- Liquidity crunch slows down trade activity

- Rebar prices decrease by INR 300/t w-o-w

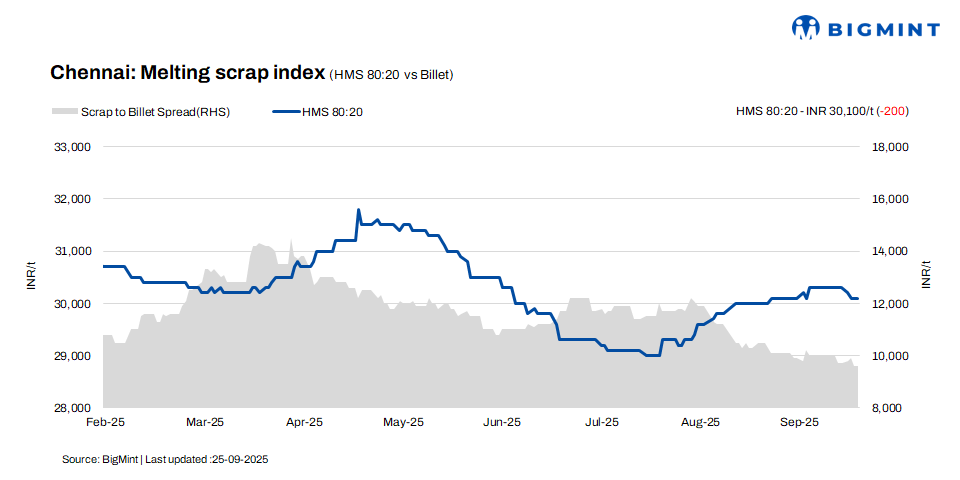

Chennai’s HMS (80:20) prices declined by INR 200/t w-o-w to INR 30,100/t, according to BigMint’s latest assessment. Meanwhile, they remained flat on a d-o-d basis. Billet registered a similar weekly drop of INR 600/t to INR 39,700/t, though remained stable on a day-to-day basis. Rebar prices mirrored this downtrend, easing by INR 300/t both d-o-d and w-o-w to INR 44,200/t.

Market sentiment remained subdued, with limited trade volumes and price corrections seen across key raw materials and finished long products, suggesting cautious trade activity.

Imported, domestic price trends

According to a scrap trader, imported shredded offers were at $365-370/t, while bids remained lower at $350-355/t. Similarly, HMS 80:20 was offered at $345-350/t, with bids coming at $330-335/t, reflecting a consistent bid-offer gap of $15-20/t. With no major deals heard, market activity remained muted, as demand for imported scrap was weak. Many buyers continued to prefer domestic scrap due to its competitive pricing and comparable quality.

In Chennai, domestic HMS (80:20) was transacted at INR 30,000-30,500/t for spot deals with immediate payment, whereas deals on extended credit terms fetched slightly higher rates of INR 30,500-31,000/t. Market activity was concentrated within the INR 30,000-31,000/t range, indicating liquidity-driven pricing, with payment terms continuing to influence trade values and buyer-seller dynamics.

Buyer-supplier sentiments

According to sources, finished steel demand in Chennai has remained weak over the past couple of weeks, with liquidity constraints continuing to weigh on overall trade sentiment. In the merchant market, billet availability has increased, as mills show readiness to sell to standalone units amid subdued rebar demand. Meanwhile, sponge iron prices have remained stable on a w-o-w basis, with offers at around INR 26,700/t.

A leading scrap supplier stated that HMS 80:20 was traded in the range of INR 30,000-31,000/t, with rates influenced by payment terms. Ongoing liquidity challenges led to subdued trade activity in recent weeks. Weak demand for billets and rebar further pressured mills to reduce scrap procurement prices to manage conversion costs, driving the current market sentiment and pricing trends.

Regional comparison

In the Jalna market of western India, HMS 80:20 prices declined by INR 300/t d-o-d to INR 30,500/t, while rebar dropped by INR 200/t to INR 43,100/t. Billet prices also edged down by INR 100/t to INR 38,700/t. According to market sources, finished steel demand has remained weak over the past couple of weeks, with mills carrying inventory levels equivalent to 12-15 days of production. It is also heard that some mills are considering production cuts next month in response to soft demand and elevated stock levels.

Outlook

While the market is currently facing a slowdown, scrap prices are expected to remain range-bound in the near term, with possible fluctuations limited to around INR +/-500/t. Market dynamics, particularly demand recovery and liquidity trends, will be key in determining short-term price direction and maintaining overall stability.

Leave a Reply