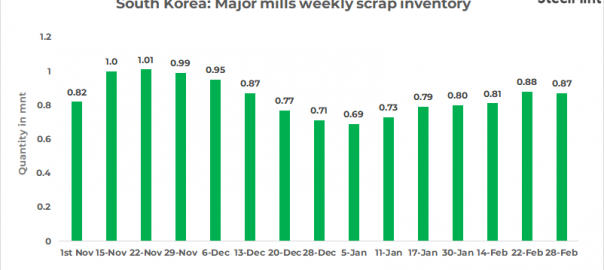

The ferrous scrap inventory of eight key South Korean steelmakers’ dipped 1% w-o-w on 27 February. The volumes were recorded at 867,000 tonnes (t). After showing a consistent rise since the beginning of February, the stocks dipped in the last week of the current month.

On a y-o-y basis, the inventory assessed on 27 February declined 13.6% compared to the same week last year. But, despite the dip, there is still more than 800,000 t of material, keeping steelmakers comfortable.

Company-wise inventory status

Hyundai, Hwan, and Dongkuk Steel: Inventory holdings of Hyundai Steel and Hwan Steel remained almost the same as last week, while inventory holdings of steelmakers in the central region decreased by 10,000 t to 513,000 t due to a decrease in inventory at Dongkuk Steel. While most steelmakers maintained similar levels as in the previous week, Dongkuk Steel’s inventories dipped 7.4% w-o-w.

This appears to be due to increased scrap consumption after the Pohang facility’s repair work schedule was finished, and warehousing constraints were felt with the initiation of repair work at the Incheon plant.

Southern region inventory status: For the week under review, the total amount of scrap stock held by steelmakers in the southern region was 354,000 t, down only 2,000 t from the previous week. Korea Iron & Steel’s inventory increased slightly, while YK Steel’s inventory decreased. Inventories at POSCO and Daehan Steel are at the same level as last week. March typically sees demand for scrap rising. The prevailing view is that demand will also increase but slowly due to a decrease in rebar production and sales amid the recent sluggishness in the construction sector.

In the meantime, market participants do not see any reason for scrap prices to increase due to adequate inventory levels.

In spring, when production and sales of rebar usually increase, demand for scrap habitually rises, and prices naturally spurt at that juncture.

However, the market does not expect the scrap market to behave in the usual manner in March this year. For one, even after March, large steelmakers’ factory maintenance schedules will continue.

Hyundai Steel’s Incheon rebar plant is scheduled for repair from 30 March-7 April, and the Pohang Steel bar plant will undergo repair for 15 days from 16 March till the end of the month. Dongkuk Steel completed repairs at the Pohang plant throughout February and will continue repairs at Incheon’s No. 2 rolling line from 27 February till 7 March 2023.

Secondly, because of the sluggish demand for finished steel items like rebar and sectionals, there is a lull in domestic scrap generation. Thus, steelmakers did not feel the pressure to lower prices. But, imported scrap offers were also declining post-Turkiey quake and Koreans bought inventory in bulk and cheap. As a result, there is stockpile at the ports and scrap prices are falling. But lower scrap prices will also mean mills will have to lessen prices of finished items too.

Outlook Steelmakers’ inventories are projected to remain high till March.

Scrap consumption has declined as a result of the factory maintenance schedule that will unfold in March. Thus, there are strong indications of price declines, while supply is expected to stay stable.

Suppliers’ expectations that Japanese scrap prices, which had recently been strong, would lead to a rise in domestic finished prices, have dissipated.

Note: This article has been published in accordance with an article exchange agreement between SteelDaily and SteelMint.

Leave a Reply