- Scrap prices fall amid weak demand, high inventories

- Steel mills restock selectively, market sentiment cautious

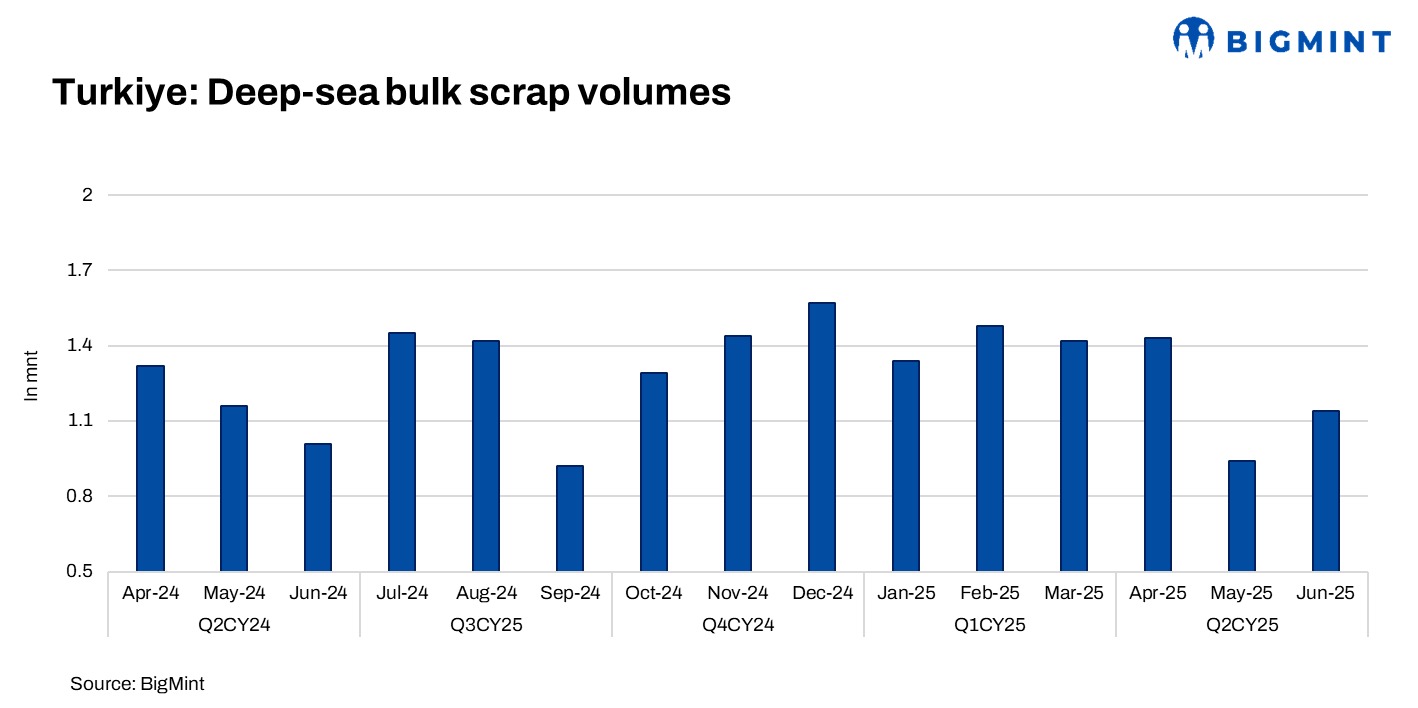

Turkiye’s bulk scrap imports in Q2 CY’25 stood at 3.51 million tonnes (mnt), dropped by 23% q-o-q from 4.53 mnt in Q1 CY’25.

On the other hand, if we consider the corresponding period of last year (Q2 CY24), the volume inched up by 1% as compared to 3.49 mnt.

According to BigMint’s vessel-tracker data, 88-90 deep-sea bulk vessels were scheduled to berth (ETB) in Q2 CY’25. Including short-sea vessel movements, total vessel activity reached approximately 140 during the quarter.

Quarterly comparison for price and key updates (steel production, billet imports, HRC imports, Lira)

Quarterly price average

- US-origin HMS 80:20 CFR Turkiye averaged $345/t in Q2CY’25, down 3% from $357/t in Q1CY’25.

- US-origin HMS 80:20 FOB East Coast US averaged $324/t in Q2CY’25, down 4% from $336/t a year earlier.

- Rotterdam HMS 80:20 bulk FOB Europe averaged $322/t in Q2CY’25, down 3% from $331/t in Q1CY’25.

Sellers struggled to match the downward price trend due to inventories purchased at higher costs, a sharp fall in export prices, and the pressure of a strong euro. Mills continued restocking but at reduced levels amid oversupply and weak finished steel sentiment. Demand stayed limited, weighed down by sluggish rebar sales and competition from low-priced Chinese billets.

Sellers struggled to match the downward price trend due to inventories purchased at higher costs, a sharp fall in export prices, and the pressure of a strong euro. Mills continued restocking but at reduced levels amid oversupply and weak finished steel sentiment. Demand stayed limited, weighed down by sluggish rebar sales and competition from low-priced Chinese billets.

Key updates

Turkiye’s crude steel production : Crude steel production stood at 9.04 mt in Q2CY’25, dropped by 1% from 9.1 mt in Q1CY’25.

The Turkish lira depreciated 21%, with the average value falling to TRY 39.16 in Q2CY’25 compared to TRY 36.6 in Q1CY’25.

Billet imports rise: Turkiye’s billet imports in Q2 2025 totalled 2.27 mnt, up from 1.81 mnt in Q1 2025, marking an increase of 25% q-o-q.

HRC imports edge up: Turkiye’s HRC imports in Q2 2025 totalled 1.19 mnt, up from 1.04 mnt in Q1 2025, marking an increase of 14% q-o-q.

Rebar imports rise by 31%: Turkiye’s rebar imports rose to 0.17 mnt in Q2CY’25 from 0.13 mnt in Q1CY’25.

Outlook

Outlook

Turkiye’s scrap demand is likely to remain range-bound near term, with mills adopting selective buying amid weak finished steel sales and cautious market sentiment. BigMint vessel-tracker data shows bulk arrivals recovering, with 1.3 mnt in July versus 1.1 mnt in June. Any price rebound will hinge on seasonal restocking, stronger export orders, or a narrower scrap-to-billet price gap.

Leave a Reply