- Sellers keep offers firm on expectations of further restocking

- Mills turn to scrap cargoes as imported billet costs climb up

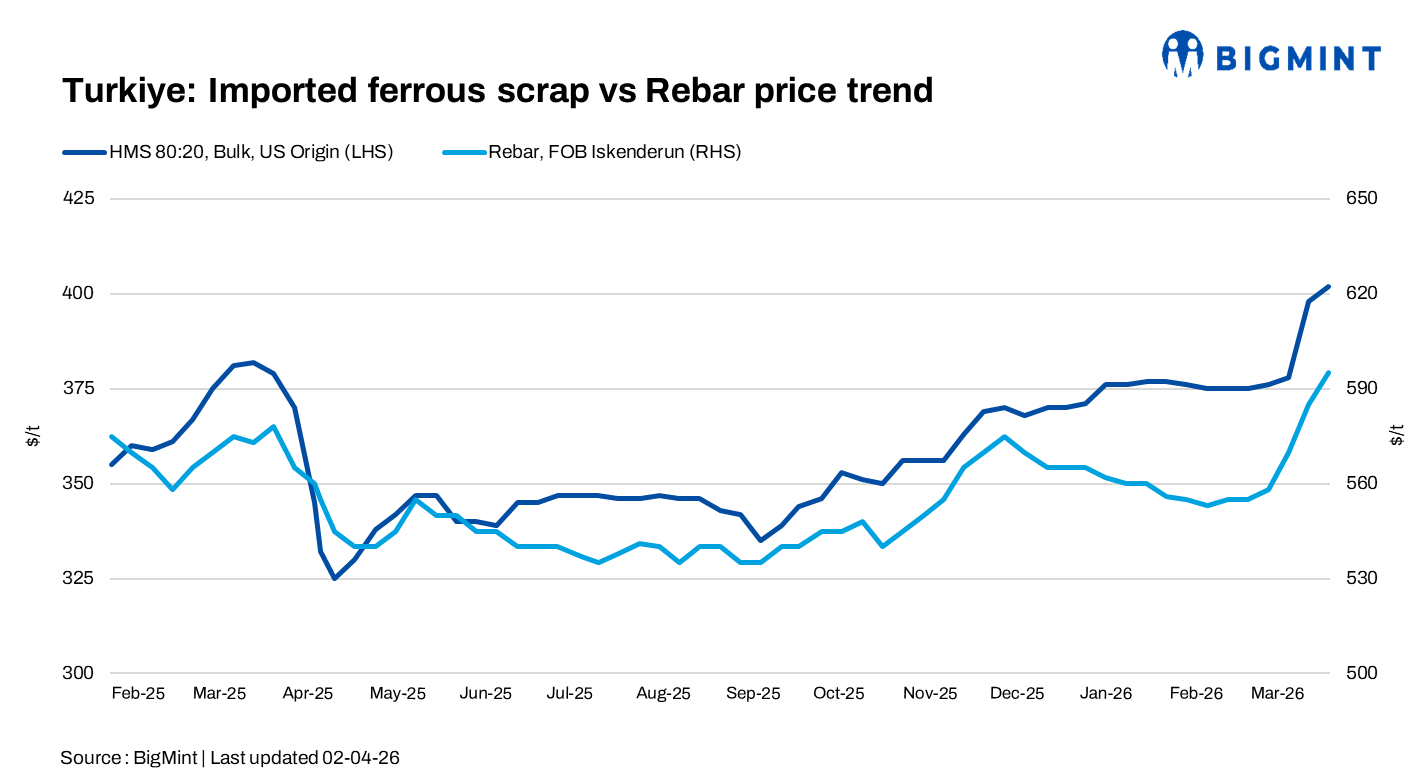

Turkish deep-sea scrap prices edged up by $4/tonne (t), with HMS 80:20 assessed at around $402-405/t CFR on 2 April, supported by firm freight and energy costs. Sellers kept offers firm as mills remain in the midst of a restocking phase. However, US-origin HMS 80:20 tradable levels were heard slightly lower at $398-400/t CFR, indicating limited buying interest at higher offers.

No major fresh deals were reported during the past week (27 March-2 April) following a strong buying phase earlier, when more than 20 deals were concluded in just 3-4 days. However, some unconfirmed higher-grade cargo trades were heard, with US/Canada-origin HMS 90:10 at $410/t CFR (equivalent to $402-405/t for HMS 80:20). Market talk also indicated the same-origin deal to a Mediterranean-based mill at around $417/t for HMS 95:5 and $422/t for shredded/PNS CFR, though these also remain unconfirmed.

Price assessments

- US-origin bulk HMS 80:20: $402/t CFR Turkiye, up $4/t w-o-w

- US East Coast HMS 80:20: $370/t FOB, up $4/t w-o-w

The scrap-to-rebar spread widened to around $193-195/t, with rebar export offers at $595-596/t FOB, continuing to keep mill margins under pressure.

Market updates

Turkish mills stepped back from the deep-sea scrap market after an active buying phase last week, though further bookings are expected as inventories require replenishment. Around 26 cargoes were confirmed for March.

A market participant said, “Scrap prices are edging up as mills return for April-May requirements, while sellers are holding firm above $400/t CFR.”

Another source noted, “US suppliers are not in a hurry to sell and expect further upside as mills continue restocking.”

Rising freight and energy costs continued to support offers, while firm billet prices also strengthened scrap demand sentiment.

Offers from Germany were heard near $395/t CFR. Limited US activity due to Easter holidays kept offers scarce. Freight is estimated at $50/t from the US and $55-60/t from the Baltic.

Semi-finished steel market: The ongoing Middle East conflict is gradually changing how Turkish mills manage their raw material mix. In 2025, Turkiye imported around 8 million tonnes (mnt) of semis from multiple sources, giving mills good flexibility.

However, that flexibility is now tightening. Supplies from nearby regions, such as Oman, the UAE, and Iran, have become less reliable due to disruptions and higher risks. At the same time, imports from Asia have gotten more expensive because of rising freight and insurance costs. As a result, semis have become harder to depend on, both in terms of price and delivery. This has pushed mills to rely more on ferrous scrap, which is currently seen as a more stable and dependable option.

Imported billet, CFR Turkiye, prices rose $10-12/t w-o-w to $495-500/t CFR as compared to $485/t last week.

Domestic steel market

Turkey’s domestic steel market was under pressure as imported scrap prices moved up and rising energy and production costs squeezed mill margins. Rebar demand remained weak, so mills struggled to pass on higher raw material costs. Even though mills tried to push up finished steel prices, slow construction activity and cautious buyers kept the market subdued.

As per market insiders, local scrap was trading about $15-20/t lower at $378-380/t, mainly because its of lower quality (70:30/60:40) compared to imported 80:20.

Outlook

BigMint expects Turkish imported scrap prices to remain firm next week, supported by restocking demand and strong seller expectations. However, margin pressure and high input costs may limit aggressive buying, with market direction dependent on billet prices and freight trends.

Leave a Reply