- Total imports rise only 3% y-o-y, while Russian volumes surge 130%

- Widening price gap between Russian, Australian cargoes drives shift

South Korea’s coal procurement strategy is increasingly tilting towards lower-cost Russian cargoes as utilities seek to manage fuel costs amid elevated thermal coal prices and tighter regional energy markets.

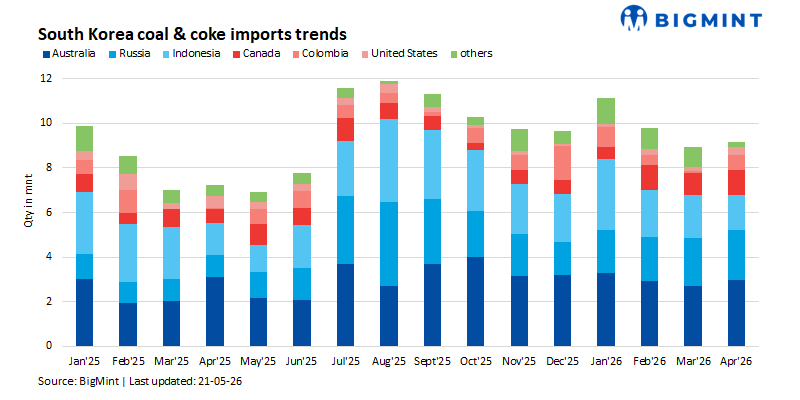

The country imported 9.17 mnt of coal in April 2026, up 2.6% m-o-m, as utilities continued procurement ahead of peak summer electricity demand. While overall import growth remained moderate, the changing composition of purchases points to a growing preference for competitively priced Russian cargoes as buyers balance affordability with supply security.

Russian coal emerged as a key beneficiary of this shift. Imports from Russia surged 128.5% y-o-y to 2.26 mnt in April, supported by a widening pricing advantage over competing Australian cargoes. In contrast, Australian coal imports declined 4.5% y-o-y to 2.97 mnt, although Australia retained its position as South Korea’s largest coal supplier.

Indonesian coal shipments stood at 1.56 mnt, rising 8.2% y-o-y, though declining 18% m-o-m, while Canadian coal imports increased sharply to 1.10 mnt, up 84.4% y-o-y, indicating a broader diversification of procurement.

The widening price differential between Russian and Australian cargoes appears to be at the centre of this shift. Russian coal landed in South Korea at an average $106.96/t in April, significantly below Australian coal at $151.88/t, creating a price gap of nearly $45/t.

In an environment of firm Pacific thermal coal prices, utilities appear increasingly willing to optimise procurement economics by blending with lower-cost material, even where calorific values or ash specifications may vary.

The broader market backdrop has also reinforced coal’s role in power generation planning. Concerns over LNG supply tightness and price volatility, particularly following geopolitical tensions in the Middle East, have encouraged utilities across Northeast Asia to secure additional coal volumes ahead of summer demand.

However, rather than relying exclusively on premium Australian tonnes, South Korean utilities appear increasingly focused on balancing security of supply with affordability by widening procurement strategies toward competitively priced Russian cargoes.

Australia nevertheless continues to dominate South Korea’s coal supply mix, although elevated FOB prices have increasingly challenged its competitiveness. The Northeast Asia 5,750 kcal/kg NAR benchmark averaged $120.02/t in April, sharply above $93.09/t a year earlier, underscoring the broader inflation across Pacific thermal coal markets.

The import mix suggests that while overall coal demand growth remains measured, South Korea’s utilities are becoming increasingly price-sensitive in procurement decisions. So long as the pricing gap between Russian and Australian coal remains substantial, buyers are likely to maintain a diversified sourcing strategy, combining premium supply security with lower-cost alternatives.

Leave a Reply