- Scrap prices rise as LNG shortages slow scrap-cutting activities

- Plant maintenance tightens billet supply, keeping prices firm

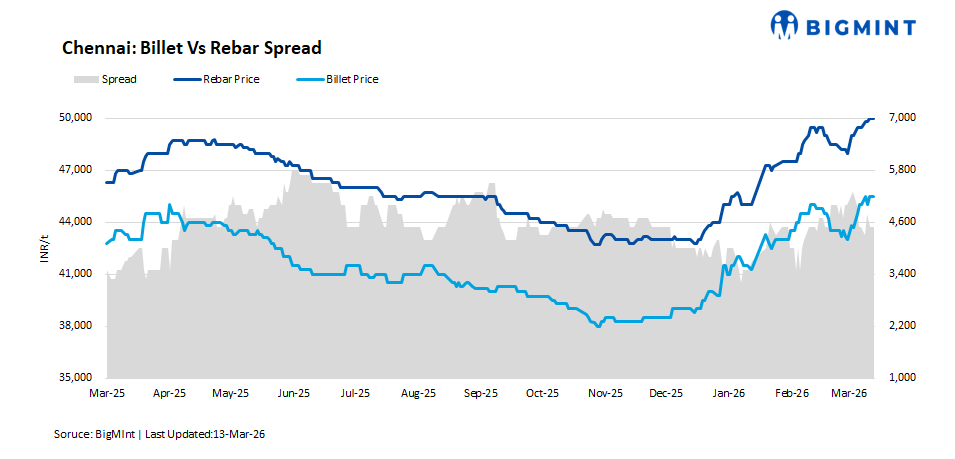

Steel prices in Southern India rose even as raw materials witnessed mixed trends w-o-w in the week ending 13 March 2026. Sponge iron prices edged down, while melting scrap prices rose slightly. Meanwhile, rebar prices remained relatively firm across major markets in Southern India, supported by steady demand and stable buying activity.

Raw material prices

Direct reduced iron (DRI) prices in Bellary declined slightly by around INR 200-300/t, mainly due to limited demand from steel smelters, as demand for finished steel products remained moderate.

Despite the marginal correction in DRI prices, the overall cost of production has increased slightly as coal and pellet prices have moved upward in recent weeks, putting pressure on sponge iron producers.

Market participants indicate that both buyers and sellers had already booked sufficient quantities in the previous weeks, which has resulted in a balanced market situation with no significant supply or purchasing pressure at the ground level.

Meanwhile, RB2 coal prices stood at around INR 12,100/t ex-Gangavaram Port as of 13 March 2026, reflecting an increase of about INR 900/t w-o-w.

In the scrap market, ferrous scrap (HMS 80:20) prices in Chennai increased by around INR 400-500/t w-o-w. The rise is mainly attributed to supply constraints caused by LNG shortages, which have slowed down scrap-cutting activities. As a result, reduced supply and steady demand have pushed melting scrap prices higher.

Semi-finished steel

MS billet prices in the southern regions remained largely stable with a slight positive trend, supported by moderate demand from re-rolling mills as the movement of finished steel products remained steady.

Sources indicated that some merchant suppliers in the Chennai cluster were inactive during the previous week due to scheduled plant maintenance, which created a slight shortage of material in the market and supported a marginal increase in billet prices.

On the export front, a small shipment of MS billets was concluded by Chennai-based merchant suppliers to Colombo, Sri Lanka. Export transactions were reportedly finalised at around $492/t (+/-5%) FOB Chennai Port, indicating steady export interest from Sri Lankan buyers.

Finished steel

Finished steel demand in South India was above-average, with market transactions taking place for around 70-80% of the total production levels.

Large-scale rebar manufacturers operated at near full capacity utilisation and maintained adequate inventory levels to ensure immediate supply for ongoing bookings from end users.

Market participants indicate that the movement of finished steel products remains steady, supported by consistent demand from the construction and infrastructure sectors.

Meanwhile, blast furnace route rebar prices were at around INR 59,100/t ex-works in both Hyderabad and Chennai. Prices are expected to remain stable in the near term, as demand is likely to sustain at current levels.

Leading steel manufacturers continue to offer induction route rebars in the local market at prevailing price levels, although selective discounts are being extended in offers to attract buying interest of customers :

Outlook

Steel prices are expected to remain at current levels in the near term, mainly supported by firm raw material costs. Key inputs such as coal and melting scrap are witnessing tight supply due to global logistics constraints and lower inventory levels, particularly of coal, at ports.

Additionally, the ongoing LNG shortage has slowed scrap processing activities, which may further tighten scrap availability in the domestic market. Amid this tight raw material scenario, steel prices are likely to maintain a positive trend in the short run.

Leave a Reply