The South Asian ship-recycling market witnessed diverse dynamics in the past week, reflecting contrasting fortunes across India, Pakistan, and Bangladesh. In India, the ship-recycling sector faced persistent challenges, with Alang buyers struggling to compete amidst a shortage of available tonnage and subdued local sentiments due to upcoming holidays and election uncertainties. Conversely, Pakistan experienced a semblance of stability post-general elections, with an easing of Letter of Credit (LC) issuance boosting demand from Gadani Recycles, albeit against a backdrop of limited tonnage availability and stagnant steel plate prices.

Bangladesh emerged as a bright spot following its elections, with increased availability of LC fueling demand in Chattogram and positioning the country atop the market rankings once again. The positive momentum was palpable with swift vessel removals and beaching, underscoring the market’s healthier stance. Despite fluctuations, the Bangladeshi taka (BDT) held steady against the US dollar, further bolstering confidence in Chattogram’s ship-recycling market.

INDIA

India’s ship-recycling sector continues to struggle, firmly placing itself at the bottom of the sub-continent market rankings. Despite efforts, Alang buyers find it increasingly difficult to compete with stronger offers from Gadani buyers and more aggressive Chattogram Choppers, creating a challenging environment for India’s performance. Factors such as a shortage of available tonnage, upcoming Holi holidays, and uncertainty surrounding the country’s general elections contribute to subdued local sentiments.

Although India’s fundamentals remain relatively steady, with the Indian rupee (INR) hovering around the INR 83 mark against the US dollar and local steel plate prices showing stability despite past losses, the market experiences volatility, with Indian plate prices closing slightly higher this week. The scarcity of vessel arrivals at Alang’s waterfront is apparent, leaving Alang buyers reliant on HKC-only units and highlighting India’s lower offer levels compared to neighbouring competitors.

Despite efforts to attract environmentally conscious ship owners, such as MSC’s commitment to HKC-only recycling, there has been no significant influx of vessels into India, resulting in zero market fixtures for Alang. Overall, India’s ship-recycling sector faces significant challenges in competing with neighbouring markets, with uncertainties surrounding elections and a lack of vessel arrivals contributing to ongoing performance issues.

A recycler expressed concern about the current market conditions, stating, “Market conditions are very bad. There are no available ships in Alang.”

