- India witnesses soft start to Q2 but demand rebounds

- HKC compliance, weak arrivals pressure Pak, B’desh

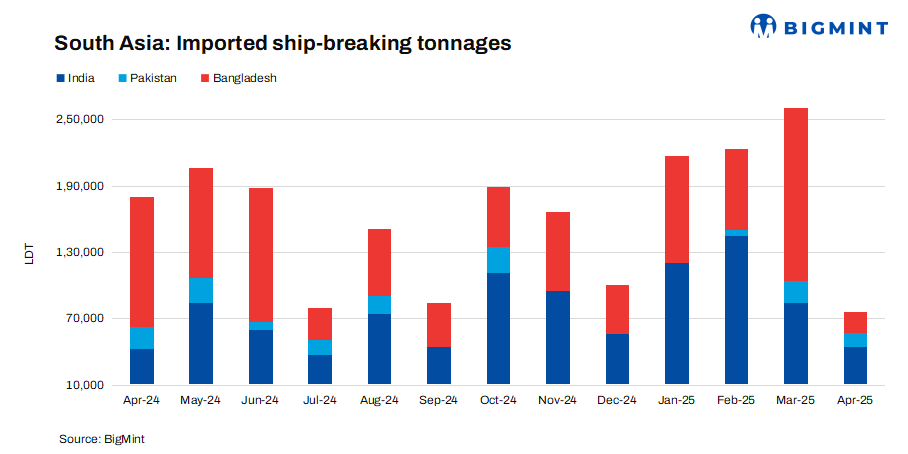

South Asia’s ship-breaking market saw a slowdown in April 2025. India dominated the regional market in terms of the tonnage processed, despite mixed sentiment. Bangladesh was slowed by delays with no objection certificates (NoCs), and Pakistan faced weak fundamentals and limited arrivals.

India: India’s ship-breaking sector processed 44,062 light displacement tonnes (LDT) in April 2025, a 48% decline compared to March’s 83,934 LDT. However, this was a 3% increase compared to the 42,925 LDT recorded in April 2024.

The Alang ship-breaking yard saw a decrease in arrivals, receiving eight vessels for recycling in April, three fewer than in March.

India’s ship-breaking market saw mixed trends during the month, with Q2 starting slowly despite a $10/t rise in plate prices, indicating a recovery in demand, and a stronger rupee (INR). US tariffs and global uncertainty weighed on sentiment, and from the middle of the month, arrivals declined, as recyclers grew cautious amid weak margins and pressure from falling Chinese steel prices.

Alang took the first place in subcontinental rankings in terms of tonnage processed, supported by higher arrivals and improved demand. However, the market remained volatile, with routine tonnage, high prices, and overcapacity limiting fresh purchases.

Pakistan: Only 13,533 LDT of tonnage arrived in April 2025, marking a 34% decline from March’s 20,572 LDT. This also represented a 30% drop compared to the 19,204 LDT recorded in April 2024. Notably, only two ships were recycled in April.

Pakistan’s ship-breaking market faced challenges, as Gadani struggled with slow progress on Hong Kong Convention (HKC) compliance and limited vessel arrivals, mainly small tonnage. Steel plate prices dropped to $624/t, and the weak Pakistani rupee (PKR) added pressure.

Larger vessels continued to head to India and Bangladesh, keeping Gadani’s yards idle. The market remained cautious, with the upcoming budget and HKC implementation adding uncertainty.

Recyclers faced rising pressure from Chinese steel imports and the monsoon season, leaving the outlook for Pakistan’s ship-breaking sector bleak.

Bangladesh: Bangladeshi recyclers processed approximately 18,684 LDT in April 2025, representing a significant drop of nearly 89% from the 164,208 LDT recycled in March. This also marked an 84% decline compared to the 118,231 LDT recorded in April 2024.

Six ships were recycled during the month, down by eight compared to March, reflecting a notable decrease in m-o-m performance.

Bangladesh’s ship recycling market slowed sharply in April amid Eid holidays, delayed NoC approvals, and uncertainty over the upcoming HKC compliance deadline. Several vessels were stranded or diverted, while only HKC-approved yards could operate. The weakening Bangladeshi taka (BDT) added pressure to sentiment, alongside a decline in steel plate prices.

Overall, despite strong early-month pricing and stable remittance-driven reserves, prolonged NoC suspensions, limited arrivals, and delayed government clarity on HKC upgrades left Chattogram yards struggling, putting Bangladesh’s market dominance at risk.

Leave a Reply