- Turkiye: US-origin deals support prices despite slower activity

- India: Buyers resist high offers, demand remains weak

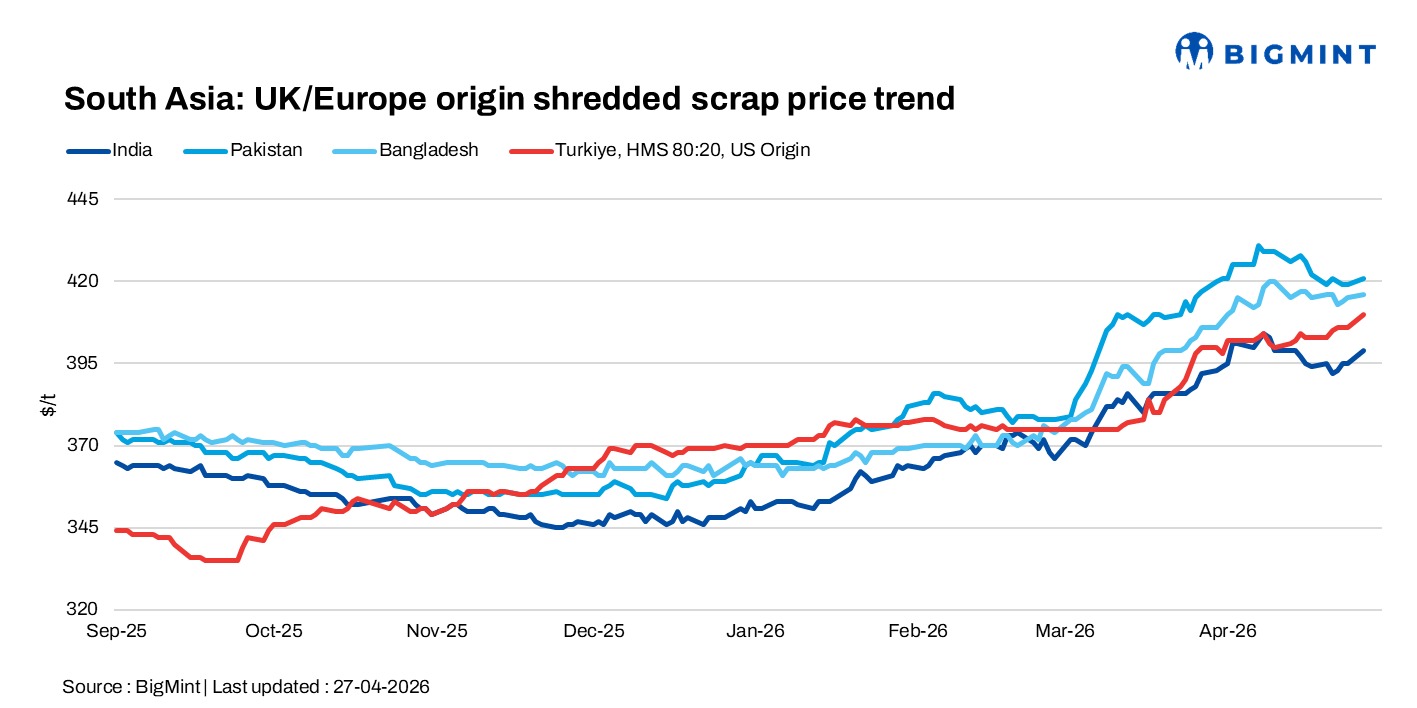

The South Asian and Turkish scrap markets remained largely stable on 27 April, with weak demand in India, Pakistan, and Bangladesh limiting activity, while in Turkiye prices held firm on US deals amid cautious buying.

India: Imported scrap market rose but elevated bulk offers from the US failed to attract buyer interest. HMS offers were heard above $415/t CFR and shredded at $420-425/t, but the wide gap between offer levels and workable prices kept trading activity minimal. No major bulk arrivals were reported at key ports such as Kandla and Chennai over the past two to three months, reflecting weak import demand.

Imported scrap prices were pressured by lower buying indications, with shredded around $400/t CFR and HMS near $380/t, while some buyers sought HMS closer to $375/t. Recent supplier offers included UK-origin Bluesteel at $430-435/t, HMS at $385-386/t, shredded (3-4% impurity) at $395-400/t, and low-impurity shredded at $405-415/t CFR.

Pakistan: The imported scrap market remained largely quiet, with buyers staying inactive despite available offers and no major deal closures reported. Offer levels were heard at around $425/t CFR Port Qasim for UK-origin shredded scrap, while weak demand continued to limit trading activity. The Monetary Policy Committee’s decision to raise the policy rate by 100 basis points to 11.50% effective 28 April 2026 further added pressure on sentiment, potentially tightening liquidity and discouraging fresh bookings.

Bangladesh: Imported scrap prices in Bangladesh remained stable, with HMS 80:20 at $400/t CFR Chattogram and indications at $390-395/t. Weak buying interest persisted as cheaper domestic scrap reduced import demand.

Turkiye: Deep-sea imported scrap prices remained slightly firm in Turkiye, with US-origin deals concluded at $410/t CFR for HMS 80:20 and $430/t CFR for shredded for May shipment. However, market activity slowed toward the end of the week as mills turned cautious. Buyers were heard bidding lower at around $400/t CFR for EU-origin cargoes, indicating resistance to higher offer levels. While earlier US deals provided support to prevailing prices, subdued steel demand and cautious procurement strategies limited fresh booking activity.

Leave a Reply