- Sponge iron trading volumes decline w-o-w

- Margins under pressure across long steel value chain

Sponge iron & melting scrap

South India’s sponge iron market remained largely stable during the week ended 10 July, with Bellary sponge iron prices holding at INR 25,000/t ex-works despite maintenance shutdowns and partial capacity utilisation at several large-scale kilns. Stable pricing was supported by balanced supply-demand fundamentals, although trading activity slowed considerably as steelmakers restricted purchases amid weak downstream demand.

On the supply side, several large sponge iron producers in the Bellary region continued scheduled maintenance, with some kilns operating at nearly 50% of installed capacity. However, sufficient inventories and balanced material availability ensured that reduced production did not translate into supply shortages, keeping the market adequately supplied.

Raw material costs softened during the week. Iron ore pellet (Fe63%) prices declined by INR 100/t to INR 9,700/t ex-works Bellary, while RB2 coal prices fell by INR 200-250/t to around INR 10,400/t ex-Gangavaram Port. The decline in input costs eased production expenses for sponge iron manufacturers, although producers largely maintained offer prices amid stable market fundamentals.

Demand conditions weakened during the week, reflected in a sharp decline in market transactions. BigMint tracked only 9,600 t of sponge iron deals during the current week, compared with 17,800 t in the previous week, as buyers limited procurement to immediate production requirements amid sluggish finished steel demand. Market participants also reported weaker business activity across the supply chain, with fewer enquiries and delayed purchasing decisions contributing to lower trading volumes.

Melting scrap (80:20) prices remained unchanged at INR 31,000/t FOR Chennai due to downstream steel markets continued to exhibit weakness which reflecting limited movement across the semi-finished and finished steel segments.

Semi-finished steel

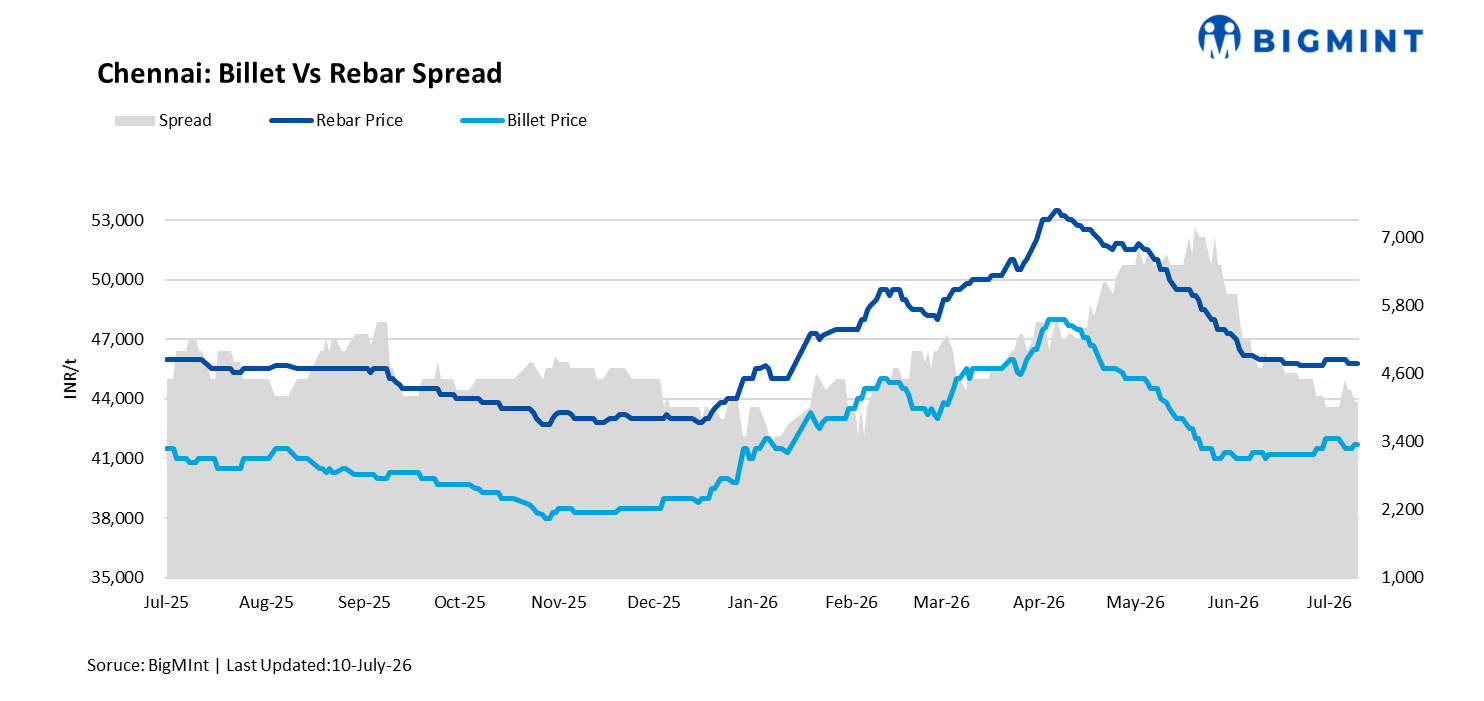

Billet prices remained broadly stable in Hyderabad, while Chennai billet prices declined by INR 300/t week-on-week due to weaker demand from re-rollers.

The conversion spread between HMS 80:20 scrap and MS billet stood at around INR 10,700/t in Chennai, reflecting restrained profitability for scrap-based steelmakers.

Billet trading activity remained subdued during the week as rebar manufacturers limited fresh procurement. Narrow billet-to-rebar conversion margins, coupled with elevated processing costs, prompted buyers to adopt a cautious purchasing approach and procure material only on a need-based basis.

Rebar

The finished steel market remained under pressure across southern India. Induction-route rebar prices in Hyderabad were largely stable at around INR 43,000/t for Fe-500 grade (12-25 mm), while blast furnace-route rebar prices corrected by INR 700/t w-o-w to INR 50,300/t ex-yard Hyderabad. The price gap between induction-route and blast furnace-route rebar widened to approximately INR 7,000/t.

Inventory pressure also intensified in the rebar segment, with mills holding around 15-25 days of inventories, depending on production scale. To accelerate inventory liquidation and maintain plant utilisation, several rebar manufacturers in the Chennai region have started offering discounts of INR 2,000-2,500/t below prevailing market prices. Combined with subdued construction activity, these discounts reflected continued pressure on finished steel demand and market sentiment.

Outlook

Steel prices are expected to remain under pressure in the near term amid subdued trading activity and rising inventories at mill level. Weak demand, coupled with the ongoing monsoon across several western and southern states, is likely to weigh on steel consumption, prompting mills to offer discounts to stimulate sales. As a result, steel manufacturers may face further margin compression if demand fails to improve in the coming weeks.

Leave a Reply