- Domestic Korean scrap prices remain below international levels

- Increased long steel exports of late has tightened iron scrap market

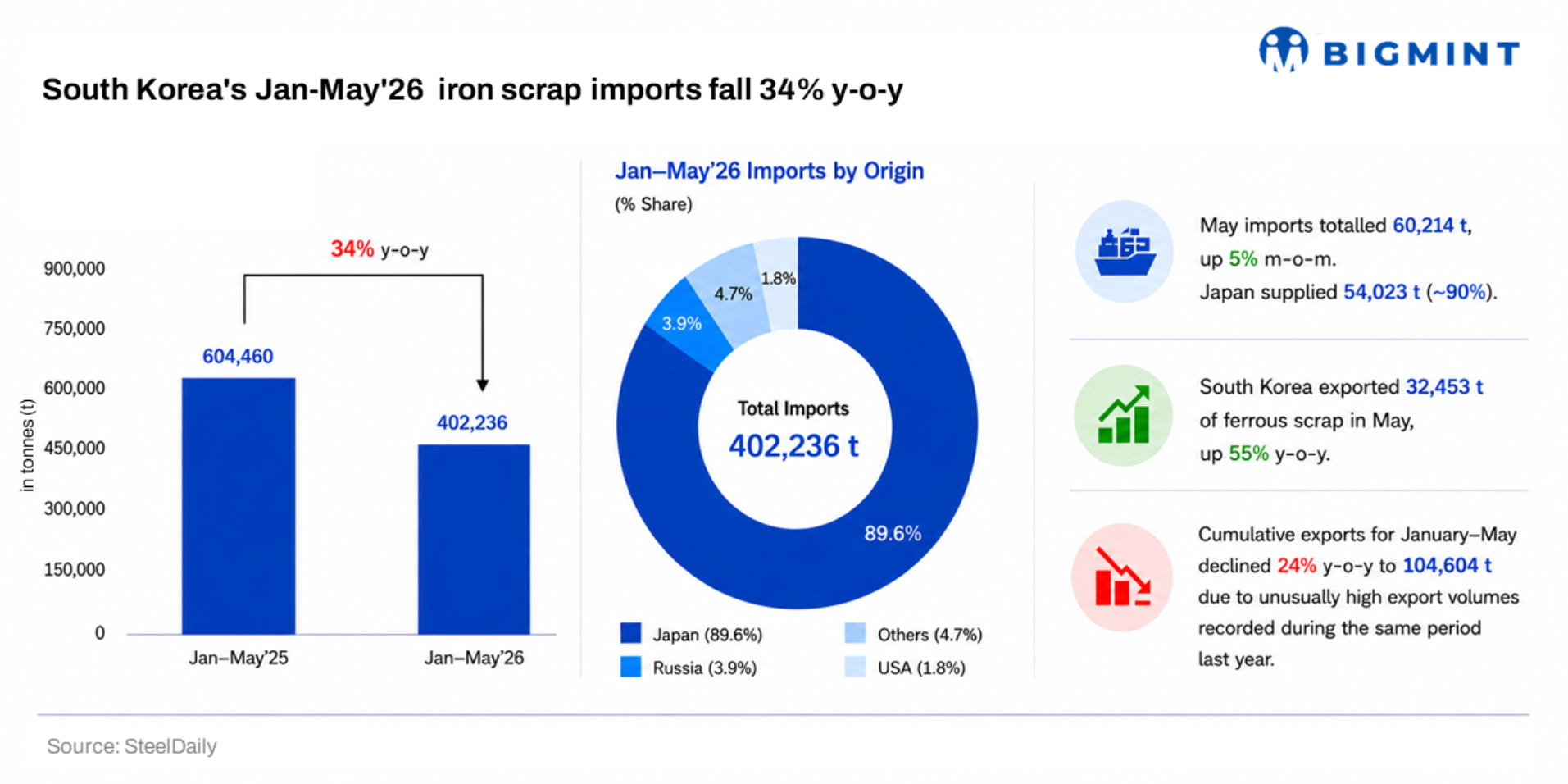

SteelDaily: Despite the continued shortage of iron scraps, imports to compensate for supply shortages have not increased much. In May, the import volume of iron scrap for general use was 60,214 tonnes (t), an increase of 4.8% from the previous month. Compared to the previous year, however, it remained at a low level.

