautious

- Steel imports into Turkiye may slow, boosting domestic output

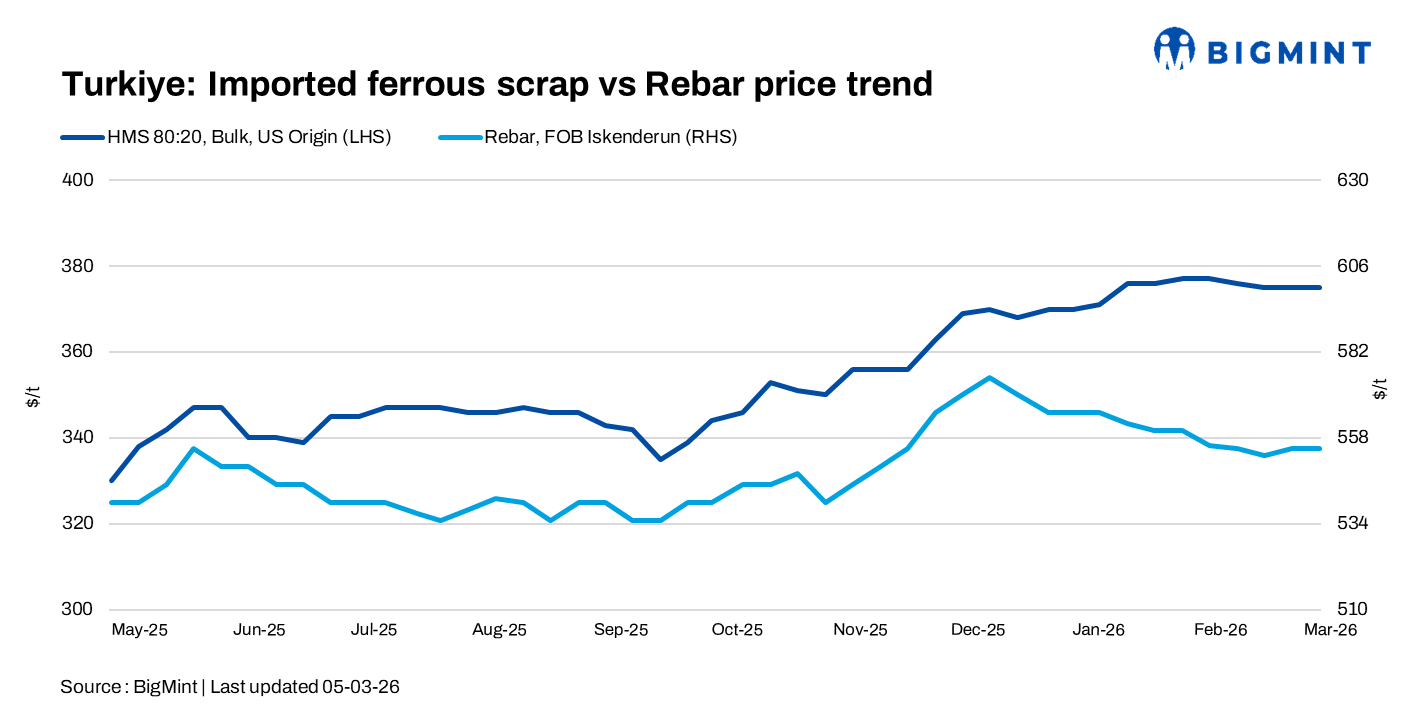

Turkish deep-sea imported scrap prices remained largely stable w-o-w on 5 March, as market participants adopted a cautious stance amid the ongoing Middle East conflict. HMS 80:20 was assessed at around $375/t CFR, with uncertainty over the duration of the war influencing market direction.

Sellers continued to resist lower bids from mills, supported by rising freight costs. A Baltic-origin scrap supplier said, “Freight is rising sharply — about $15/t from the US and around $10/t from the Baltics. Exporters will not absorb these costs, so buyers will have to bear the increase.”

He added, “Workable levels in Turkiye are around $370-375/t for HMS 80:20. Mills are trying to push prices lower, but the real challenge right now is knowing which market information can actually be trusted.”

Baltic-origin cargoes were heard around $373/t CFR, while EU-origin material circulated between $366-370/t CFR.

Price assessments

- US-origin bulk HMS 80:20: $375/t CFR Turkiye, stable w-o-w.

- US East Coast HMS 80:20: $344/t FOB, down by $2/t w-o-w.

The scrap-to-rebar spread remained at $179-180/t, with rebar export offers at $555/t FOB.

Around four deals were reported in the $365-374/t CFR range, mostly for Europe-origin material, with only one cargo from the US West Coast, concluded just before the Middle East conflict escalated.

A US-origin scrap supplier representative said, “The market was mostly quiet until the deals heard yesterday, with many participants just watching from the sidelines. One US West Coast cargo was booked last Friday, though the details of some recently circulated trades remain unclear.”

He added, “Some recently circulated deals should be viewed cautiously, as the sudden release of multiple trades from the same source raises questions.”

Market participants also stated that information circulating in the market should be treated cautiously, as both buyers and sellers are attempting to influence sentiment through selective deal reporting.

Domestic steel market

Downstream steel demand remained sluggish, with Turkish rebar export offers largely unchanged at $555-560/t FOB in recent weeks. This has made mills cautious regarding scrap procurement due to production adjustments and uncertain export demand.

However, some traders indicated that disruptions in regional trade flows, particularly around Iran, could reduce finished steel imports into Turkiye. This may encourage higher domestic production levels, potentially supporting scrap demand in the near term.

Outlook

For now, the Turkish scrap market remains in a wait-and-watch phase as participants monitor geopolitical developments and rising freight costs. While mills are attempting to push prices lower, exporters remain firm amid higher logistics costs. Market participants also note that distinguishing reliable trade signals from speculation remains a key challenge.

Leave a Reply