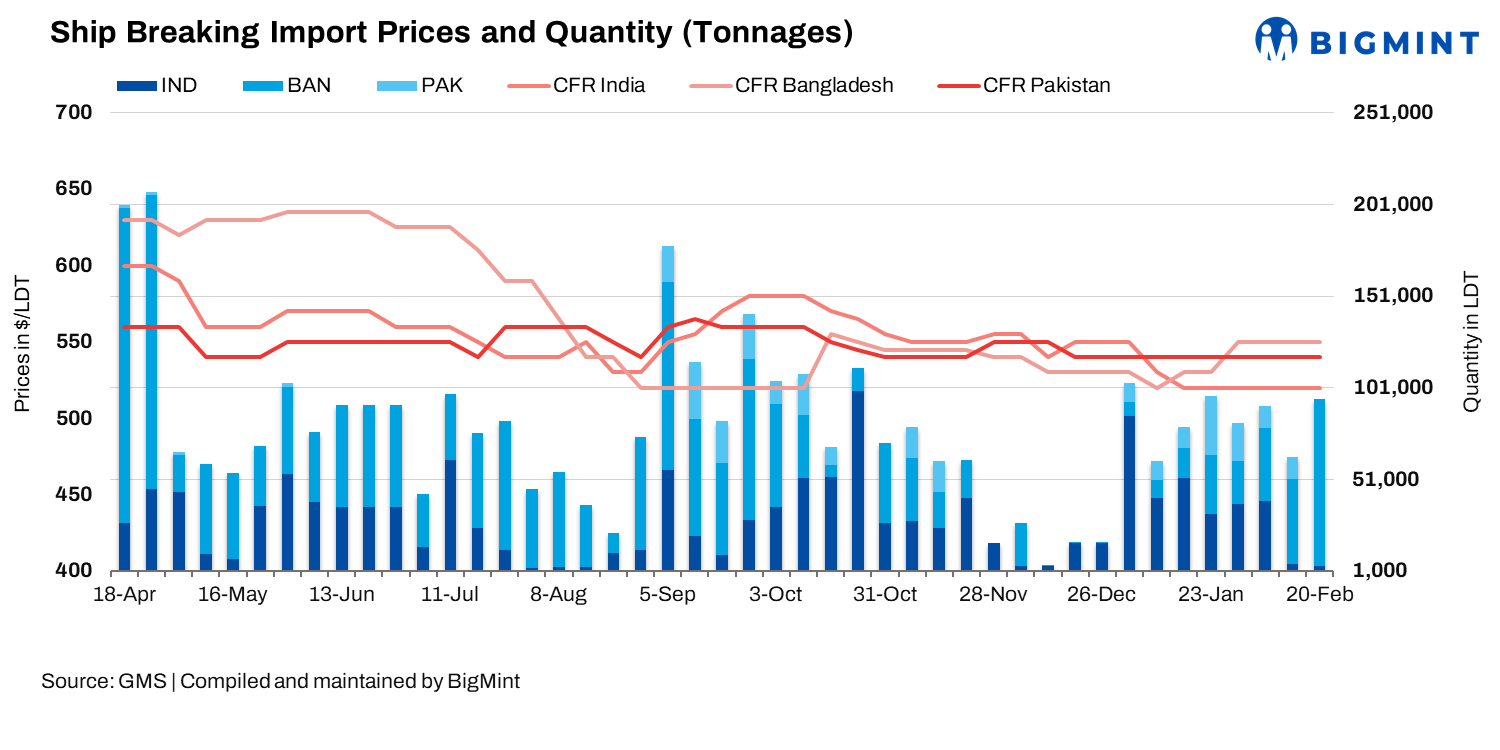

The total tonnage received in Alang was around 3,934 LDT this week.

BANGLADESH

Following the conclusion of Bangladesh’s general elections, there has been a notable increase in the availability of Letters of Credit (LCs) for domestic ship recyclers in Chattogram, leading to a surge in demand from the market. This uptick in availability has spurred aggressive negotiations and heightened demand for tonnage, positioning Bangladesh at the forefront of the market rankings once again. The root cause of the previous LC issues can be traced back to a shortage of U.S. dollar reserves in both Bangladesh and Pakistan, prompting governments to restrict LC issuance from domestic banks.

While some LC problems persist, a majority have been resolved, resulting in increased interest and demand from Chittagong Choppers. This renewed enthusiasm is evident in the swift removal and beaching of vessels in Chattogram, contrasting sharply with the quiet beaches of neighboring competitors. Despite minor fluctuations, the Bangladeshi taka has stabilised against the U.S. Dollar, while local steel plate prices saw a slight decrease. Overall, the Chattogram ship recycling market is currently in a healthier position than it has been in some time, signaling positive growth for the industry.

The total tonnage received in Chattogram port was around 90,942 LTD this week.

PAKISTAN

Following Pakistan’s recent general elections and the announcement of a coalition government, the country appears to be settling into a period of relative calm after pre-election uncertainty and violence. With the easing of LC issuance for vessel recycling following reports of an IMF loan agreement, demand from Gadani Recycles has surged. However, this comes at a time when tonnage availability is extremely limited, leaving local recyclers uneasy. Despite this, Gadani continues to face challenges due to ongoing vessel supply shortages and domestic volatility, with steel plate prices remaining stagnant as the Pakistani rupee (PKR) weakens against the US dollar.

Meanwhile, Bangladesh maintains its lead in ship-recycling numbers, expected to remain the preferred destination for vessels from the Far East following the conclusion of the Chinese New Year holidays. This trend is evident in Chattogram’s bustling port activity contrasted with Gadani’s empty port, resembling a ghost town. It is likely that future vessels will continue to favour Bangladesh, particularly if HKC units and Chinese-owned tonnage resume recycling sales.

A recycler commented, “The market is a bit quiet as people are anticipating a correction. International sellers are feeling pressure due to downturns in Chinese futures and the Turkish market.”

Notably, no tonnage was received at Gadani Port this week.