- Sponge iron prices in Bellary ease on cautious buying

- Mild steel billet prices remain stable w-o-w in Chennai

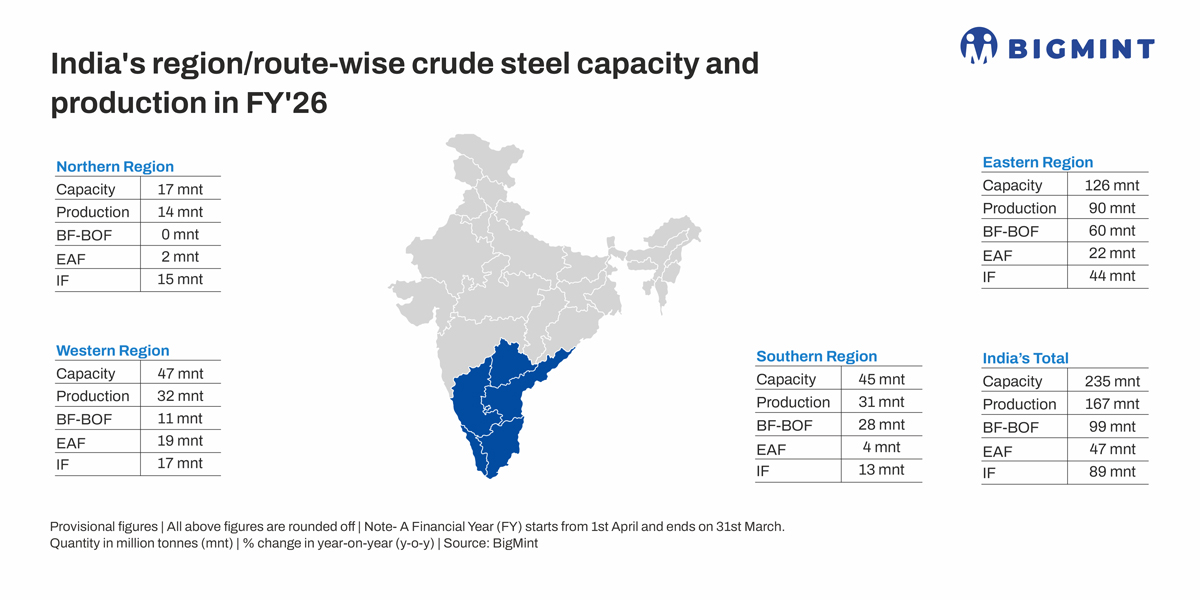

South India is a key hub of steel manufacturing in India, with an installed production capacity of around 45 million tonnes (mnt), accounting for nearly 20% of the country’s total steel production capacity. The region hosts a mix of integrated steel plants, secondary steel producers, rolling mills, and downstream units, supported by a robust port infrastructure, raw material linkages, and established industrial clusters.

In addition to being a major production centre, south India is also a significant steel consumption hub, thanks to the rapid development of modern infrastructure projects, including highways, metro rail networks, ports, renewable energy installations, and urban real estate. The presence of major automobile and auto-component hubs in Chennai, Bengaluru, Hosur, Coimbatore, and Hyderabad further strengthens regional steel demand, particularly for long and flat products.

Overall, the combination of robust manufacturing capacity and strong end-use consumption positions south India as a strategically important region for India’s steel industry, playing a critical role in both domestic supply chains and long-term demand growth.

In view of this, BigMint is launching a weekly insight, starting today, on finished steel, semis and raw material market movements in the key steelmaking clusters of south India with the objective of presenting an incisive and close-up view of market dynamics in the region.

Sponge iron and melting scrap

Sponge iron prices in Bellary corrected marginally by around INR 700-1,000/t w-o-w, primarily due to subdued buying interest at higher prices. Buyers remained reluctant to place fresh bookings, as a significant portion of their requirements had already been covered at lower rates in the previous weeks. The sponge iron mills have secured bookings for at least the next seven to 10 days, reflecting stable near-term demand.

Despite the mild correction, producers refrained from implementing steeper price cuts, as raw material costs continued to remain elevated. Prices of key inputs, particularly iron ore pellets and iron ore lumps, stayed firm, providing cost-side support to sponge iron manufacturers.

Currently, iron ore pellet prices (Fe 63%) are prevailing at around INR 10,550/t ex-Bellary, which has limited the scope for any sharp downside in sponge iron prices in region.

Meanwhile, sponge iron prices in the Hyderabad market also corrected, largely due to subdued demand for finished steel products. Weaker offtake from the downstream steel segment kept buying sentiment cautious, prompting sponge iron consumers to restrict fresh procurement at prevailing price levels.

In contrast, sponge iron buyers increased their bookings of raw materials, especially pellets, from Chandrapur-based manufacturers, citing superior and more consistent quality. This shift in sourcing reflects buyers’ preference for better-quality inputs amid tight conversion margins.

At present, iron ore pellet prices are assessed in the range of INR 10,800-11,000/t delivered to Hyderabad, which continues to influence sponge iron production costs and overall pricing dynamics in the region.

Ferrous scrap prices witnessed a marginal improvement w-o-w, supported by stronger bid levels in select major automobile scrap auctions. The higher auction realisations boosted market sentiment and encouraged sellers to hold firm on price expectations. Additionally, the market experienced a slight shortage in availability, as collection and inflows of scrap remained limited, which further tightened supply. The combination of improved auction benchmarks and constrained supply helped stabilise the market and provided upward support to ferrous scrap prices despite cautious buying from end-users.

Semi-finished steel market

In the Chennai market, MS billet prices remained relatively stable, supported by adequate forward bookings secured by merchant sellers over the past few weeks. Additionally, some volumes were booked for supply to neighbouring markets, which helped absorb available material and maintain price stability despite broader market challenges.

However, overall sentiment remained cautious. Buyers attempted to negotiate lower billet prices, citing subdued demand for finished steel products at higher price levels. Weak downstream offtake has put pressure on rolling margins, leading to reduced conversion costs and limiting buyers’ willingness to accept elevated billet prices.

Meanwhile, elevated ferrous scrap prices continued to provide cost support, preventing any sharp downturn in billet prices. Currently, MS billet (100 mm) prices are prevailing at around INR 41,500/t in the Chennai market.

Finished steel demand

Finished steel demand in south India remained moderate during this period; however, buying activity has been largely restricted to fulfilment of immediate needs. Market participants continued to book material mainly to meet immediate requirements, reflecting a cautious approach at prevailing price levels.

Despite selective buying, large steel manufacturers did not curtail production. The current rebar inventory at the plant level is estimated to be around 10-15 days, indicating a relatively balanced stock position. Current induction furnace (IF) route Fe500 rebar prices are hovering around INR 45,000/t ex-works, while blast furnace (BF) route rebar prices are at INR 52,200/t exy-Chennai. However, these prices may vary across local markets.

Outlook

Steel prices in south India are expected to remain largely stable in the near term, especially during the upcoming festive holiday period. However, trading activity is likely to slow down, as the absence of market participants during the holidays may limit spot transactions. As a result, market liquidity is expected to remain thin over the next four-five days which will keep prices range-bound.

Leave a Reply