- Richards Bay stocks fall to 3.5 mnt; FOB 6,000 kcal at $102-103/t

- Indonesian policy risks and freight reshape global coal trade flows

The seaborne coal market is entering a more balanced phase after the recent rally, with price movements now driven more by inventories, freight and industrial demand than by broad consumption growth. Data from the week starting 23 February 2026 show tightening stock levels in key export hubs, firm prices across basins, and trade flows shaped increasingly by arbitrage and fuel economics rather than simple demand expansion.

South Africa: exports firm as Indian industry supports the market

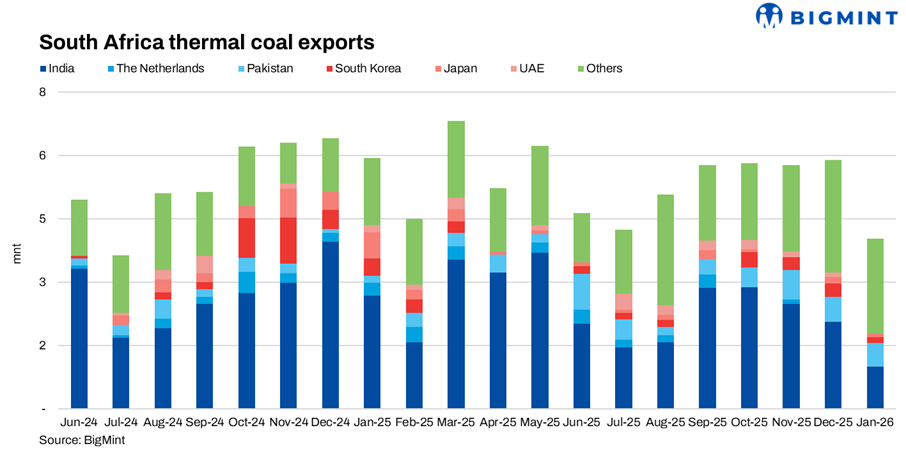

South African export momentum remains visible in terminal inventories. Stocks at Richards Bay Coal Terminal stood at roughly 3.5 mnt as of 23 February 2026, down both month-on-month and year-on-year, reflecting strong export pull rather than supply disruption. Indian buyers, particularly sponge iron producers and industrial users, continue to be the main marginal demand source.

Spot prices mirror this steady demand. During the same period, FOB Richards Bay 6,000 kcal coal traded near $102-103/t, with 5,700 kcal material around $101/t and 5,500 kcal close to $90-91/t. These levels suggest the market has stabilised after the rally, though buyers in India are increasingly cautious and are waiting for either freight easing or a modest price correction before covering further cargoes.

Because industrial users are less price-sensitive than utilities, South African coal continues to find buyers even as prices rise. This makes Richards Bay exports an important support for the Atlantic basin.

Europe: winter rally fading as prices consolidate

In Europe, the delivered coal market appears to be pausing after several weeks of gains. During the week ending 20 February, physical cargoes into the Amsterdam-Rotterdam-Antwerp (ARA) hub were trading around $112-113/t, with forward contracts in a similar range. This suggests the winter risk premium is largely priced in.

Inventory signals remain supportive but not bullish enough to drive another rally. ARA stocks remain structurally below historical averages, even though they have recovered slightly week-on-week. Meanwhile, milder weather expectations, stable gas prices and weaker forward power spreads are limiting additional coal demand. Without a new supply shock or cold spell, European prices are likely to hold rather than rise sharply.

Asia: arbitrage and policy risk continue to guide global flows

The broader direction of seaborne coal still depends heavily on Asia. As of 23 February 2026, Chinese port inventories had fallen noticeably below long-term February averages, suggesting

tighter domestic availability and supporting the import outlook once post-holiday trading activity resumes.

At the same time, Indonesian policy uncertainty continues to influence market sentiment. Potential export limits or quota delays create a risk premium that benefits alternative suppliers such as South Africa and Australia, even when actual export volumes remain stable.

Freight costs are also reshaping competitiveness between origins. Higher Atlantic freight, particularly from the US, is making long-haul supply less attractive and reinforcing the role of regional exporters such as South Africa into India and Australia into Asia. Freight therefore acts as a ranking mechanism, constantly reshuffling which origin is most competitive for buyers.

The bigger picture: tight supply supports prices despite limited demand growth

Taken together, the late-February data suggest the seaborne coal market is not being driven by strong new demand growth, but rather by supply discipline, logistics and regional fuel economics. Tight inventories in both Asia and the Atlantic basin are preventing prices from falling sharply, even as the winter demand impulse fades.

In the near term, high-calorific coal prices may soften slightly as buyers wait for clearer signals and better entry points. However, over the medium term, low stock levels, freight volatility and ongoing policy risks should keep the global coal market broadly supported rather than weak.

Leave a Reply