- Bangladesh’s tariff incentive could favour US cotton imports

- Pakistan supply gap and China mill demand intensify regional competition

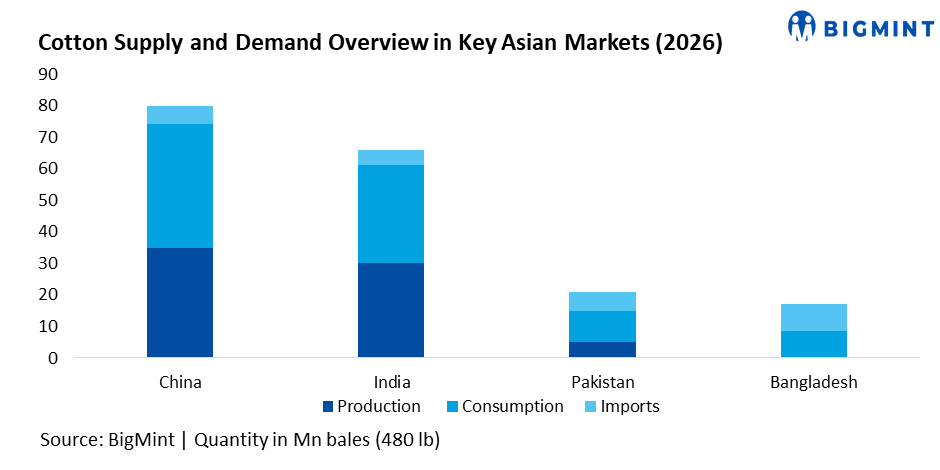

The Southeast Asian cotton market is entering a phase of structural adjustment as trade policies, production imbalances, and shifting textile supply chains reshape trade flows among India, China, Pakistan, and Bangladesh. According to recent global forecasts, cotton production is projected near 116 million bales in 2025-26, while global consumption is expected to exceed 120 million bales, indicating tightening supply conditions. China remains the world’s largest producer with output around 35 million bales, while India remains the second-largest producer with output estimated near 23-24 million bales. Pakistan’s cotton crop, however, has fallen sharply to around 5 million bales, far below the country’s annual mill consumption of 9-10 million bales, increasing its dependence on imported fibre.

China continues to dominate global textile processing and remains the world’s largest cotton consumer, with annual mill use exceeding 38 million bales. Despite strong domestic production concentrated largely in Xinjiang, China still imports cotton to support its massive spinning and textile industry. Meanwhile, Bangladesh has emerged as the largest cotton importer globally, importing more than 8-8.5 million bales annually to sustain its export-oriented garment sector, which ships large volumes of apparel to the United States and Europe.

A major development influencing the regional cotton market is the US-Bangladesh fcotton-for-zero-tariff” arrangement announced in early 2026. Under this framework, Bangladeshi garments exported to the United States can receive zero-tariff access if they are manufactured using US-origin cotton or fibres, compared with the general tariff level of about 19% normally applied to Bangladeshi apparel exports. The tariff incentive effectively links Bangladesh’s garment exports with US cotton supply chains and encourages Bangladeshi manufacturers to increase imports of US fibre to remain competitive in the price-sensitive US retail market.

Bangladesh’s large cotton import requirement means even a partial shift in sourcing patterns could significantly influence regional trade flows. India has traditionally been one of the major suppliers of cotton and cotton yarn to Bangladesh due to geographic proximity and shorter logistics routes. However, Brazil has recently overtaken India as Bangladesh’s largest cotton supplier in some periods, and the new tariff incentive could further strengthen the role of US cotton in Bangladesh’s import basket if garment manufacturers increasingly prioritise fibre that allows duty-free access to the US market.

At the same time, Pakistan’s declining cotton production continues to reshape the regional textile balance. With domestic output near 5 million bales against mill demand exceeding 9 million bales, Pakistan has increasingly relied on imported cotton to sustain its spinning industry. This supply deficit limits its competitiveness in yarn exports while strengthening the role of global exporters such as the US and Brazil in supplying Asian textile hubs.

For India, the evolving regional cotton landscape presents both opportunities and risks. India remains one of the largest cotton producers globally and retains logistical advantages when supplying cotton and yarn to Bangladesh’s textile industry. However, the tariff-linked sourcing advantage for US cotton could gradually reduce India’s share in Bangladesh’s imports if mills adjust procurement strategies to maximise duty benefits in the US apparel market.

Overall, the Southeast Asian cotton market is becoming increasingly interconnected, with trade policies playing a greater role in shaping fibre flows. Bangladesh’s growing dominance in garment exports, China’s sustained textile demand, and Pakistan’s production challenges will remain key drivers of regional cotton trade. For Indian ginners, spinning millers, and brokers, closely monitoring Bangladesh’s sourcing patterns and US cotton shipments will be critical, as shifts in fibre preference could influence export demand and price competitiveness in the coming seasons.

Leave a Reply