- Limited vessel inflows restrict overall market activity

- Geopolitical tensions continue influencing regional dynamics

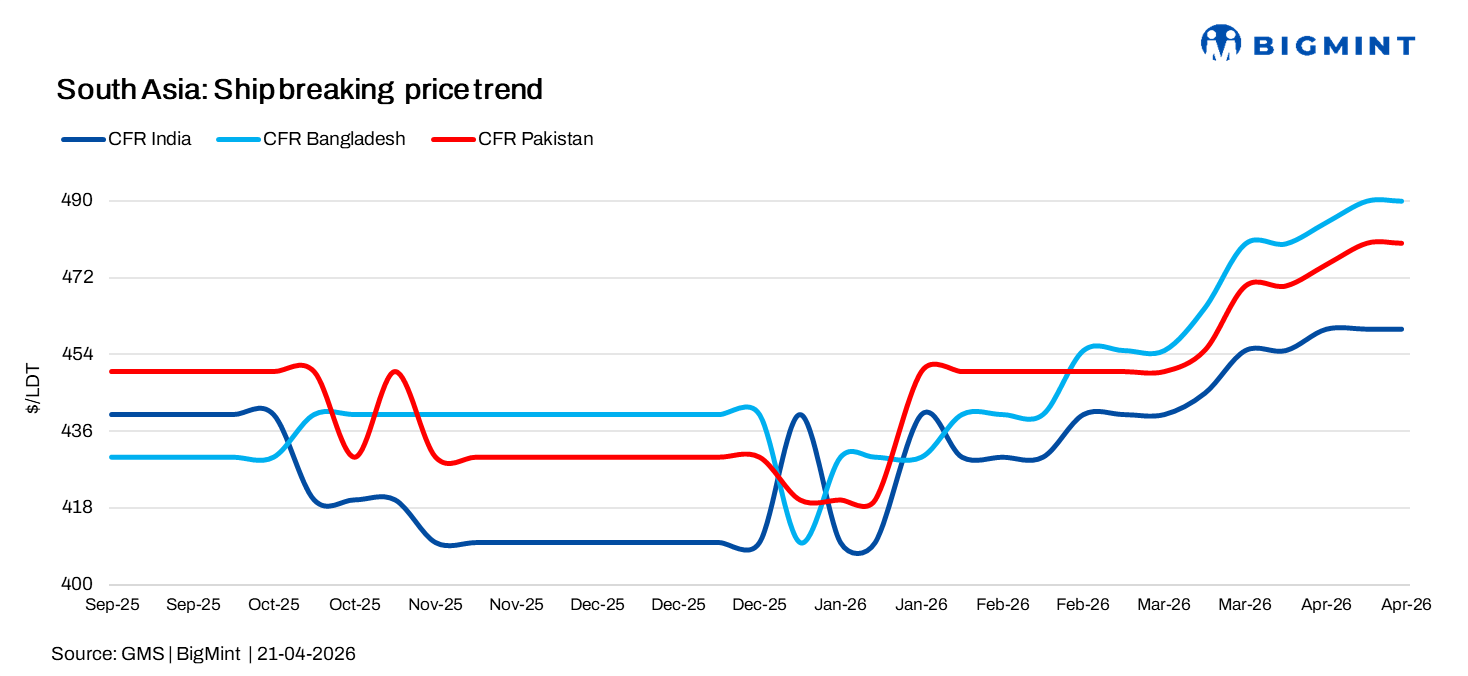

South Asian ship recycling markets showed mixed trends in Week 16, with firm pricing across Pakistan and Bangladesh, while India remained under pressure due to currency weakness, energy constraints, and limited vessel availability.

Alang ship recycling under pressure amid constraints

India’s ship recycling market remained under pressure, weighed by a weakening rupee and ongoing geopolitical tensions affecting the Strait of Hormuz. Despite softer global oil prices, energy costs stayed elevated due to supply risks, with RBI intervention remaining cautious. At Alang, LPG supply disruptions eased slightly, while steel plate prices fluctuated within a narrow range, eventually settling at stable levels.

Limited vessel inflows, firm freight rates, and the approaching monsoon season restricted activity, keeping overall supply tight and market sentiment cautious.

Gadani ship recycling firm on strong pricing

Pakistan’s ship recycling market maintained firm momentum, supported by a stable rupee and strengthening local fundamentals. Steel plate prices strengthened, placing Gadani at its strongest USD levels this year and significantly widening the gap with India. Despite inflation at 7.3%, steady currency conditions helped sustain yard margins.

Geopolitical tensions, including the continued closure of the Strait of Hormuz and US naval presence, favored Pakistan’s geographic positioning, supporting vessel inflows. Compliance levels also improved, with three HKC-certified yards operational and more expected. However, the key uncertainty remains whether this advantage will translate into firm deals, as vessel availability and geopolitical developments continue to influence near-term market direction.

Chattogram market firm amid tight vessel supply

Bangladesh’s ship recycling market remained firm, supported by stable steel plate prices and a steady currency against the US dollar. Chattogram retained its position as the highest-paying and most active market in the sub-continent, particularly as the pre-monsoon window narrows, limiting time for fresh deals.

LC-related constraints eased post-Eid, aiding smoother transactions; however, compliance concerns–especially regarding sanctioned vessels–kept scrutiny high. Despite firm pricing and stable macro conditions, vessel inflows remained limited due to tight availability and strong freight markets. As a result, while demand remains healthy, actual deal conversions continue to face supply-side challenges.

Leave a Reply