- Imported scrap prices weaken amid ample offers

- Mills remain cautious as finished steel demand stays subdued

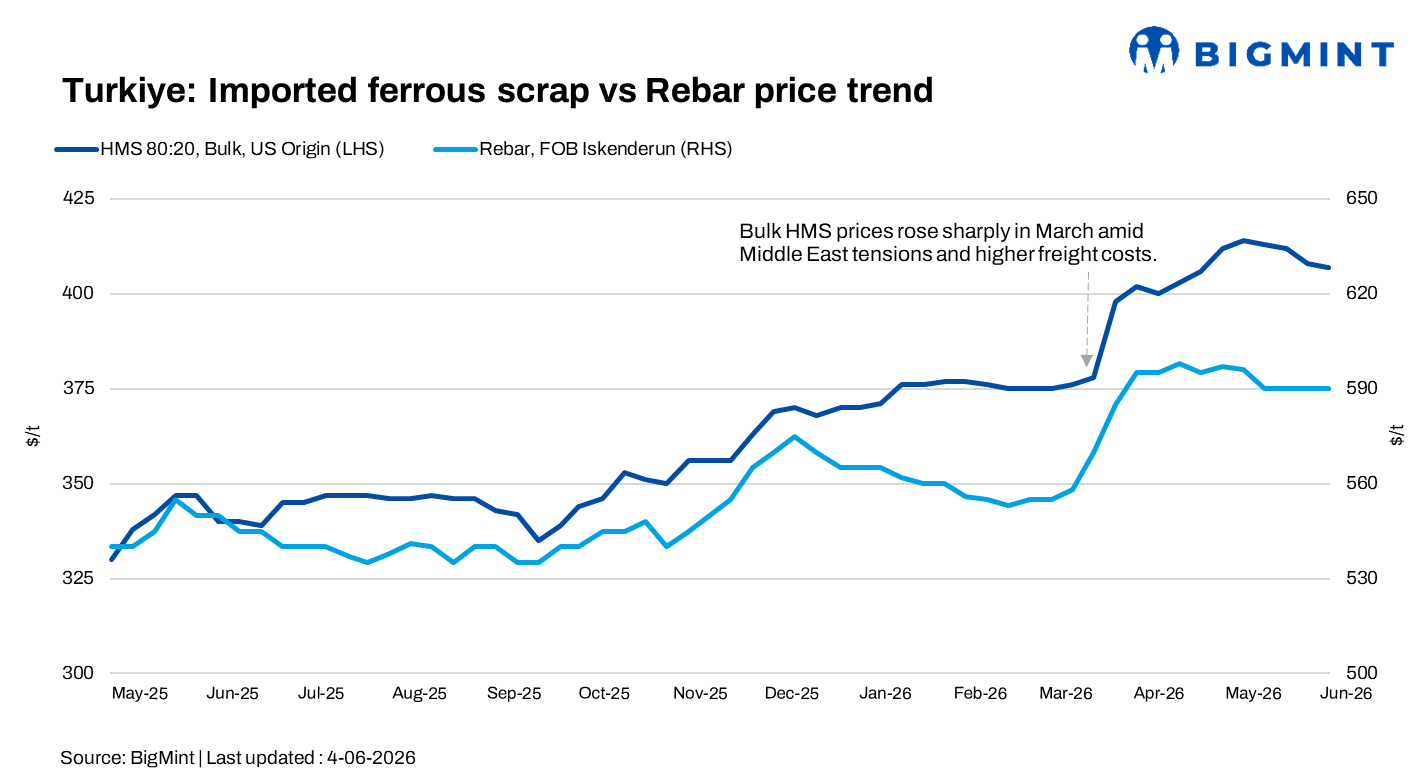

Turkish deep-sea imported scrap prices declined w-o-w, with HMS 80:20 assessed at around $405-406/t CFR. Market sentiment remained bearish during the week amid abundant scrap supply, weak rebar demand, and cautious mill buying.

Buyer participation remained limited, while the number of available suppliers continued to increase, placing additional downward pressure on prices. While a few transactions surfaced, most producers continued to delay bookings, expecting further corrections in the market.

Price assessments

- US-origin bulk HMS 80:20: $406/t CFR Turkiye, down $2/t w-o-w

- US East Coast HMS 80:20: $373/t FOB, down $3/t w-o-w

Only one deep-sea scrap deal was reported during the week, with an EU-origin HMS 80:20 cargo sold to an East Marmara mill at $397/t CFR. Market participants linked the transaction to a rumoured booking that was later denied by the alleged buyer, leaving its details unconfirmed. Meanwhile, details emerged of a previously concluded US-origin deal, with HMS (90:10) booked at $414/t CFR and shredded scrap at $429/t CFR for June shipment.

Meanwhile, the scrap-to-rebar spread remained tight at around $180-183/t, continuing to pressure Turkish mills’ margins, while export rebar offers were heard stable at approximately $590/t FOB.

Market updates

“Turkish mills are currently prioritising rebar sales over scrap purchases. Finished steel demand remains weak, limiting buyers’ willingness to accept higher prices. At the same time, abundant cargo availability is forcing sellers to become more flexible in negotiations,” a Turkish trader source commented.

According to market sources, workable levels for US-origin HMS 80:20 were heard around $400-405/t CFR, while EU-origin material was indicated below $400/t CFR. Several participants noted that prices have fallen significantly from levels seen two weeks ago, when suppliers were targeting at least $405/t CFR for EU-origin cargoes and around $410-412/t CFR for US-origin material.

Market participants pegged the tradable value of high-grade HMS 80:20 at $404-411/t CFR, clustering around $407/t CFR. However, sentiment remained largely negative, with many sources expecting prices to soften further due to weak steel demand and the abundance of sellers in the market. Some buyers were heard targeting $395-400/t CFR for EU-origin material.

Domestic steel market: Turkish mills remained focused on improving finished steel sales amid weak domestic and export demand. Rebar demand continued to underperform expectations, limiting producers’ appetite for aggressive scrap purchases and keeping pressure on steelmaking margins.

Market participants said mills continue to procure scrap on a need-to-buy basis amid weak margins. The scrap-to-rebar spread remained tight at around $183/t– a persistent pressure from high raw material costs.

Outlook

The Turkish scrap market is expected to remain under pressure in the near term as mills continue to limit purchases to immediate requirements amid weak steel demand and poor margins. Ample scrap availability and cautious buying sentiment may keep prices under pressure, with some market participants expecting further corrections before buying activity improves.

At the same time, Iran’s temporary ban on semi-finished steel exports through end-June could offer some support to the market. Reduced Iranian supply may create additional export opportunities for Turkish steelmakers, potentially leading to improved scrap demand in the coming weeks.

Leave a Reply