- Turkiye: HMS 80:20 edges lower on soft rebar demand

- Pakistan, Bangladesh demand weak keeps trade sluggish

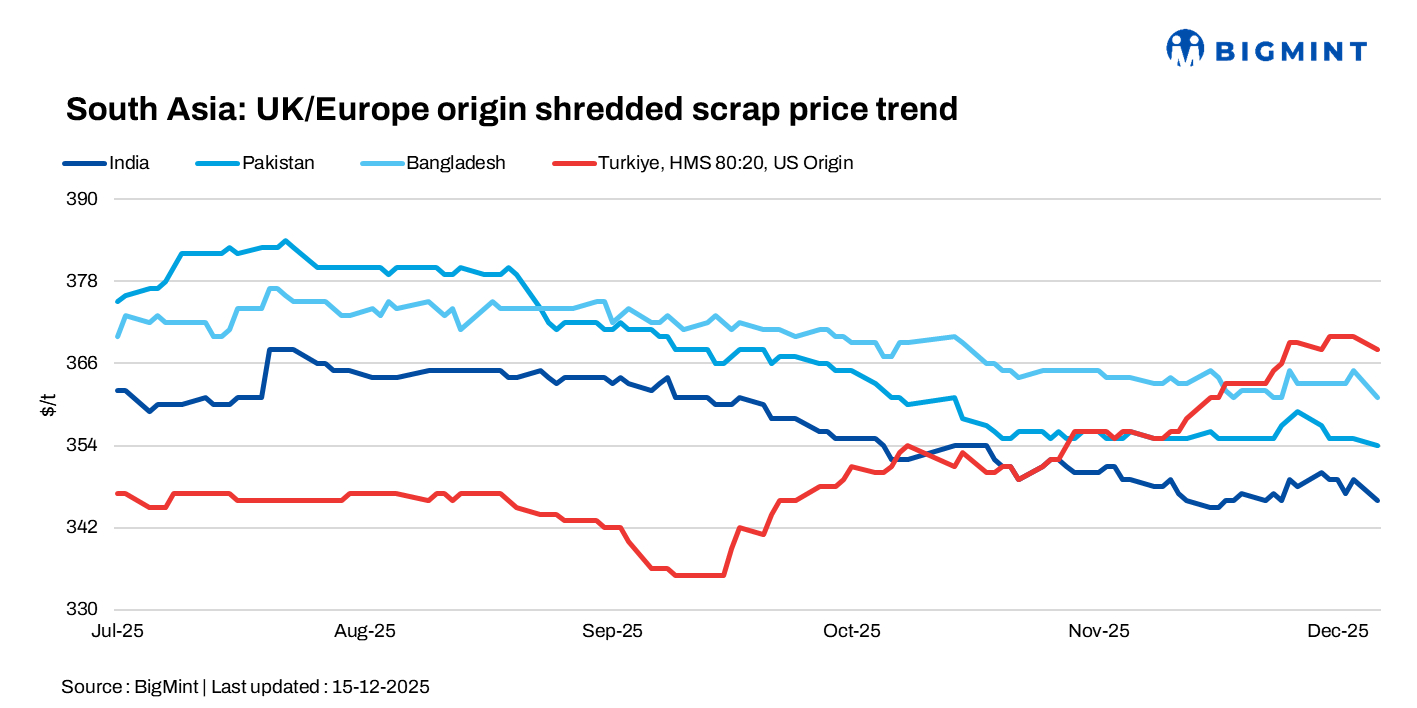

South Asia scrap markets stayed subdued on 15 December, led by weak import demand in India, Pakistan, and Bangladesh amid currency pressure and weak steel consumption, while Turkiye recorded marginal d-o-d price easing as mills delayed bookings despite firm supply-side fundamentals.

India: Indian imported containerised shredded scrap prices eased on 15 December, as the rupee’s slide to record lows against the US dollar further reduced buying viability. The weak exchange rate, along with ample availability of cheaper domestic scrap, weighed on already subdued import demand, prompting buyers to step back unless material was urgently required. Shredded scrap hovered around $346/t CFR Nhava Sheva, while EU-origin HMS 80:20 stood at $315-318/t CFR.

Pakistan: The imported scrap market remained very slow on 15 December, with trading sentiment quiet and lacking momentum. Buyers were active only at lower workable levels, while offers were heard around $353-354/t CFR, leaving limited room for deal closure and keeping overall activity subdued.

Bangladesh: Bangladesh’s imported scrap market stayed subdued amid weak downstream steel demand and cautious buying sentiment, while Australian-origin prices were assessed at $330-332/t CFR for HMS 80:20, $335-338/t for HMS 1, $358-360/t for shredded, and $364-365/t for PNS, with buyers remaining selective and trade volumes limited.

Turkiye: Deep-sea scrap import prices edged lower d-o-d on December15, with HMS 80:20 easing slightly to around $368/t CFR. The dip was driven by softening downstream rebar demand, which continued to pressure mills’ buying appetite despite otherwise firm market fundamentals.

Sentiment remained mixed as mills resisted higher scrap levels, expecting prices to soften further, even though high collection costs, firm freight rates, and limited seller offers supported the market. Mills were reported to have low scrap availability in yards but continued to delay January–February 2026 bookings, while currency movements between the euro and dollar were also closely monitored.

Leave a Reply