By country, Japan accounted for the largest proportion with 54,023 t, down 9.7% from the same month last year, but up 13.4% from the previous month. Imports from the US amounted to 1,181 t, and there were no imports from Russia. Imports from other regions hit 5,010 t. Philippine-origin scrap accounted for 2,298 t, while 1,143 t were imported from Oceania.

The decline in domestic iron scrap imports has been in full swing since hitting 543,362 t in March 2022. In some periods, imports recorded y-o-y increases, but the overall downtrend continued through May this year.

The main reason for the decline in imports is lower domestic consumption. In addition, the widening price gap between domestic and imported scrap, along with steelmakers’ preference for domestic purchases to improve profitability, has contributed to weaker imports.

This trend is also reflected in import prices. The average import price of iron scrap in May was $379/t, while Japanese material averaged $375/t. Applying the average exchange rate in May, the import cost was roughly KRW 565,000/t. From January to May this year, cumulative imports reached 402,236 t, down 33.5% y-o-y. Japan supplied 363,690 t, accounting for 89.6% of total imports, followed by Russia with 15,765 t and the US with 7,196 t.

Scrap exports remain weak

In May, iron scrap exports stood at 32,453 t, up 54.5% y-o-y. Considering the size of the domestic iron scrap market, the volume is still not particularly high, but exports have continued to rise strongly since the second half of last year. However, cumulative exports from January to May was 104,604 t, down 24.1% y-o-y. During the same period last year, exports were boosted by shipments on large bulk vessels, causing a temporary surge. The average export price was $399/t.

Rebar, H-beam exports surge

On the other hand, exports of rebar and H-beams, both major consumers of iron scrap, are showing strong growth. In May, rebar exports reached 58,558 t, more than six times higher than a year earlier. Cumulative exports from January to May totalled 466,323 t, compared with just 4,526 t during the same period last year. Exports of H-beams are also booming. May exports stood at 118,921 t, up 82.6% y-o-y. Cumulative exports from January to May reached 395,888 t, up 5.9% y-o-y. Although exports weakened somewhat in April, overall shipments have remained above last year’s level.

The increase in rebar and H-beam exports is unlikely to be a temporary phenomenon concentrated in the first half of the year. US demand remains strong, and steelmakers view exports as a key tool for raising utilisation rates. While some producers may reduce exports because of weaker profitability, many rebar mills intend to maintain overseas sales. For H-beams, high US domestic prices continue to support export profitability. Both Hyundai Steel and Dongkuk Steel are expected to focus on exports for the time being. Dongkuk Steel, in particular, established a dedicated export team this year and is actively promoting overseas sales of rebar and H-beams.

Exports tightening scrap supply

Over the past three years, the domestic iron scrap market has largely moved independently of the international market. Imports collapsed as steelmakers’ demand weakened, while domestic scrap prices remained below international levels, reducing import incentives.

However, domestic demand for rebar, which had been a major factor behind weak scrap demand, is beginning to recover. Without the recent increase in steel product exports, supply and demand could likely have remained balanced even with imports below 100,000 t per month.

Instead, rising exports of rebar and long products are gradually tightening the iron scrap market. Procurement managers at steelmakers increasingly believe that improving supply-demand conditions will be difficult without higher imports.

At the same time, poor profitability continues to discourage purchases of relatively expensive imported scrap. As a result, the supply imbalance may persist for some time. According to a steelmaker official quoted in the article, “Import scrap prices need to fall significantly before active import purchases can be seriously considered.”

Note: This article has been written in accordance with a content exchange agreement between SteelDaily and BigMint.

Leave a Reply