- Turkiye market soft amid weak rebar demand

- Bangladesh stable, high freight leads to limited buying

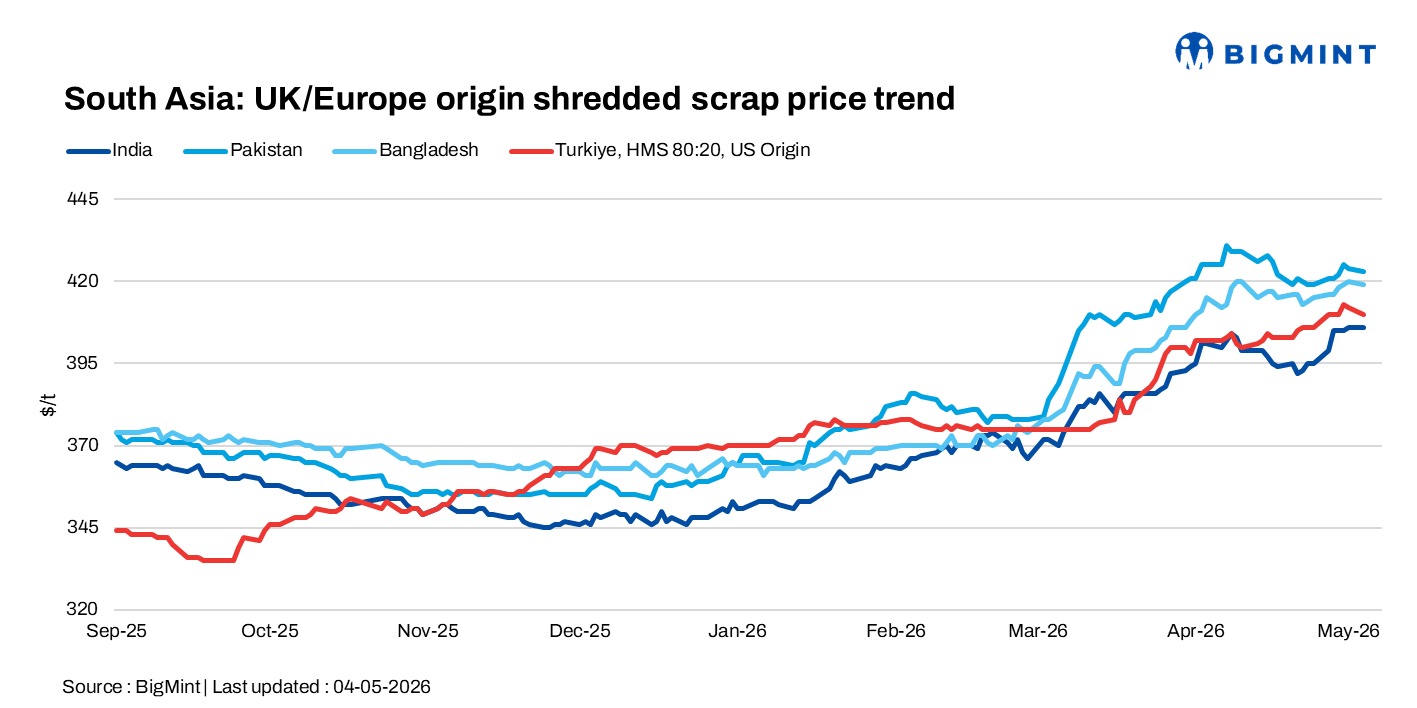

South Asian imported scrap markets remained subdued to stable on 4 May 2026, with weak demand in India, steady deal flow in Pakistan and stable prices in Bangladesh. However, softer sentiment was seen in Turkiye, as cautious buying and recent holidays continued to limit trading activity.

India: The imported scrap market remained subdued d-o-d, with no deals or fresh offers reported as the UK and European markets were closed due to bank holiday. Trading activity stayed dull, with market participants expecting clarity once sellers return.

Indian containerised scrap prices remained flat, with Africa-origin HMS 80:20 offered at $385-395/t against bids at $375-380/t, while EU-origin HMS was heard at $380-385/t. Shredded offers were around $415/t, but the absence of buyer interest kept the market inactive.

Pakistan: Imported scrap prices remained firm on steady deal flow. Malaysia-origin busheling was heard at $435-440/t CFR Karachi, while shredded and busheling were offered and reportedly sold around $445/t CFR Qasim. Additionally, turning scrap deals were concluded at $370/t CFR Qasim, reflecting stable demand at current levels.

Bangladesh: Imported scrap prices in Bangladesh remained largely stable, with a deal for 1,000 t of Chile-origin HMS 90:10 concluded at $415/t CFR Chattogram. Offer levels were heard at $400-405/t for Brazil-origin HMS 80:20, while Hong Kong-origin PNS (oversize) was around $440/t, with tradable indications at $425-430/t and AB bundles near $410/t.

Market activity remained limited as high freight costs restricted Far East offers, though around 1,500-1,600 t cargoes from Korea were heard for Chattogram. Overall sentiment stayed steady with selective buying and resistance to higher offers.

Turkiye: Deep-sea imported scrap market remained largely stable d-o-d, though prices showed slight downward pressure as Turkish import levels softened. US-origin HMS 80:20 offers were heard around $410/t CFR, indicating increased activity toward the end of the week.

However, sentiment stayed weak as mills resisted higher prices amid subdued rebar demand and limited trading due to public holidays in Turkiye and Europe. The market remained cautious, with price direction leaning softer despite improved deal flow.

Leave a Reply